Illumin Update: Amazing Set-Up

It's in the adding zone

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program, which means I have a financial relationship with Seeking Alpha. This article is for entertainment purposes.

Mongolian short AD: THE LINK

Get a 7-day free trial and the SUMMER SALE 60$ discount on your first year of Seeking Alpha Premium with my Affiliate link: AFFILIATE LINK

If you sign up for 1 year of SA premium using my link, you will get a free one-year premium sub to my substack. Contact me and provide proof.

My last article, where I was pounding the table on a stock, was this Sintana Energy update, where I wrote, “I think the risk/reward is better now than it has been at any other time I have known about this stock, and I have bought the dip.” Sintana has gone up since then and has left my adding zone, but I would characterize Illumin right now at 1.82 CAD exactly how I characterized Sintana in that quote. Illumin is my favorite stock to add to at this moment.

This is not a situation where I’m averaging down like I was averaging down on Sintana at 50 cents CAD. My cost-basis for Illumin is 1.83$, and the stock is right around there now. The stock hovered around 1,4-1,5$ for a while in 2024, and I was saying at the time that I liked the stock. Why do I like it even more now at 1.82$?

It comes down to how the thesis is advancing. Illumin's thesis in 2024 at 1,45333$ was that the stock has low downside due to the net cash being 55m and the market cap being 75m, no debt, and roughly cash flow neutral. If the company remains in that position, the downside of more than -26.67% is highly improbable, as the market cap would be the same as net cash. The stock also had a lot of upside potential if they get back to revenue growth, as revenue was flat at the time, or they improve their profit margins, or ideally, both.

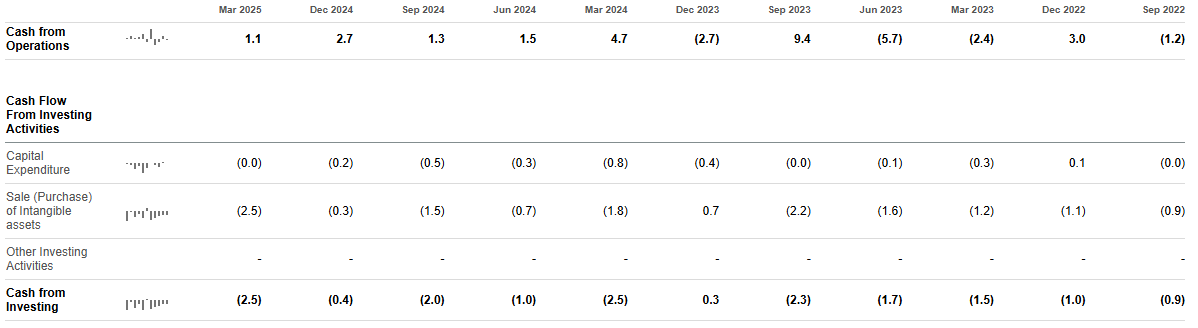

All the numbers are in CAD

Source: Seeking Alpha Premium

In the last 3 quarters, Illumin returned to y-o-y growth.

Q3 +23%

Q4 +35%

Q1 +17% Growth weakened here due to one of their big clients restructuring

Illumin growth should be measured against as y-o-y, not q-o-q, because the business is seasonal. Q4 is always the best quarter, and Q1 is always the weakest quarter. The cash flow hasn’t improved much due to increased costs for R&D and marketing. These are not huge growth numbers, but because the expectations were so low and the market was apathetic about the stock, it had pushed the valuation to a point where even a modest improvement could drive the stock price up a lot, and it did.

Source: Google

I was patting myself on the back as the stock was going past 3$. It’s a turnaround, I was right. For some reason, the gains feel better when it’s an unpopular stock like Illumin. For example, Aduro has gone up a lot, but seeing all these other people also enjoying their Aduro gains takes away from my enjoyment of my Aduro gains.

It’s still a turnaround, and I’m still right; the stock is just taking a little detour at the moment.

Now we have seen where the stock is headed when the market starts believing that the company is getting to growth. It’s heading past 3$. Easily. Right now it’s 94m market cap, 40m EV, 144,5m TTM revenue, roughly cash flow neutral adtech business. It’s not going to stay at this valuation if it’s growing consistently or starts improving its profitability, or both.

Why did it fall back to 1,82$?

To figure out whether the turnaround thesis is still intact, we have to look at the reasons why the market took the stock down and whether they are fatal to the thesis.

-Tariffs/Trade war fears

I won't conduct a comprehensive economic analysis of the impact of tariffs on the global economy. You can get that meal at a number of different locations.

Adtech got hit heavily when Trump’s trade war started because when there are economic problems, advertising budgets are one of the first places to cut costs.

Source: https://ceo.ca/content/sedar/ILLM-2025-05-09-interim-financial-statementsreport-english-ff90.pdf

Illumin is heavily US-focused.

Source: Seeking Alpha Premium

Here is the YTD performance of some businesses that get the majority of their revenue from advertising. Strongest being ZOOMD, which is my other adtech play, and weakest being Trade Desk, which is a huge Adtech company that has been growing for a while and had/has a very high valuation.

Tariffs started in February and intensified with the Liberation Day on April 2nd. Looking at the Q1 results of these companies, they are not showing much impact; Q2 should start showing the impact, whatever it ends up being.

Trade Desk is projecting 17% growth y-o-y in Q2. Illumin said in the Q1 call on May 9th that “We are now seeing a higher level of activity that continued from the second half of Q1”, but also indicated some impact from the tariffs. Zoomd grew 100% y-o-y in Q1 and said on the May 29th earnings call that the momentum continues. Meta guided 8.8-16.5% y-o-y growth in Q2, and Alphabet didn’t guide anything. For some of these businesses, high organic growth may be masking the economic impacts, like Zoomd, but in general, based on numbers, company statements, and projections, we are not seeing a significant slowdown in the adtech space from the tariffs. And from the above chart, we can see that some of these stocks have already fully recovered from the trade war lows, and the rest have started to recover, except Illumin.

Overall industry projections for the Adtech industry have been 12-22% of annual growth into the 2030s. The big trend is that this space is growing while the trade war creates uncertainty I don’t see it as a big enough risk to not invest in Adtech. It’s an unpredictable variable, and in general, with the macro situations, usually they are best ignored and focus on the companies, and only focus on a macro situation if it has a very large impact on the company. Remember the varus? Remember the regional bank crisis? Remember the trade war? I don’t.

-Weak Q1 results

The results weren’t that bad. It was better than Q1 2024. They grew 17% y-o-y, but the stock started going up after 23% Q3 and 35% Q4. Then the trade war started, and growth slowed down in Q1(not caused by the trade war), and the stock price gains from late 2024 to early 2025 were almost completely wiped out.

Also, the company said in the Q4 call, “In terms of Q1, I will say that the Q1 did start slower than we wanted. That was primarily due to the market coming back just on the calendar adjustment, a week plus later. And then, some of the macro uncertainty related specifically to the macroeconomic condition right now” “So we did see marketing budgets in January get approved later than normal. I have seen deal velocity pick up in the second half of Q1 2025. I have seen improved ARPU, average revenue per customer related to the self-service product in particular. I have seen improved overall channel adoption and stickiness. And so we are currently tracking ahead of Q1 fiscal year ‘24.” So I thought with these comments, something like 10-20% growth for Q1 was priced, but I guess it wasn’t because the stock tanked right after Q1 results were released. I have learned that it’s impossible to know for sure if an event is priced in. I can have an educated guess, but how informed the broad market is about a specific stock is hard to tell.

Apart from the marketing budgets being approved later and macroeconomic conditions, this also hurt Q1 revenue:

“a large client that reduced spending by $2 million during the quarter due to their own specific circumstances, including undergoing a business restructuring."

If a large client hadn’t gone into restructuring, Q1 growth would have been 24,4% y-o-y.

Inflexio Research Pointed out on X that this client is WeightWatchers.

Source: https://www.adexchanger.com/platforms/dsp-acuityads-valued-at-600-million-after-us-ipo/

Illumin’s old name was Acuityads, and here they confirmed WeightWatchers as a client, and WeightWatchers is going through a restructuring at the moment.

Source: https://corporate.ww.com/news/news-details/2025/WeightWatchers-Takes-Strategic-Action-to-Eliminate-1-15-Billion-of-Debt-Strengthening-Financial-Position-for-Long-Term-Growth-and-Profitability/default.aspx

WeightWatchers continues to operate, but I assume it will do so with a significantly reduced advertising budget until the reorganization is complete. After it’s done and emerges as a public company, it’s likely Illumin will experience some revenue growth, as they would likely want to demonstrate growth following the debt repayment and public listing, assuming they remain Illumin's client and we have not been led to believe otherwise for now.

This was masking some organic growth in Q1. Overall, it was an interesting quarter in terms of the revenue mix.

They said managed fell because of Geopolitical and macroeconomic uncertainty, but in the call, they said, "We are encouraged to see that the increased momentum in managed service in the latter half of Q1 continue into Q2,”

But at the same time, their “recently reinvigorated Exhance Services line” Revenue grew 149% y-o-y. I’m certainly glad they reinvigorated that business. It would have been a very bad quarter with that business unreinvigorated.

Self-service was basically flat due to WeightWatchers masking the growth from 18 new clients and a +30% average spend per client increase y-o-y.

"our self-service revenue increased 1% year-over-year, but we are pleased to have added 18 new customer relationships in the quarter while we continue to see increased average revenue per client. This self-service growth was offset by a large client that reduced spending by $2 million during the quarter due to their own specific circumstances, including undergoing a business restructuring. We expect that the new clients we added during the quarter will mainly offset this impact going forward as these customers ramp up their spend. Excluding this particular large client spend, our average spend per client increased 30% year-over-year."

-Change in Strategy

The increase in spend per client was communicated by the old management as one reason for the weak revenue, when they were really pushing their clients to switch from managed to self-serve. I quoted this from my original write-up in 2024.

“As far as Q4 is concerned, in general, we're still seeing challenges on the managed side of the business. So, again, Q4 is not going to be the results that we would like to see. And again, I think it's due to the financial situation out there and due to the fact that more and more customers are moving into self-serve. Some of those customers are moving to our self-serve, and it takes them a little longer to start spending to the same levels as it's something new for them. And I do believe we see the results in the future as well.” Q3 2023 call

It seems that this headwind is largely behind us, as spending is ramping up and management is not pushing clients to switch to self-serve as heavily if they are happy with managed services.

We should expect more variance going forward in terms of which business line is growing, due to the new growth strategy introduced by the new CEO.

The growth plan under the old CEO was just to grow self-service, which wasn’t really working. The results came in usually as self-service growing, managed declining, and exchange flat. The old CEO was trying to force Self-Service. Making statements like “It's not an easy transformation to change the DNA of the company, from the managed side of business to Self-Serve” and “The growth numbers are masked by the decline in our managed business. And we always communicated that we feel that the managed business is going to decline. But the value of illumin is illumin Self-Serve”

While the new CEO is saying: “With this customer centric approach, we're finding that more customers are seeing the value in utilizing both our managed service and illumin self-service products. That is what you are now starting to see in our revenue. These results also prove a point I made on prior calls where I discussed my view on managed services as an area where we could return to growth, moving our story from a single growth track to potentially multiple tracks of growth. The initiatives we have been implementing to refine our sales approach and reorganize our sales and marketing activities include a recommitment to managed services” and “At the core of our strategy is a commitment to supporting our customers in a flexible way as opposed to forcing them into one product”

Based on results, the new CEO's strategy is proving more effective, as the company has started growing instantly since he took over. In Q3 and Q4, all business lines grew while Q1 was more mixed, but still showed overall growth.

IlluminX=Exhance Services Reinvigoration

Source: https://illumin.com/company-overview/

On January 22nd, when Q4 and Q1 had not been released yet, the new CEO stated that the Exhance Services business had been neglected prior to his reign, at 13:10 in the video.

“third thing is is we had that third bucket if you remember from my first slide exchange services where we we work with the Publishers this is really a nancent side of the business and I asked a bunch of questions well hang on a sec it's still 20 some percent of our sales why is it so neglected so just being honest and so so we didn't put a lot of effort into exchange services yet this third piece but we got a lot of inbound demand over the last quarter or so and so we have seen a nice sort of steady opportunistic rise in exchange services”

They have been investing in this business in recent months, and the results are starting to show.

"Specifically, our exchange service business grew 148% over year to $12 million, reflecting the addition of new customers, expanding our partnership with new suppliers and investing in key technology enhancements to the platform as well as growing our customer support team. Experiencing measurable success in this area since the second half of last year has sharpened our focus and helped us concentrate more on this part of the business, leading to growth in this segment."

“we had a strong first quarter in terms of revenue growth. This was mainly led by outstanding growth in our Exchange Services business, which benefited from our targeting investments in this area.”

New Products and CTV

Source: https://ceo.ca/@GlobeNewswire/illumin-forecasting-smarter-campaign-planning-with

This was one of their investments that led to higher costs in Q1, and it’s now complete. The CEO thinks it’s going to bring in more customers(quotes from Q1 call):

“So when I think about AI forecaster and new customers, I think that it is a strong driver to bring in new customers.”

“And one of those absolutely critical features is an AI forecaster. This is a tool that is typically reserved. It is available elsewhere, but it is typically reserved for large upfront contracts and big commitments.”

“when we talk to these brands, these challenger brands are like, hey, if you had forecaster, we might flip you some of our business or we might switch all of our business, especially if we don't have to be beholden in tight times to a $5 million, $6 million, $4 million upfront commitment.”

“AI forecaster does put us in that game, first and foremost, but puts us in that game in a way that's much more customer-centric. It doesn't commit them to that big spend. So we think that's going to bring us new customers.”

This forecaster also helps their CTV offering, which they have highlighted as a source of growth. “We are also preparing to launch our new forecasting tool in Q2, which will add tremendous value to several channels, including CTV.”

Source: January 22, Illumin presentation

Outlook

"We are encouraged to see that the increased momentum in managed service in the latter half of Q1 continue into Q2,”

"We are now seeing a higher level of activity that continued from the second half of Q1, and we are working to build on this momentum and overcome the slower start to the year."

All the statements point to a better Q2 than Q1. And a better 2nd half of 2025 compared to the first half. They are expecting profitability to improve in the 2nd half, partly due to higher expenses in the first half, due to spending on investments like the forecasting tool that was released last month.

“This is consistent with what we said on our last earnings call that we expected to record higher expenses in the first half of the year, mainly from continued investment to enhance our product platform, strengthen brand identity as well as certain initiatives to increase our sales capacity, efficiency and focus by our enhanced account management team. This team will be focused on increasing client satisfaction, retention and incremental spend.

Along those lines, we also said we would expect more profitable third and fourth quarters once those investments were largely completed, and this view has not changed, assuming that the short-term headwinds we are experiencing related to tariffs and persistent macroeconomic uncertainty ease. We continue to believe in our long-term prospects and intend to remain focused on cost management and generating strong, sustainable revenue growth.”

“we are really just getting warmed up” ← This is huge.

They prefaced their bullish comments with warnings about the macroeconomic environment. We’ll see if they use macro as an excuse in case they don’t deliver, but they also said they won’t be using that as an excuse.

“From our point of view, we're a small company, and we have the opportunity to really drive our own performance. I think it is a tougher environment out there, but we're not using that as any sort of shield or excuse.”

One thing that raises my confidence is the large amount of insider buying in May by three different insiders. These are all board members.

.Source: https://ceo.ca/insiders-dashboard?symbol=illm&transaction=buy-sell

Illumin has also started buybacks again after a long pause. Further supporting the share price at current levels.

Source: https://ceo.ca/insiders-dashboard?symbol=illm&insider=illumin+Holdings+Inc.

Summary

I really like the current situation with Illumin stock at the moment. Macro fears and WeightWatchers restructuring took the stock down. The valuation is very cheap. The downside is limited due to high net cash and insider buying, and buybacks are providing support for the current share price. Q2 is expected to be better than Q1. The 2nd half is expected to be better than the 1st half. New features are being released, and previously neglected business lines are being reinvigorated. The new CEO is overhauling the marketing and sales strategy. I think this is a strong set-up for consistent growth and revaluation of the stock.

My favorite position to add to right now.

you still long after the post-earnings crash?

how do you compare it with zoomd?