Heartbeam: The Device

New pick(paywall removed)

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program which means I have a financial relationship with Seeking Alpha.

Mongolian short AD: THE LINK

Get a 7-day free trial and 30$ discount on your first year of Seeking Alpha Premium with my Affiliate link: AFFILIATE LINK

Heartbeam Basic info:

Source: Google

IPO late 2021 into a strong market for tech innovation stocks. The stock price has performed poorly since then due to delays for commercialization, delays for FDA permits, and the overall worse market for small-cap innovation stocks.

Market cap=66m USD

No debt

No revenue at the moment. Target for revenue 2nd half of 2025.

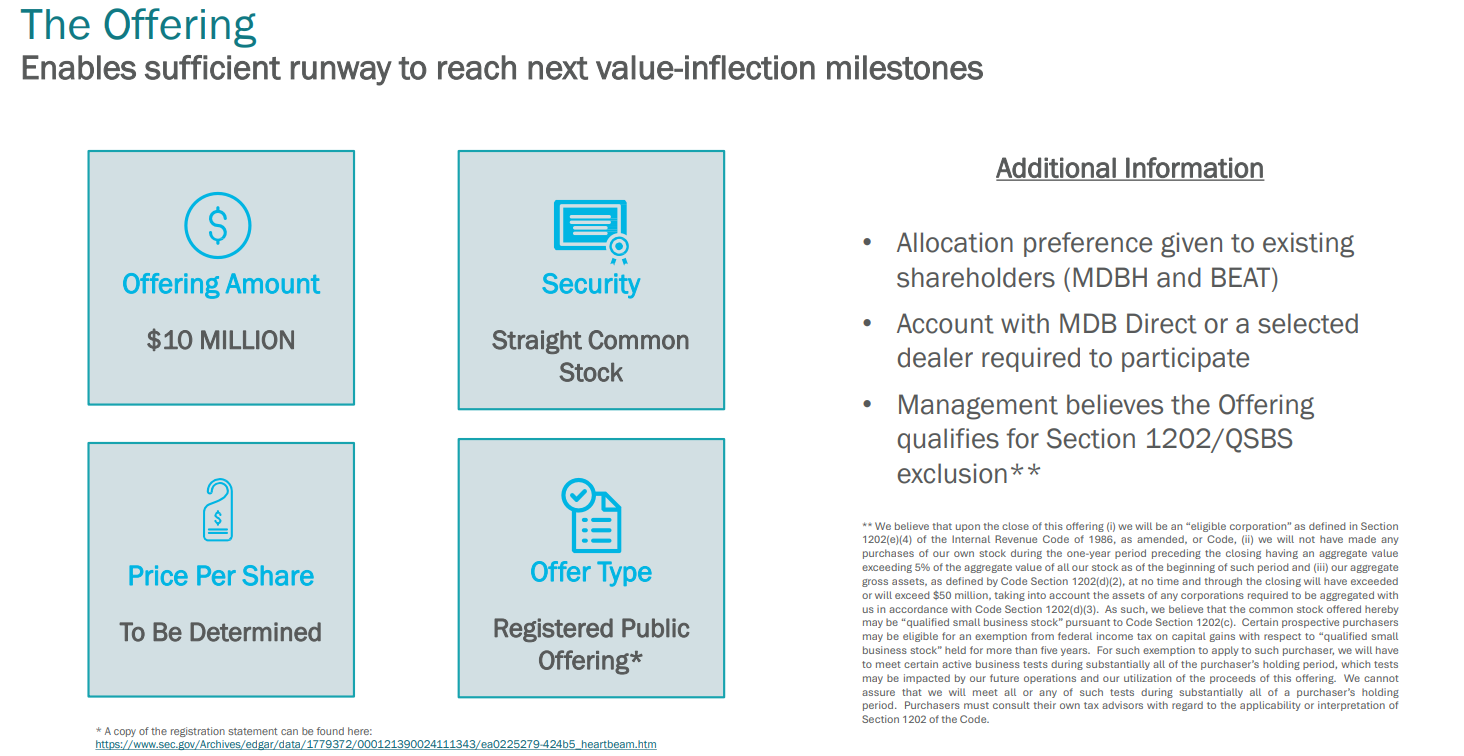

Recently raised $11.5 million USD (at $1.70, no warrants, oversubscribed). This raise should sustain them for about a year.

The total addressable market exceeds $ 100 billion USD.

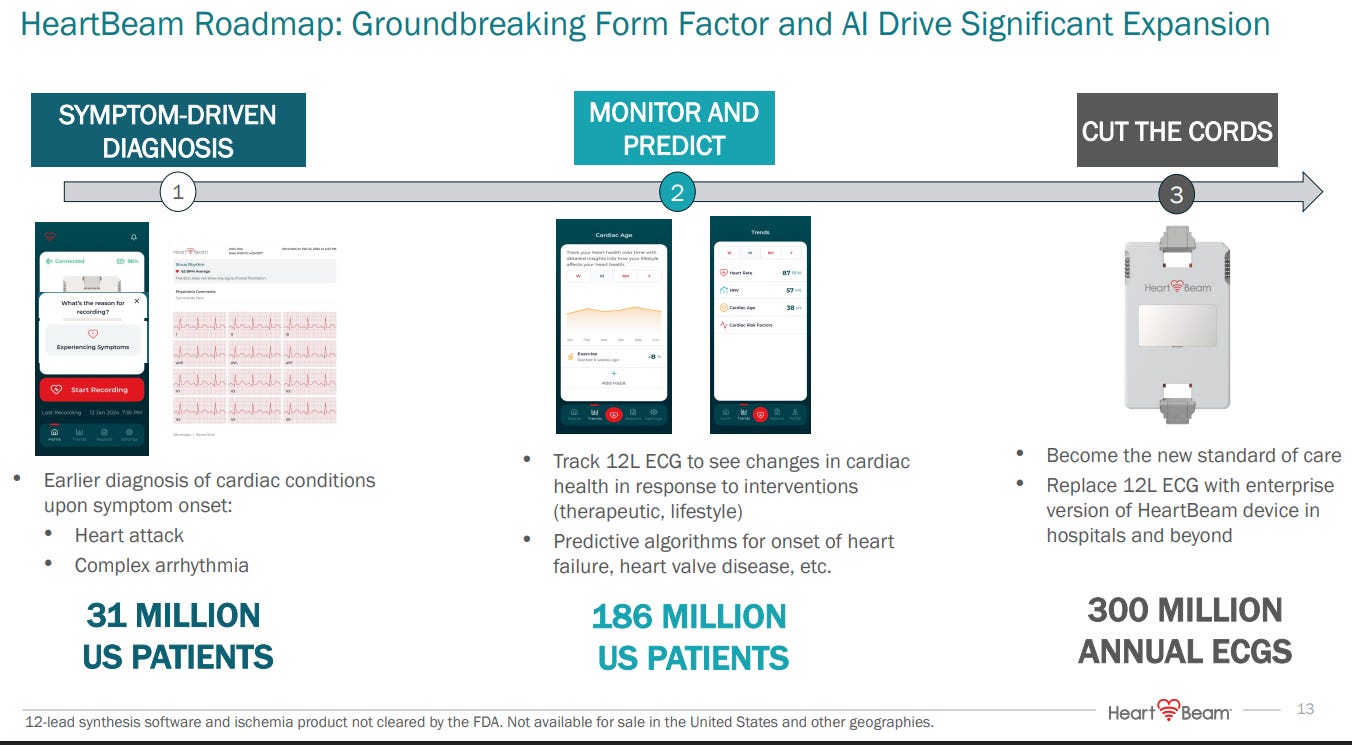

Heartbeam, the newest addition to The AlmostMongolian Portfolio, is my first healthcare stock and also my first heart attack-focused stock. Heartbeam has developed an innovative heart-monitoring device. The device is what this company and the investment thesis are all about, which means with this write-up, I will try to answer the following questions based on available information:

How does the device work?

What proof does Heartbeam have that the device works?

Is the device superior to the existing devices?

Is it permitted?

What is the plan for commercialization?

Who are the people owning and running Heartbeam?

In answering these questions, I have written the most comprehensive Heartbeam write-up on the internet.

To give you the basic idea of the thesis.

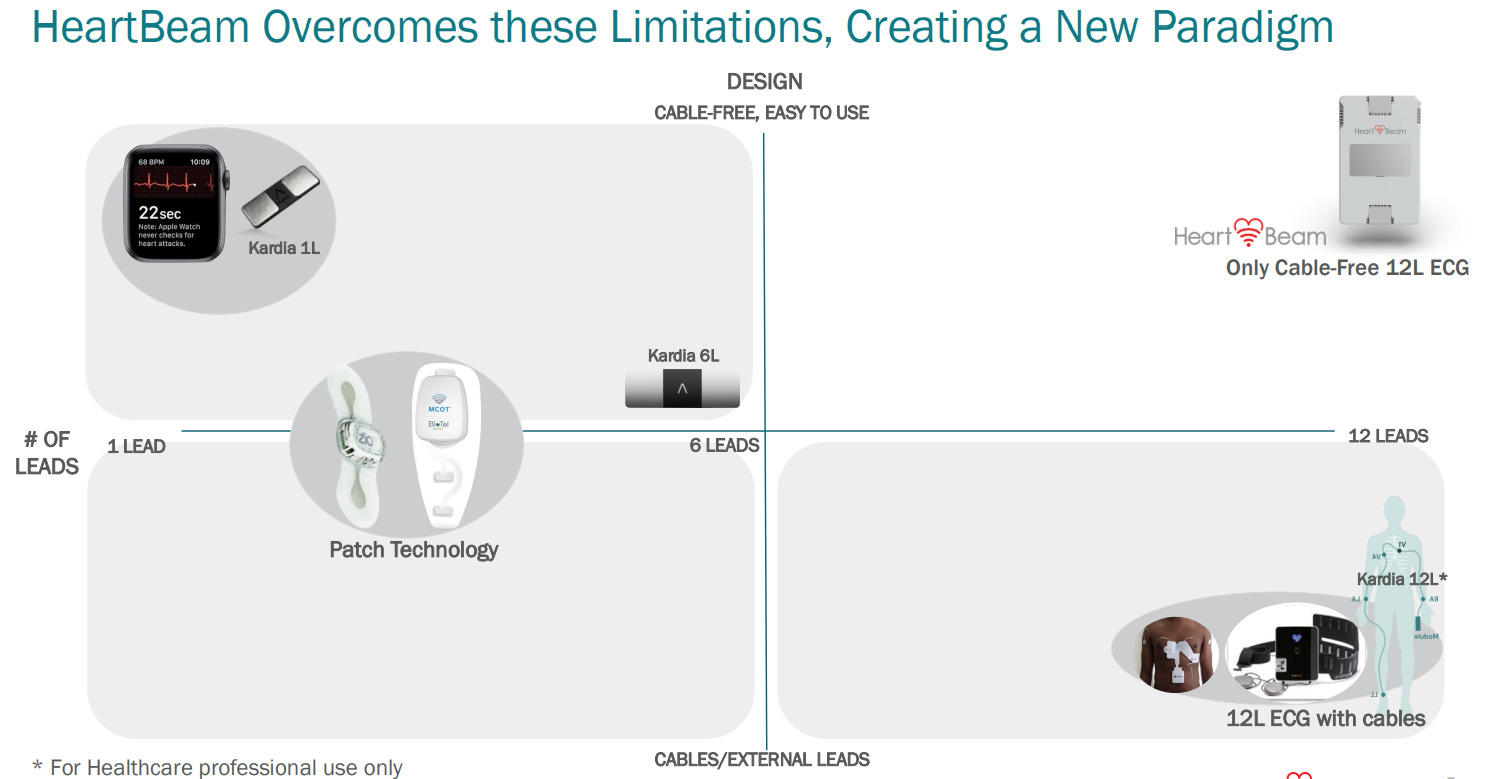

This is HeartBeam’s competition

Source: https://d1io3yog0oux5.cloudfront.net/_00cc34ec2f18b412abff79848819c77b/heartbeam/db/2293/21696/pdf/HeartBeam+investor+pres+03142025.pdf

The easy-to-use heart monitoring devices used at home and on the move are not accurate enough. Nobody who fears that their heart will brutally attack and murder them is solely going to rely on the Apple Watch. They will go to the hospital to obtain the best reading with a 12-lead ECG.

However, the current 12-lead ECGs are not practical for use at home or on the move due to the cables, size, and training required to use them properly. Just look at the standard 12-lead ECG on the right side of the picture. Imagine lying on a public beach or a park bench with that set-up, looking like you’re about to die any minute.

There is a demand in the market for a device that has hardware similar to the devices on the left side of the picture (easy to use, small) but with the capabilities of the device on the right side of the picture (accuracy).

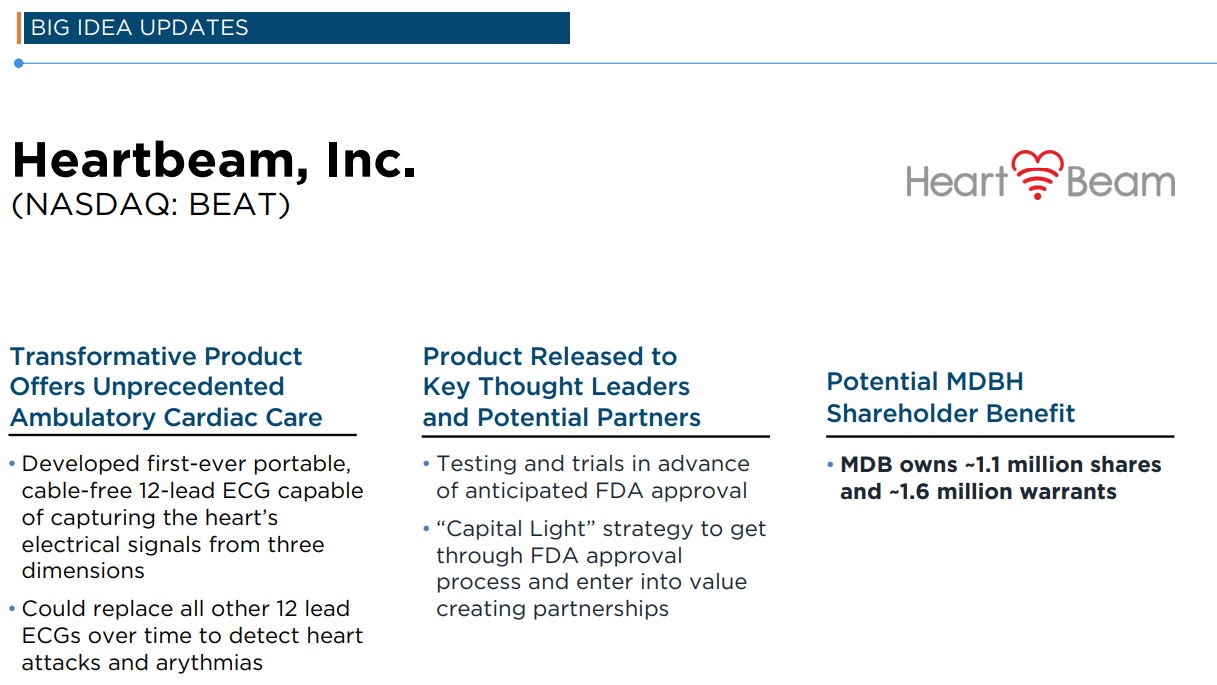

This is what HeartBeam has developed: the first-ever cable-free 12-lead ECG system, approximately the size of a credit card.

Source for 2 slides above: https://d1io3yog0oux5.cloudfront.net/_00cc34ec2f18b412abff79848819c77b/heartbeam/db/2293/21696/pdf/HeartBeam+investor+pres+03142025.pdf

This shows the competitive situation perfectly. Of course, the top-right is where you want to be, and it’s only Heartbeam in there. I didn’t just take their word for it; I tried to look for competitors online, but I didn’t find any other devices in the market or in development that could be placed on the top right.

Source: https://d1io3yog0oux5.cloudfront.net/_00cc34ec2f18b412abff79848819c77b/heartbeam/db/2293/21696/pdf/HeartBeam+investor+pres+03142025.pdf

Quick detour. Here, it says 17 patents. Their March 2024 PR states that they hold 14 patents in the US and 4 internationally. Using my calculator, I calculated that this translates to a total of 18 patents. I don’t know what happened to that 1 patent.

But we don’t need to obsess over that 1 patent. Overall, they have a vast patent collection.

They are also looking to expand it. That same press release also states that they have 20 pending patent applications worldwide. The whole world.

Here is the demo for the HeartBeams device. It’s very easy to use and fast to use.

Source: https://ir.heartbeam.com/

They have an app, which means recurring revenue. The average user will be old, so it’s crucial that the app is easy to use, and as you can see from the video, it is. You just put the device where your heart is (if you don’t know, the app will tell you) and press start recording. It takes 30 seconds to get the results. The results are sent to the patient's cardiologist, and within 24 hours, the patient should receive a response from the cardiologist.

The app also provides an option to speak with a cardiologist immediately for $65.

Source: https://ir.heartbeam.com/

The competition, which is the cabled 12-lead ECGs performed mostly in hospitals, takes 10-15 minutes, not accounting, of course, for the time it takes to go to the hospital.

Quick demand outlook:

We all know that our heart becomes our greatest enemy as we age. According to the World Health Organisation around 30% of global deaths are due to cardiovascular diseases. And it’s the leading cause of death globally. The population is getting old in rich countries(Heartbeam’s first target market). The demand for this kind of product is strong and will get stronger.

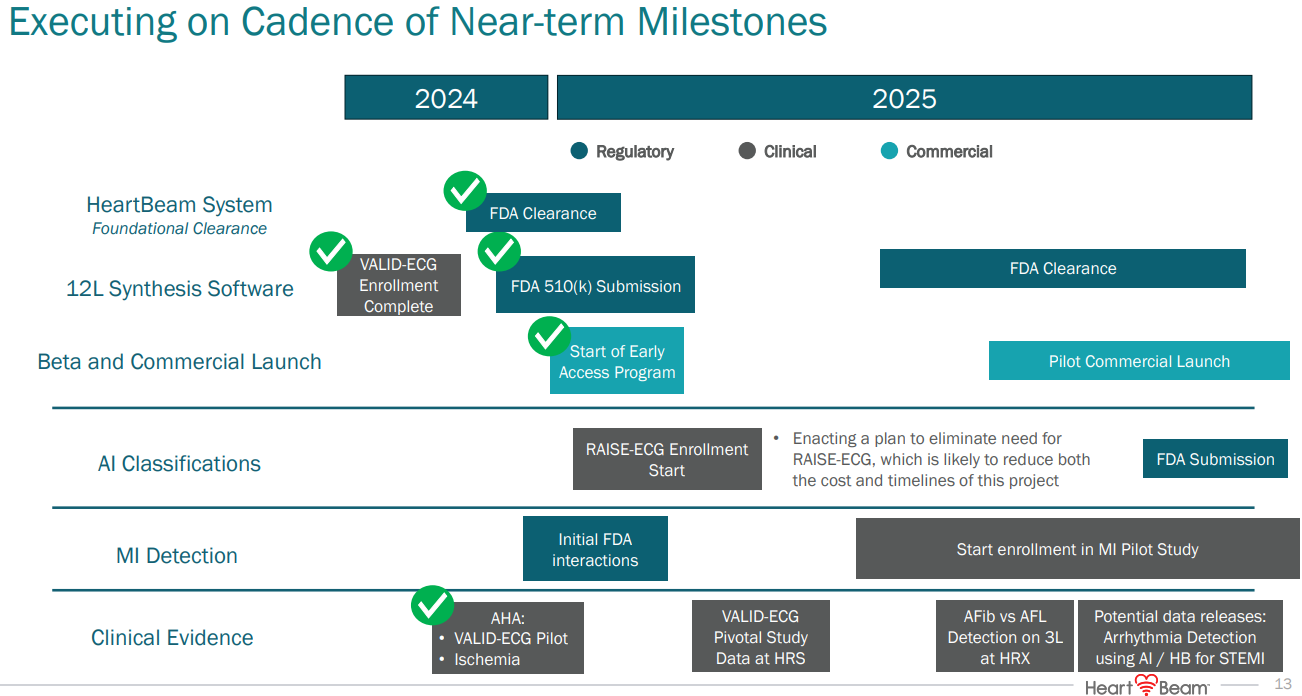

FDA approvals and submissions

Before commercialization, Heartbeam needs FDA clearance for its products.

They need two crucial FDA approvals. 1 for the hardware and 1 for the software.

FDA approval for the hardware was granted in December 2024, and the FDA submission for the software was submitted in January 2025.

Source: https://ir.heartbeam.com/news-events/press-releases/detail/83/heartbeam-announces-fda-clearance-for-at-home

This is already very important because it serves as a crucial piece of validation for the technology. FDA 510(k) clearance means that the product is deemed safe and effective for its intended purpose.

The purpose, as stated in the PR, is a “comprehensive arrhythmia assessment.”

arrhythmia=abnormal heart rhythm

This FDA clearance also means the product can be sold. The question then arises as to why they are not selling it yet.

“Our first webcast question asks, congratulations on receiving their first FDA clearance, what went into your decision to not immediately commercialize upon clearance.

Rob Eno

Yes, I'll take that one. So just to recap, our initial clearance is for the system with the three-lead output and the second submission is the 12-lead Synthesis Software. And we just think it's important that we initially commercialize with the 12-lead software, which is really where we think the differentiation is from a physician and a patient perspective. So we're using this time after the initial clearance while waiting for that second clearance to fully prepare for commercialization with the Early Access Program. Hope that helps.” Q4 earnings call transcript

Source:https://d1io3yog0oux5.cloudfront.net/_00cc34ec2f18b412abff79848819c77b/heartbeam/db/2293/21696/pdf/HeartBeam+investor+pres+03142025.pdf

In summary, There are two pieces that both need FDA approvals for optimal commercialization.

FDA approved is the device that “collects signals in 3 directions, capturing the totality of heart’s electricity signals”

FDA submitted “Signals from 3 directions train HeartBeam’s AI algorithms and are synthesized into 12L ECGs using a personalized transformation matrix”

Source: https://ir.heartbeam.com/news-events/press-releases/detail/85/heartbeam-achieves-major-milestone-with-fda-submission-for

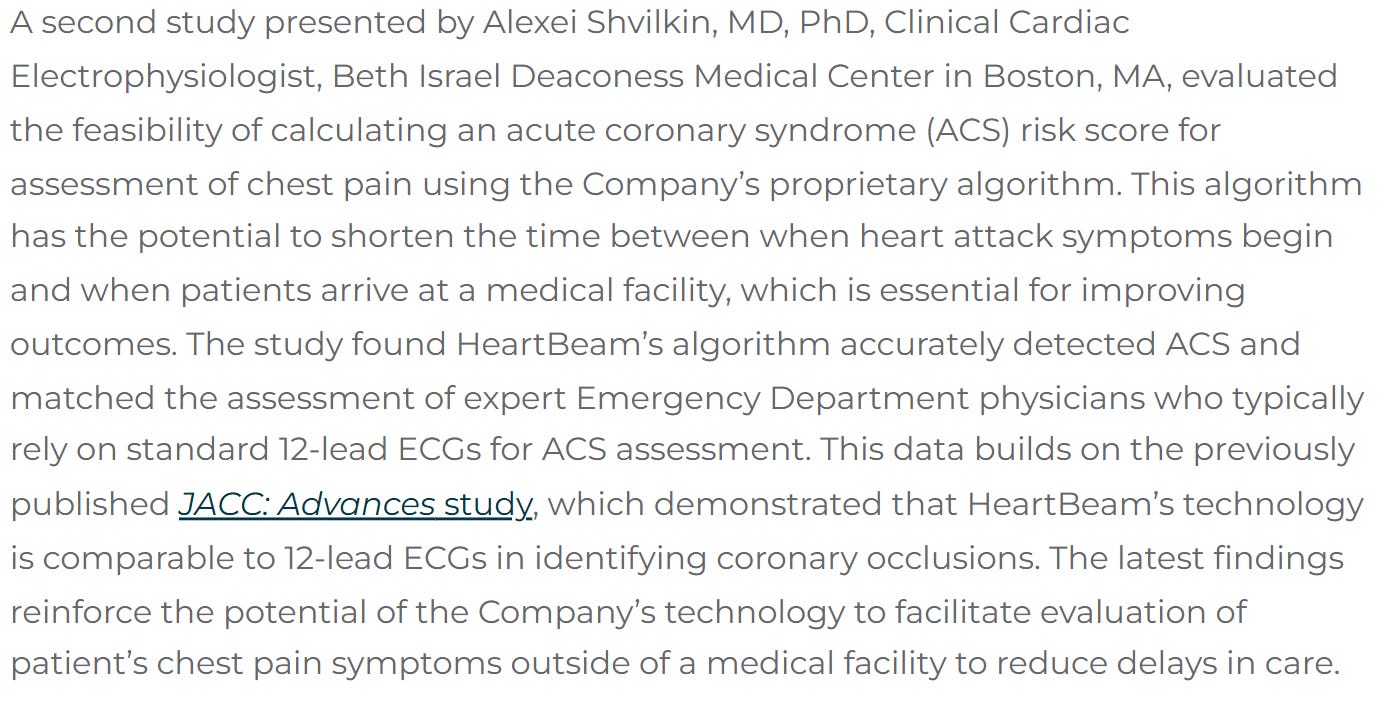

In terms of near- and mid-term catalysts, this second FDA clearance is the biggest one. It would be a big de-risking event, and If they obtain it, the company will be ready to proceed with full commercialization. Based on existing studies, the first FDA approval, and blind trust, I believe it’s highly likely that the software will receive FDA clearance; however, it’s always a possibility that it won’t, which is one of the risks associated with this stock.

When?

“Next question asked, when is the expected clearance time from FDA for the second clearance?

Rob Eno

Yes, it's always challenging and even in today's environment, particularly so in predicting the timing of FDA reviews and clearances. We're estimating that we'll receive the clearance before the end of the year, but right now, it's a little early for us to give any more specific guidance with that.

I'll just add that we have excellent relationships with FDA. We feel good about our submission. We held two pre-submission meetings with FDA to specifically talk about the design of the VALID-ECG study. And then as we've mentioned, we're encouraged by the results of the VALID-ECG study, which will be the main focus of the application and also those results will be presented publicly at the end of April.” Q4 call

They mention the VALID-ECG study and that they are encouraged by the results that will be presented at the end of April. This is likely our most near-term catalyst, as it is a more important study than usual because this study is a component of this FDA submission, which means if the results are positive, as they are indicating with ” encouraged,” the FDA clearance is highly likely. My confidence is further increased by the fact that they conducted a smaller study using the same protocol, which yielded good results.

I delve into this study further in the studies section of the article.

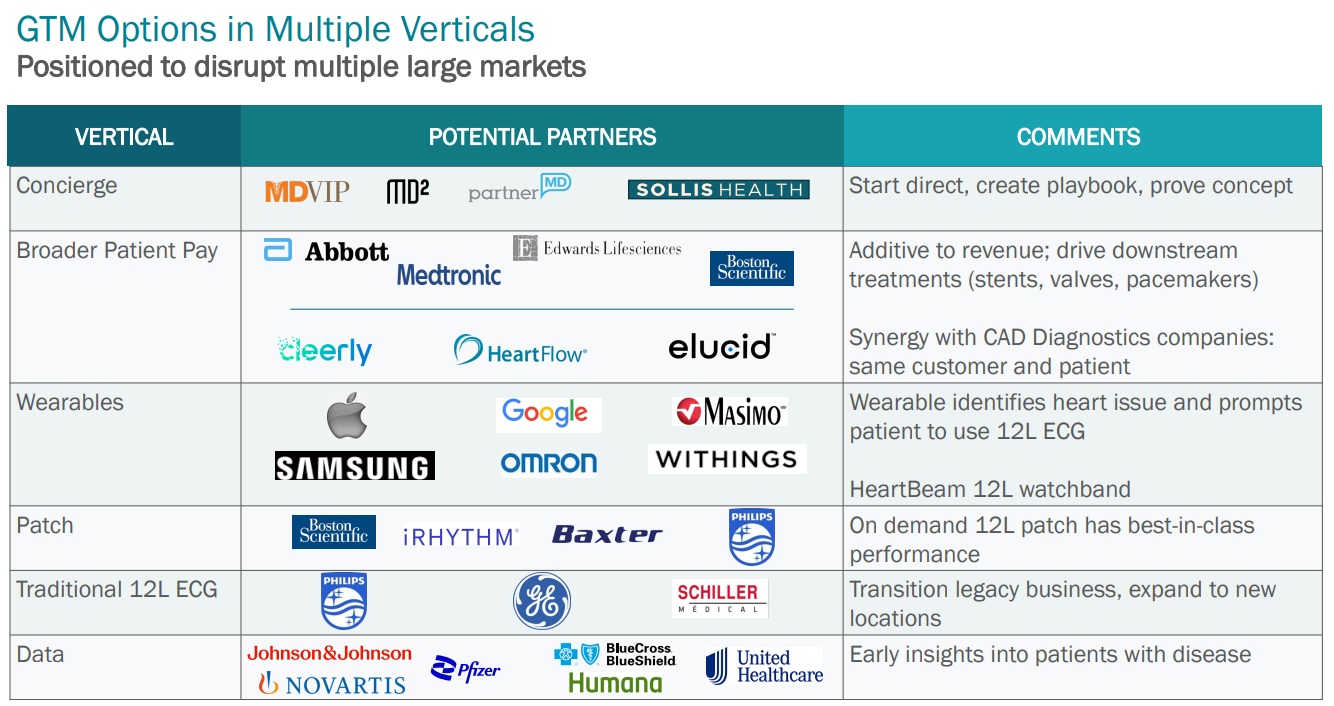

Commercialization Strategy

There is considerable uncertainty surrounding how the commercialization will unfold. This is a small company with just “approximately 20 employees” going after large markets. They are going to need partners with manufacturing, marketing, clinics prescribing their device, etc. I would say the stock will have already increased by a decent amount if they even reach this point, so this is not the most relevant issue at the moment. It’s very relevant if this becomes a long-term hold, and ideally, that is what I would prefer.

Source:https://d1io3yog0oux5.cloudfront.net/_00cc34ec2f18b412abff79848819c77b/heartbeam/db/2293/21696/pdf/HeartBeam+investor+pres+03142025.pdf

Right now Heartbeam is doing an early access program in preparation for commercialization in the second half of the year.

Quotes from Q4 earnings call:

“we commenced our Early Access Program in Q1 2025 and the intent of this program is to learn in preparation for our pilot commercialization, which we plan to initiate after we receive FDA clearance for the 12-lead Synthesis Software.

The goals of the Early Access Program include refining the clinical workflows, establishing operational readiness, validating our commercial messaging and marketing materials and creating a strong funnel of early adopter sites. By laying this groundwork and using this time to optimize these areas, we anticipate being able to maximize the impact of our pilot commercialization.”

“Of note, we're extremely encouraged by the inbound interest with hundreds of physicians and potential patients joining the waiting list.” Talking about the early access program

“And our last question asks, can you give us more details on the Early Access Program?

Rob Eno

Sure. So I described in the main part that the objective is really we're trying to evaluate our offering on a number of levels and prepare for commercialization. So we're going to focus on things like patient onboarding, training and the whole end-to-end clinical workflow, but also we're going to be establishing things like customer service operations and relationships with an outside physician reader service and those associated workflows. We're going to take this opportunity to evaluate our marketing message and materials and also build out a funnel of early adopter centers.

And then in terms of scope, we're going to work with a number of centers, and we anticipate including hundreds of patients in this program.”

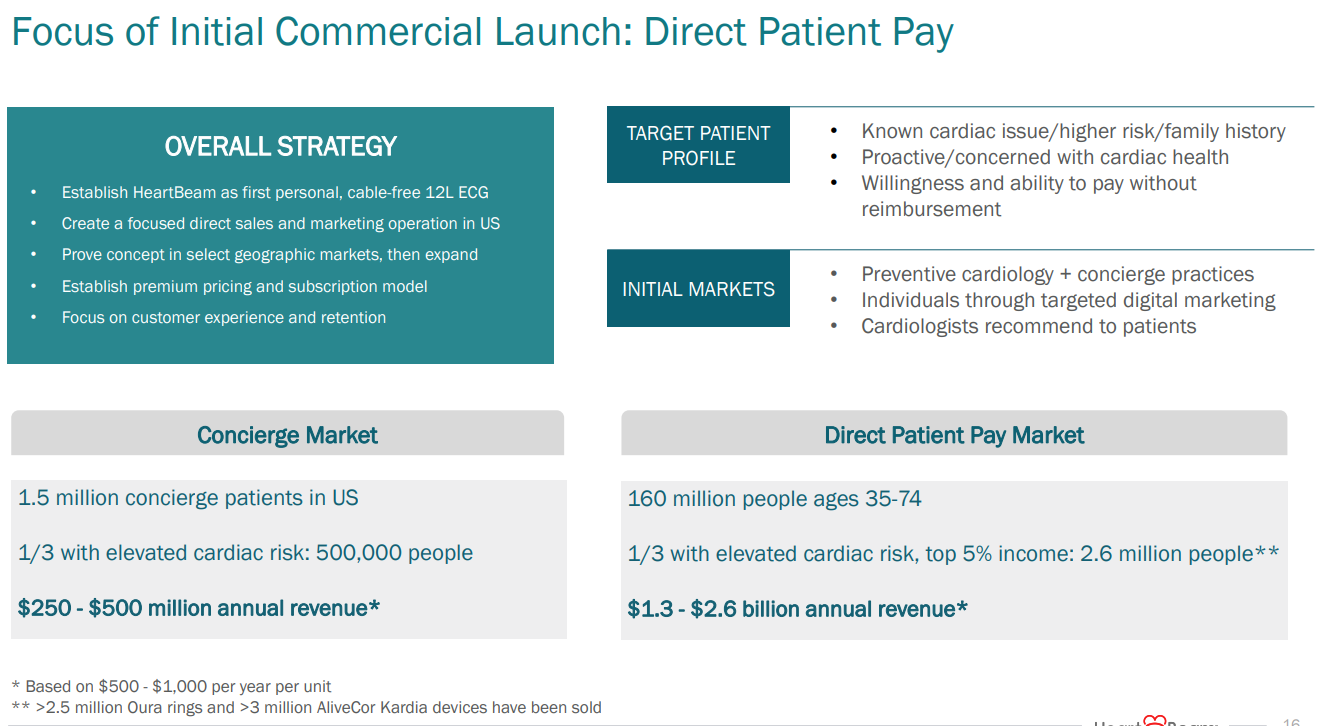

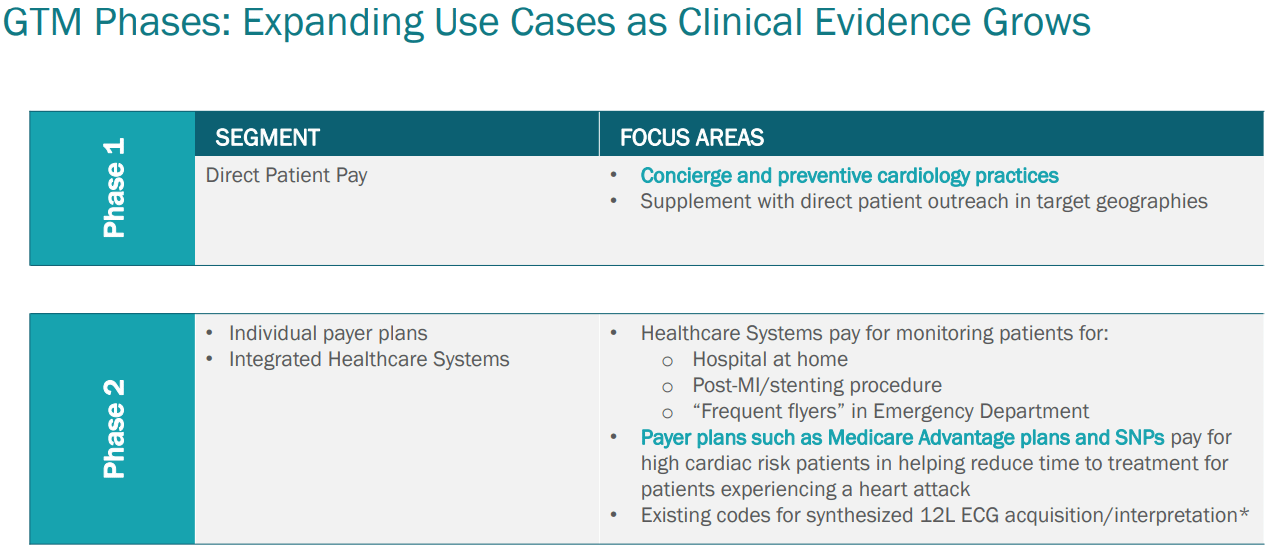

The first markets Heartbeam is going for consist primarily of wealthy older people. Direct patient pay market and Concierge market in the US.

Direct pay is self-evident. The concierge market in the US is when people pay a yearly/monthly fee to have direct access to a doctor with enhanced/personalized care. This costs thousands of dollars yearly.

“We're planning to start with what we're referring to as Direct Patient Pay, specifically patients paying for the system outside of reimbursement. This is largely a section that we can reach through concierge and preventive cardiology practices, but at the same time, supplement this by targeting individuals in select geographic areas through digital marketing. We've conducted extensive market research with patients and concierge practice and validated that there's a strong market need for the HeartBeam technology in this market segment. So that's Phase I.” Q4 earnings call

It makes sense to start with wealthy people. This demographic will want the best at-home and on-the-go device in the market and won’t care as much about the cost. They are already spending thousands of dollars annually on healthcare.

They haven’t disclosed the cost of the device yet.

They haven’t also said how much the app will cost annually/monthly.

What they state is “establish premium pricing and subscription model”.

From that, I can speculate that premium pricing means maybe the device’s initial purschase cost is 500-1000$ and the subscription model tied to the app may be 100-200$ per year, but with potential add on’s like paying for the immediate calls with the cardiologist could increase it a lot depending on what is the Heartbeam’s cut. Pure speculation.

Source: https://d1io3yog0oux5.cloudfront.net/_00cc34ec2f18b412abff79848819c77b/heartbeam/db/2293/21696/pdf/HeartBeam+investor+pres+03142025.pdf

Next question asked. Are you planning to initially commercialize this technology alone or with a partner?

Rob Eno

Yes. Another great question. We've talked about previously that we are assessing all options, and we're very much open to partnerships, and there are so many different opportunities here that we want to take advantage of partnerships. So we certainly are continuing discussions along those points.

What we are planning to do is do our initial pilot commercialization, as I described in these two pilot markets with our own team, a small and focused direct sales and marketing organization. And in our opinion, there's really two reasons for that. The first is we want to demonstrate that the demand that we see is real. And second, in a sense that we understand and can implement the playbook in order to market and sell a novel technology like this. And then with that, we'll have options in our hands about expanding that internal effort and/or working with partners in various areas.” Q4 earnings call

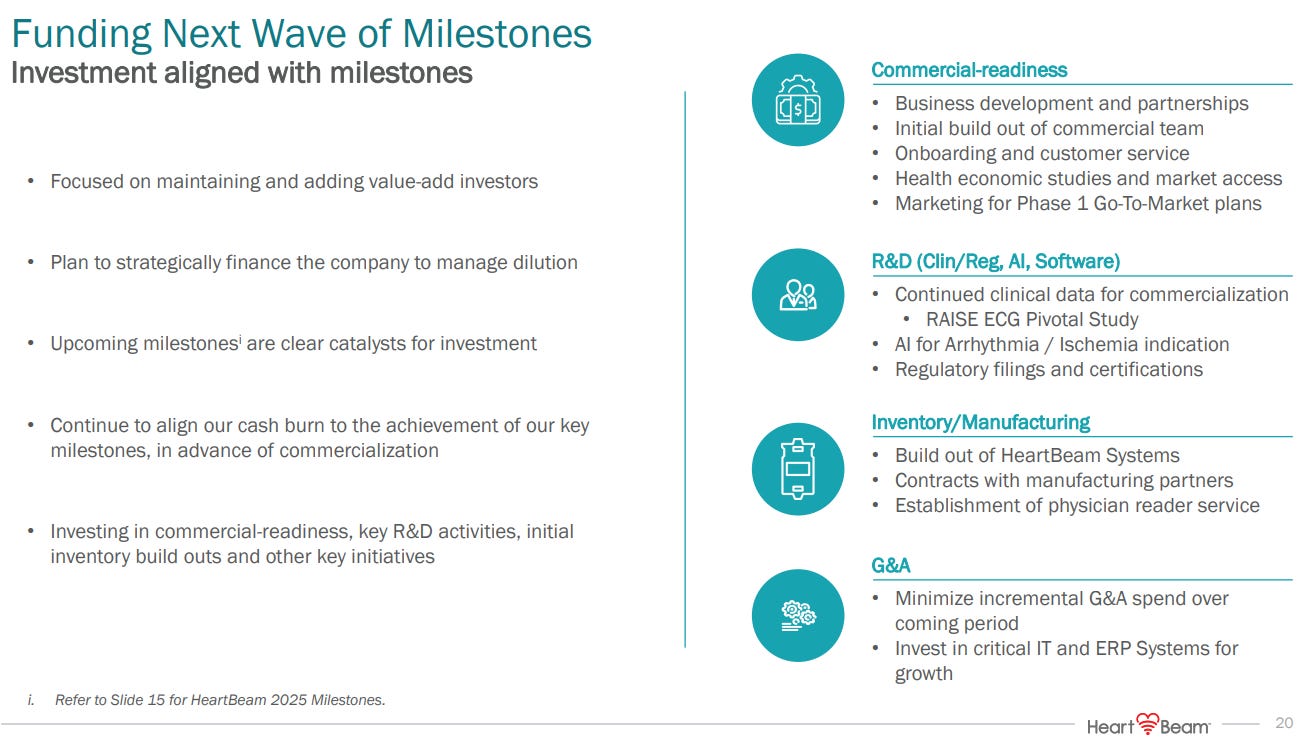

Here is a slide outlining the general preparations for commerialication.

Source: https://d1io3yog0oux5.cloudfront.net/_00cc34ec2f18b412abff79848819c77b/heartbeam/db/2293/21696/pdf/HeartBeam+investor+pres+03142025.pdf

Build inventory, minimize incremental G&A, and even AI in the mix. Good stuff. I don’t disagree with any of that.

Source for 2 above slides: Heartbeam corporate presentations

The next phase is to target these larger markets, but I assume this would be years away. This is what increases the total addressable market above 100 billion USD. The entry into these markets will be more in focus if Heartbeam is still in my portfolio after many years. Currently, these larger markets are not as relevant. If Heartbeam is successful in the concierge and direct patient pay markets, the stock would likely have more than 10x its current value by that point, considering these markets are themselves multi-billion-dollar revenue opportunities.

Studies

First, let’s continue from where we left off in the FDA section with the VALID-ECG study, as this is the most important study happening at the moment.

ECG (electrocardiography) is a test that produces a recording, also known as an ECG (electrocardiogram), which is a type of chart that has been shown in pictures in this article, featuring lines that indicate heart activity.

The following quotes are from this PR: https://ir.heartbeam.com/news-events/press-releases/detail/82/heartbeam-announces-positive-data-from-two-studies-at

The VALID-ECG Study will enroll a total of 198 patients presenting with a variety of underlying cardiac conditions at up to five US sites. All patients enrolled in the study will receive simultaneously recorded ECGs from a standard 12-lead ECG machine and the HeartBeam AIMIGo system.

The primary objective of the study is to demonstrate the equivalence of ECG waveforms between the AIMIGo synthesized 12-lead ECG and a standard 12-lead ECG by analyzing key ECG parameters called amplitudes and intervals. The study will also examine the accuracy of physician diagnosis for various arrhythmias with the AIMIGo synthesized 12-lead ECG, compared to a standard 12-lead ECG.

HeartBeam’s 510(k) submission for the credit card-sized AIMIGo system is currently being reviewed by FDA. This application is for the entire 3D VECG system, which consists of the AIMIGo device, the patient application, the physician portal, and the wireless communications between them. The company expects that, when cleared, this would be the first FDA clearance for a handheld VECG system.

The VALID-ECG study will be a component of HeartBeam’s subsequent 510(k) submission, which will focus on the algorithms that take the 3D VECG signal and synthesize a 12-lead ECG, providing physicians with a visual representation of the gold standard ECG output. HeartBeam expects enrollment of the VALID-ECG study to be complete in Q2 2024.

“The initiation of the VALID-ECG study is a major milestone for the company and a reflection of our commitment to provide a strong foundation of clinical data as we strive to provide patients and physicians with the ability to accurately monitor cardiac disease outside of a medical facility,” said Branislav Vajdic, PhD, CEO and Founder of HeartBeam. “In addition, our product pipeline includes coupling AI with our data-rich 3D VECG technology which will enable us to extract unique information and longitudinal insights to transform how cardiac care is monitored in the future.”

The company has already completed an 80-patient pilot study using the same protocol as the VALID-ECG study. The company anticipates presenting the results of the pilot study at a scientific meeting in the second half of 2024. HeartBeam will also present data on its deep learning algorithm at two prestigious Electrophysiology conferences in Q2 2024.

The results of the 80-patient pilot study have been released.

The first presentation by Thomas Deering, MD, FACC, FHRS, Chief of Arrhythmia Center, Piedmont Healthcare in Atlanta, GA, highlighted results from an 80-patient pilot study, which evaluated the performance of HeartBeam’s synthesized 12-lead ECG waveforms compared to simultaneously collected standard 12-lead ECGs for arrhythmia detection. The study found excellent agreement when physicians diagnosed various arrhythmias utilizing the HeartBeam synthesized 12-lead ECG compared to a standard 12-lead ECG (Sensitivity: 94%, Specificity: 100%). Arrhythmias evaluated include sinus rhythm, atrial fibrillation, atrial flutter, and sinus with premature ventricular contraction (PVC) or premature atrial contraction (PAC). This study is a precursor to the Company’s pivotal study, VALID-ECG, which completed enrollment in June. VALID-ECG will support the clinical equivalence basis for the synthesized 12-lead ECG software in the Company’s next FDA submission.

“One of the main challenges with timely assessment of arrhythmias is that a single-lead ECG does not contain complete diagnostic information, and at the same time, obtaining a standard 12-lead ECG is highly impractical outside of a medical setting,” commented Dr. Deering. “Our study showed that the synthesized 12-lead ECG obtained from the HeartBeam device is similar to a 12-lead ECG, allowing patients to easily obtain the highest fidelity ECG data wherever they are upon symptom onset and greatly reduce any potential delays in receiving care.”

That’s a lot of words, but from this whole thing You just need to combine 3 sentences from different parts:

“The VALID-ECG study will be a component of HeartBeam’s subsequent 510(k) submission” Referring to the second FDA submission for the software

“The company has already completed an 80-patient pilot study using the same protocol as the VALID-ECG study.”

“Our study showed that the synthesized 12-lead ECG obtained from the HeartBeam device is similar to a 12-lead ECG” referring to the 80-patient study

First of all this is another piece of proof that the Heartbeam is comparable to the cable monster. Secondly, the 80-patient study had good results and it was done with the same protocol as the VALID-ECG study which is a component of the second FDA submission it gives a strong signal that Heartbeam is very likely to get the FDA clearance which is the biggest catalyst for the company.

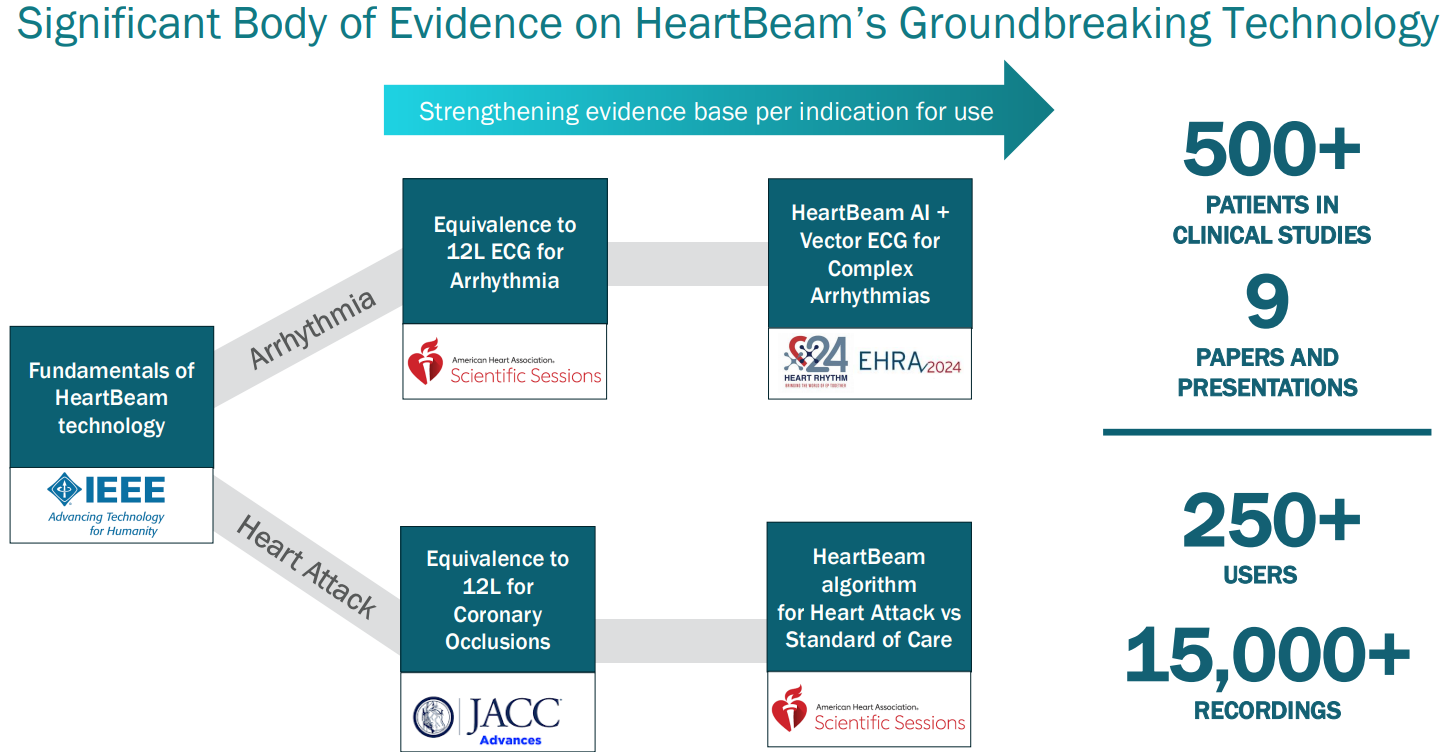

What other scientific evidence is there for Heartbeam?

Source for 2 slides above: https://d1io3yog0oux5.cloudfront.net/_00cc34ec2f18b412abff79848819c77b/heartbeam/db/2293/21696/pdf/HeartBeam+investor+pres+03142025.pdf

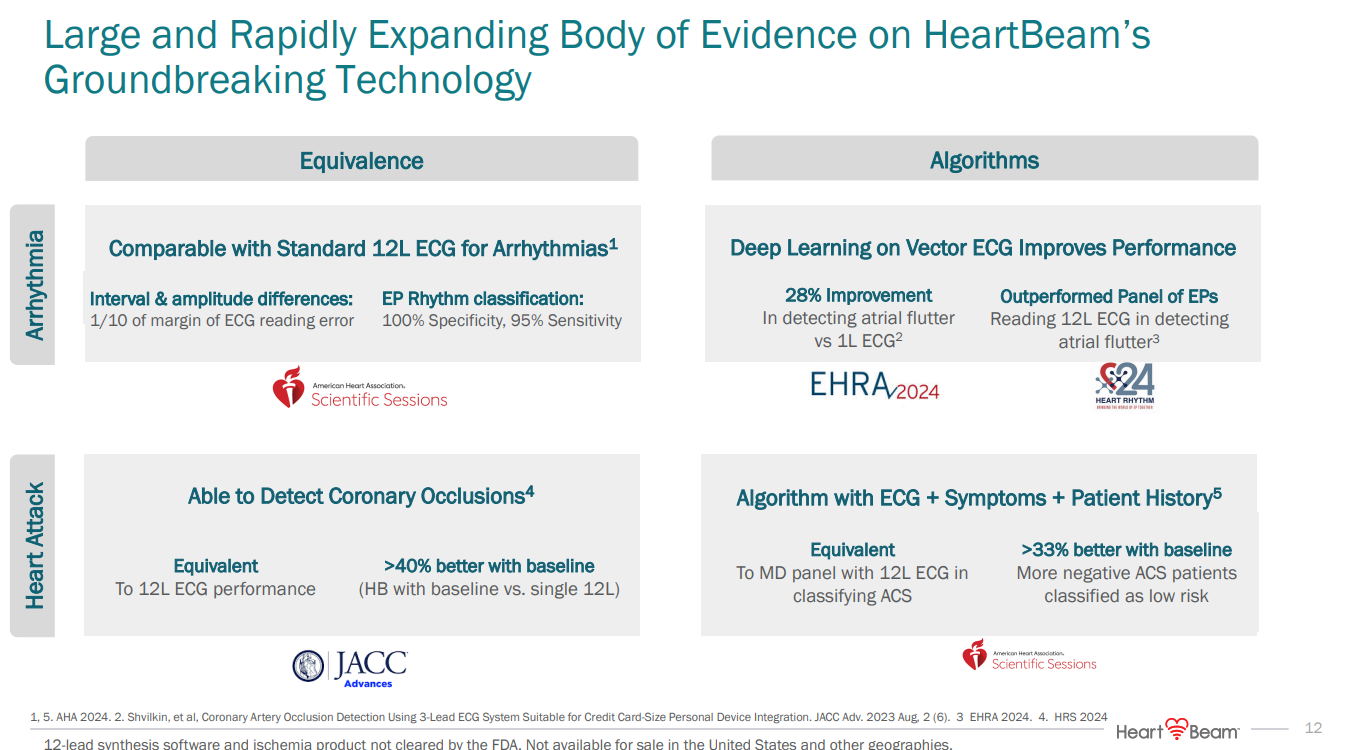

Let’s look at some of these studies. Heartbeam’s promise is not at this point that it’s more accurate than standard 12L, but that it’s comparable in accuracy, and has other features that are way superior to it. Any result that shows Heartbeam’s tech to be comparable is a positive outcome.

JACC advances study on the ability to detect coronary occlusions(66 patients)

Coronary occlusion is a partial or complete blockage of blood flow of an artery.

The objective:

The purpose of this study was to compare the accuracy of coronary occlusion detection using vectorcardgiographic analysis of a near-orthogonal 3-lead ECG configuration suitable for credit card-size personal device integration with automated and human 12 lead ECG interpretation

Conclusion:

Vectorcardiographic ST-segment analysis using baseline comparison of 3-lead ECG system suitable for credit card-size personal device integration is similar to established 12-lead ECG methods in detecting balloon coronary occlusion.

This was the reason for studying this :

“Early coronary occlusion detection by portable personal device with limited number of electrocardiographic (ECG) leads might shorten symptom-to-balloon time in acute coronary syndromes.”

Symptom-to-balloon time refers to the total duration from the onset of heart attack symptoms (for example chest pain) to the moment a blocked coronary artery is reopened using a balloon angioplasty during primary percutaneous coronary intervention.

What we can conclude here is that using the device people can get to the balloon faster which could save their lives.

There is a another study that was mentioned in this the same PR as the 80-patient study that supposedly builds on this JACC Advances study. This hasn’t been published yet, but according to the PR it also had good results.

Source: https://ir.heartbeam.com/news-events/press-releases/detail/82/heartbeam-announces-positive-data-from-two-studies-at

I’m not covering every study in this article as it would take a very long time.

Here are the links to the studies with a little explanation included from Heartbeam’s website:

Arrhythmia Detection:

{kind=link}

“Pilot data demonstrating similar performance between HeartBeam system and 12-lead ECGs for arrhythmia detection”

“Outperforms single-lead ECG in detecting atrial flutter”

“Outperforms expert panel of electrophysiologists in detecting atrial flutter”

Heart Attack detection:

“Highlights potential of HeartBeam’s technology with a novel risk-assessment algorithm to evaluate chest pain remotely”

“Shows HeartBeam technology is comparable to 12-lead ECG in identifying coronary occlusions”

Technology validation:

“Validates synthesis of 12-lead ECG from HeartBeam’s vector-based approach using a personalized transformation matrix.”

“A Morphology-Preserving Algorithm for Denoising of EMG-Contaminated ECG Signals”

“Validates HeartBeam’s method of removing noise from ECGs while preserving morphology.”

“A Database of Simultaneously Recorded ECG Signals With and Without EMG Noise”

“Validates HeartBeam’s novel acquisition method that allows for direct recording of ECG signals.”

They also have won awards. Another piece of validation.

Source: https://d1io3yog0oux5.cloudfront.net/_00cc34ec2f18b412abff79848819c77b/heartbeam/db/2293/21694/pdf/BEAT+Q4%2724+Financial+Results+Conference+Call+Presentation-3-13-2025-Final.pdf

Two last year and one already this year (Pinnacle Awards).

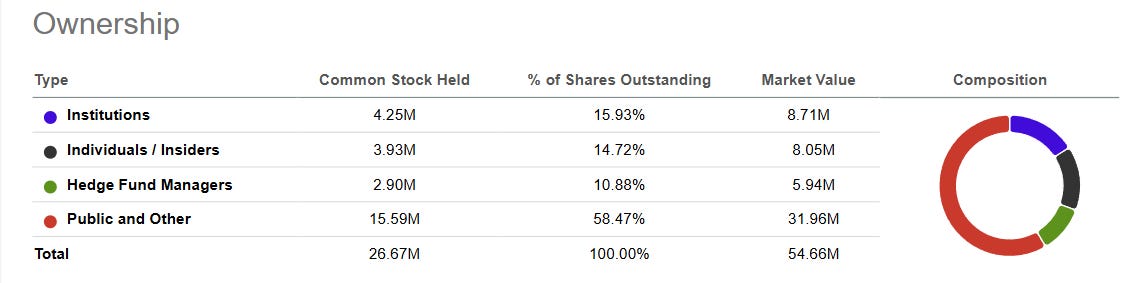

Shareholder base

For a stock like this, the shareholder base is particularly important because they are a small-cap pre-revenue innovative technology company. If you have a large-cap health insurance company or a multinational retail chain, for example, do you really care whether insider ownership is 1% or 10% or what institutions own the stock? Not really, the company is what it is. It’s not completely meaningless. But it’s not something you really focus on with a company like that.

However, with stocks like Heartbeam and another small-cap pre-revenue innovative tech company in the AM portfolio, Aduro, it is very important to consider the shareholder base. If you have a “transformational” or “game-changer” technology on your hands with a very small market cap and some crazy total addressable market, and the insider ownership is only 2%, it will definitely make anyone doubt the merits of the technology.

A stock like this is already very risky, and if the insiders are not willing to make a large investment, it raises serious doubts. Also, as generalist investors, we can never understand the technology as well as the professionals in the industry, so we want to see the professionals, the scientists, and the PhDs developing the product invested.

As we know, Aduro has insider ownership of 39%. The % has gone down due to capital raises. When I started investing in it it was almost 50%. This was one of the big reasons why I was willing to invest in it or even take a serious look at it considering the type of stock it was.

Heartbeam technology is more proven than Aduro’s which is why I won’t need quite as high of an insider ownership. The idea here is that if there is uncertainty about the commerciality of technology I need to rely more on just trusting what the company is saying and for me to trust(never 100% trust) them I need to see them heavily invested.

Heartbeam has an insider ownership of 14.72% according to Seeking Alpha.

Source: Seeking Alpha Premium

14.72% is not amazing, but it’s not bad. 8m USD investment from the insiders. I would say the insider ownership is adequate, but I would like it to be higher.

There is one very noteworthy shareholder and I found this stock through looking at their investments.

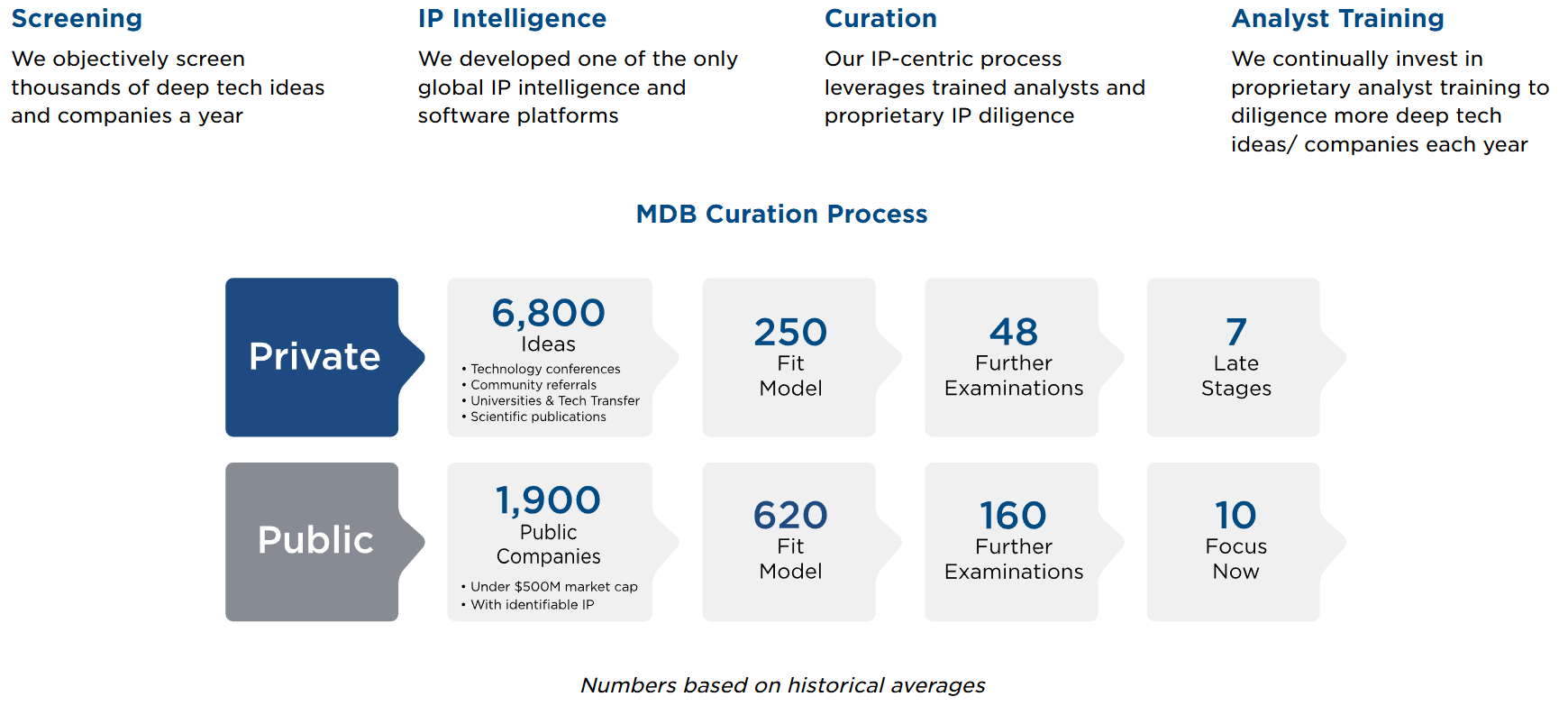

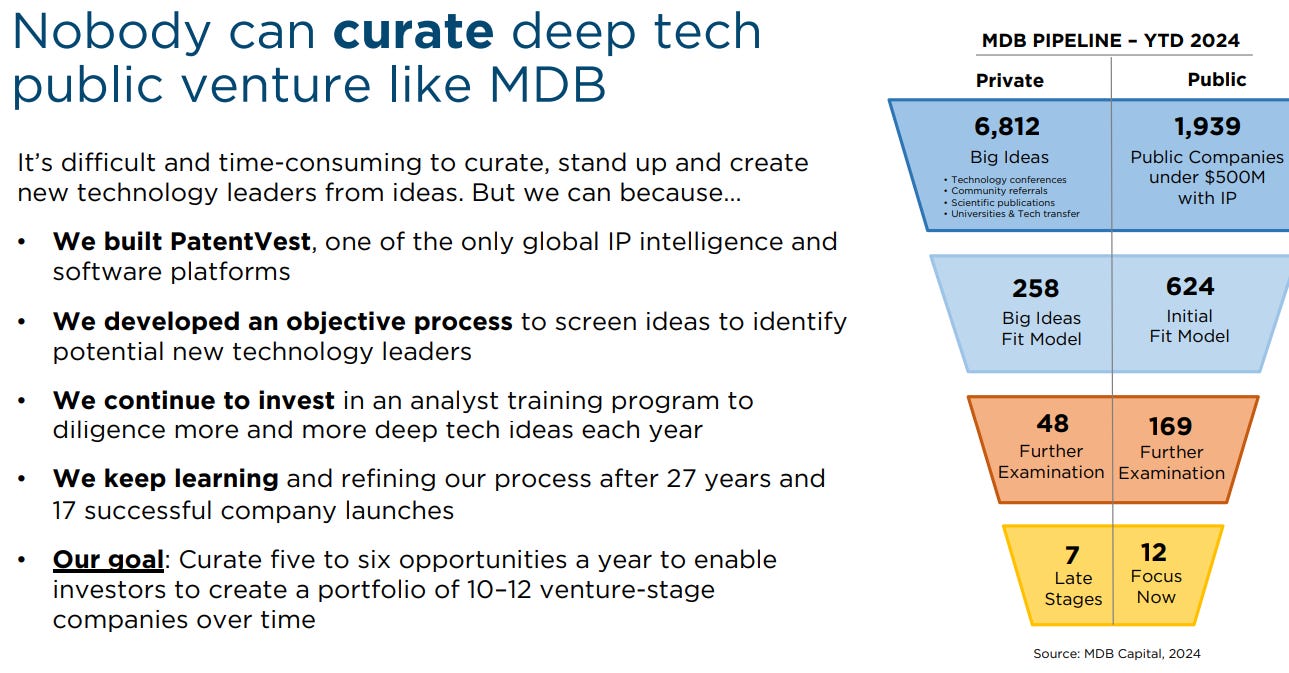

MDB Capital is an odd company. It’s a publicly traded investment bank and a group of high-net-worth investors who are part of the MDB community.

MDB Capital conducts rigorous due diligence and takes companies public. They also sometimes invest in already publicly traded companies like Heartbeam that they did not take public. I have been researching MDB Capital, and I’m quite impressed with them.

Source: https://www.mdb.com/why-mdb/curation-process/

Source: https://storage.googleapis.com/vendorgroup-assets/site/c9b0f1f2-bee4-4f4e-adc1-886ae6e270de/MDB%203Q%202024%20Shareholder%20Call%20-THE%20FINAL-%2021NOV24.pdf/2024/11/21/673fbe4b6fb6d550d5d7bcd1

Source: https://www.mdb.com/why-mdb/investment-criteria/

This is their investment philosophy. They analyze massive amounts of companies and how many fit their criteria, which you can see explained in the above picture. From there, only a few make it into investments.

Here is a video where they explain their process in more depth.

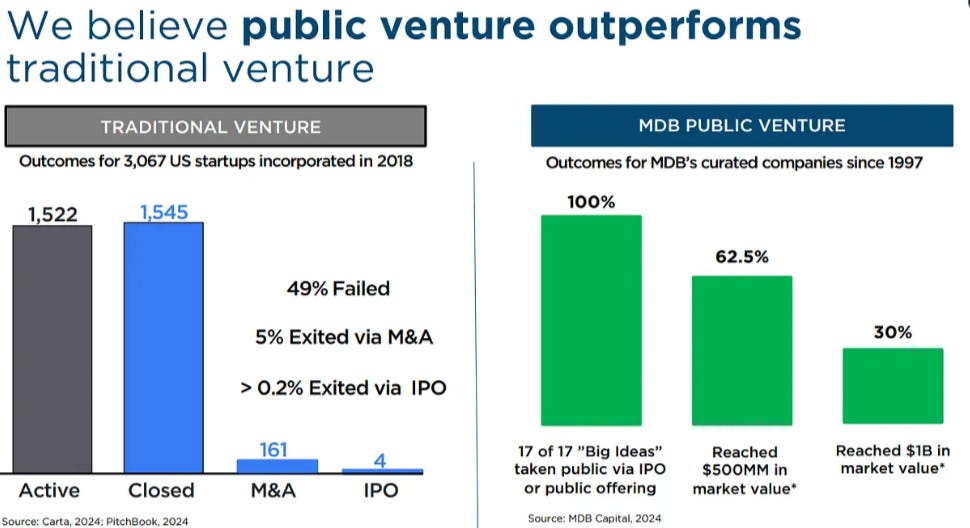

Any institutional investor will tell you how they do thorough research into their investments. So why am I going on about MDB? MDB has an excellent track record with companies like Heartbeam and is currently investing in only three public companies; Heartbeam is one of them.

Source: https://storage.googleapis.com/vendorgroup-assets/site/c9b0f1f2-bee4-4f4e-adc1-886ae6e270de/MDB%203Q%202024%20Shareholder%20Call%20-THE%20FINAL-%2021NOV24.pdf/2024/11/21/673fbe4b6fb6d550d5d7bcd1

If you look at that track record and then at the MDB market cap of only 66m, it will raise questions. This is because when MDB sells investments, it distributes the profits to its shareholders, so MDB does not have a treasure chest of stocks of companies in its portfolio that it has invested in over the decades. This keeps the company relatively small.

Some of these companies they have taken public at much lower prices include Pulse Biosciences(multi-bagger from IPO, still public), Prevention Bio(acquired for 2.9B), and Medivation(acquired for 14B, more than 200x return from IPO price to share price peak).

Source: https://storage.googleapis.com/vendorgroup-assets/site/c9b0f1f2-bee4-4f4e-adc1-886ae6e270de/MDB%203Q%202024%20Shareholder%20Call%20-THE%20FINAL-%2021NOV24.pdf/2024/11/21/673fbe4b6fb6d550d5d7bcd1

They have 2,145m USD worth of shares and 1.6m warrants. They have been the underwriter for a 25m raise in 2023 and an 11.5m raise in early 2025 for Heartbeam. The MDB’s direct position doesn’t tell the whole story, because the MDB community of high-net worth sophisticated investors own a lot of this stock and participate in these raises heavily. We don’t know exactly how much of the last raise was from the community because they are private individuals, but I think we can assume it was a lot because MDB shareholders have an allocation preference, and the raise was oversubscribed. They had an over-allotment option, which allowed the company to raise an additional 1.5$ on top of the original offering amount of 10 million.

Source: Heartbeam corporate presentation

MDB Capital is clearly heavily involved with this company. It’s helping the company raise money. MDB’s involvement lends legitimacy to Heartbeam, thanks to its strong track record. MDB also helps Heartbeam with its IP strategy with their wholly owned subsidiary PatentVest.

Source: https://www.mdb.com/about/subsidiaries/

Management

I won't start listing all the management's credentials. They do have some impressive people. Here are some links:

Heartbeam call with MDB↓

<iframe title="vimeo-player" src="

" width="640" height="360" frameborder="0" allowfullscreen></iframe>

Summary

Now that you are here. The next thing you should do this article again. Understand the investment thesis.

You’re back from your second read. Now that you and I both understand Heartbeam investment thesis we can list out our main risks and positives.

Positives:

-TAM is massive, and the market cap is small

-There won’t be additional capital raises for about a year

-MDB Capital is invested and is supporting the company in other ways

-The device works

-The device will have a strong demand

-The device is a game changer

Risks:

-Commercialisation in practice presents challenges

-The FDA approval for the software has not been granted yet

-Potential weak study results

I think the positives outweigh the risks here, which is why I’m willing to bet on Heartbeam. Still, it’s not a large position. There are risks and not much of a margin of safety to keep the stock price from crashing if some of the risks materialize. And I’m sure there are risks I’m not even thinking about. In the bear case, the stock price would go lower, and then they would need to dilute at the lower price and so forth. This is the dilution death spiral, which I covered more in my Smith Micro article.

The potential reward is massive. The story has already been de-risked in many ways. If I saw this stock in this situation, trading at a $ 500 million market cap, I would not be surprised at all. But the delays sucked the initial hype out of the stock, and now we have a chance to get it at a very low market cap while knowing they have a game-changer product. That is the key to this thesis. At this point, I can say with let’s say 99% confidence that the product is at least the best at-home and on-the-move ECG device. We need more results with the final commercial device to make that 100%, but combining everything that we know so far, it’s pretty clear that it’s at least the best portable heart monitoring device. That is already a massive market opportunity even before considering the potential to take over the hospitals.

Knowing with 99% certainty that the product already is the best in a niche with a multi-billion-dollar total addressable market (TAM), backed by MDB and a $ 60 million market cap, is what makes the risk-reward so attractive for Heartbeam.

Great write up mate! Heartbeam is definitely an under the radar opportunity with little coverage. Once they receive FDA approvals, the company could really fly