Smith Micro Software: Death Spiral

Is it over?(paywall removed)

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program which means I have a financial relationship with Seeking Alpha.

Mongolian short AD: THE LINK Long AD: LINK

Get a 7-day free trial and 30$ discount on your first year of Seeking Alpha Premium with my Affiliate link: AFFILIATE LINK

It’s tax loss selling season. A time of year to look at horribly performing stocks YTD that people are selling for tax purposes. This year the effect of the tax loss selling is even more drastic than usual especially in the US because of the overall strong market performance people will be selling their losing positions to reduce their capital gains taxes for the next year. I’m on the lookout for beaten-down stocks that have the potential to turn-around like Smith.

Smith Micro Software is a software company founded and still led by William Smith. It’s also a micro-cap. They named the company correctly in 1982, knowing these three things wouldn’t change.

Source: https://ir.smithmicro.com/presentation/SMSI-Investor-Overview-November-2024.pdf

They have 3 products and they white-label these products to other companies. Meaning their customers will rebrand Smith’s products, market them and have revenue sharing agreements with Smith.

Safepath=Family safety app Smith white-labels to wireless carriers for them to rebrand and sell. Their main revenue generator and centerpiece of the investment thesis. This product is the ultimate helicopter parent. It tracks everywhere your child goes, what he/she does online, what websites they have access to, controls screen time and they can’t delete it. It’s a great app. Allthough I don’t have any personal experience using it or other similar apps.

Viewspot=Retail management solution

Commsuite=Advanced Messaging solution

Smith has been around for a long time.

Source: Google

And now we are sitting at close to all-time lows. The exact all-time low was 0,55$ which was hit a couple of months ago and I don’t know why it was up 15,9% yesterday. This stock can be erratic.

The company has a market cap of 15,42 million USD and no debt.

Their TTM revenue is 24,2m USD and they are burning cash, but are saying that will change in 2025. Their gross margin is 70-90%.

February 21st, 2020 Smith acquired Circle Media Labs for 13.5m USD

April 19th, 2021 Smith Acquires the family safety business from Avast for 66m USD

This is already starting to remind me of another company. Send me a fax If you know what other company I’m thinking about.

The integration of Safepath with Circle and Avast plus the R&D spending over the years means Safepath has easily gotten +100m USD of investment.

February 27th, 2023 Verizon terminates its contract with Smith to build its own family safety app.

April 3rd, 2024 Smith announces reverse split to stay listed on Nasdaq.

October 3rd, 2024 the company raised 6,9m$ which included 3m$ investment from the CEO and Founder William Smith.

November 19th, 2024 European tier one carrier Orange launches Safepath in Spain.

There was some starting information. Now let’s move on to my history with this stock.

Mongolian history

Source: Seeking Alpha Premium+My edits

This is my history with the stock. In Autumn 2024 the remaining small position had plummeted and an insignificant sum was left. I was thinking about whether to take the tax loss or buy the dip. I did not have a strong view on Smith, because I had not done proper due diligence on the stock. I had surface-level knowledge and was focusing more on other stocks. So end of this summer and autumn was the first time I started doing proper due diligence on this stock to make up my mind on what to do with this calamity which was long overdue because I had a position since 2022. Shouldn’t wait for 2 years before starting due diligence.

Source: Almostmongolian, Substack notes

Sometimes I write Substack notes. Follow me on the Substack App for these.

This August I made the decision and 5x the position then recently added some more now having 6x the position and got my cost-basis down to 1,96$. It’s still my second smallest position(slightly bigger than Eco Atlantic). Shows how small the position had gotten that I could 6x it and it would still be the smallest position. I wouldn’t make this a big position even now. Maybe a mid position, but It’s still one of my riskier picks. The current price is 0,88 so now I need 123% to break-even. Which I think has a high chance of happening.

What went wrong in 2022-2024?

The original thesis in late 2022 when I first got involved was this. Smith has Safepath and they got the top 3 wireless carriers in the US as customers Verizon, T-Mobile, and AT&T. Massive companies. Massive subscriber base to market Safepath to. If these companies start pushing the app and ramping up marketing Smith will grow massively and there were all sorts of arguments about why they would do this. “Marketing Safepath is a win-win for both Smith and the Carriers.” Safepath grew very fast with Sprint(previously 4th biggest US mobile carrier) which was acquired by T-Mobile. This is Safepath growing with Sprint.

Source: Picture from this article. Another write-up about Smith from june 2023

Imagine if you could do this kind of ramp with one of the 3 carriers that all have way more customers than Sprint. They just need one carrier to do what Sprint did to succeed. The product has also been vastly improved since the Sprint ramp with new features, new offerings, and integration with the Avast Family safety product and the Circle family safety product.

Source: https://www.statista.com/statistics/199359/market-share-of-wireless-carriers-in-the-us-by-subscriptions/

What ended up happening:

Verizon terminated its contract with Smith in order to build its own family safety app.

T-Mobile merged with Sprint and while this provided Smith with a bigger potential opportunity because of T-Mobile’s much larger customer base the merger turned out to be a disaster for Smith because while T-Mobile kept using Safepath they were not as motivated to market their Family Safety App as Sprint was.

AT&T launched its upgraded version of Safepath in August 2023 and there was going to be a marketing push with that. The “we only need one” thesis was still in play and shareholders had faith in it. “If AT&T ramps like Sprint the Verizon loss will feel like a mosquito bite”

Also, the other smaller parts of Smith’s business their products Commsuite and Viewspot experienced declines.

This is what happened with the top 3 carriers.

There is going to be some positive stuff later.

Revenues went down:

2022=48.5m

2023=40,9m

TTM(trailing 12 months)=24,2m

And the company kept burning cash despite cutting costs. Cash from operations is the same as FCF for Smith because they have no CAPEX and an immaterial amount of other investing activities in the cash flow statement.

Source: Seeking Alpha Premium

In Q4 2023 Verizon terminated their contract, but Smith had a launch with AT&T in Q3 2023 which was expected to coincide with a heavy marketing push from AT&T and this growth would offset this revenue loss somewhat as well as their launch with a European tier one carrier in the summer of 2025. So things did not seem too bad.

Then AT&T did not really push Safepath that much and the Launch of the European tier one carrier was delayed to November of 2024. It has now finally launched.

Because of all this underperformance and delays the stock has been in something I call THE DEATH SPIRAL.

What is the death spiral?

A death spiral can occur when growth stocks do not deliver. These stocks have high valuations when the market believes in the story. They usually burn cash (investing in growth) but can raise cash from the market using their high valuation, because the market believes in the growth story.

But when the company does not meet market expectations. The stock price falls. They need to raise money at a lower valuation meaning more dilution. Doesn’t meet expectations again. Stock falls. Raises money and again it dilutes more than last time because of lower valuation. And so forth

The stock has a 100m market cap. They raise 5m$ and dilute 5%. If the market cap falls to 50m$ now 5m$ raise is a 10% dilution. If the market cap drops to 10m$ the 5m$ raise is a 50% dilution. This is not accounting for warrants that would be usually included with the raise.

As this keeps happening market will start expecting it and the stock falls in anticipation of the next raise which will dilute more because of the lower valuation. This is what happened to Smith. Their last raise diluted about 50% instantly and around 100% with Warrants.

If a cash-flowing stock falls in price the stock is just cheaper and pays a higher dividend yield or the company can buy back stock cheaper. With a growth stock that needs to tap the market the stock price fall by itself can be a negative fundamental event because raising money becomes so much more dilutive to existing shareholders.

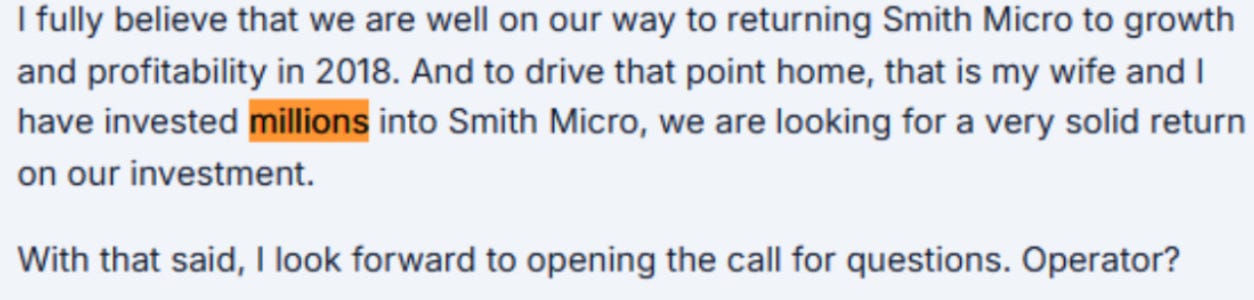

The death spiral can end in 2 ways. The valuation starts rising so raising money is gets less dilutive or the company gets profitable and doesn’t need to raise money anymore. After this happens or if you project this happening it’s time to buy and reduce cost-basis and you can’t be thinking about the prices in previous years where you bought in originally. The dilution has been so heavy after a death spiral that returning to those prices is unlikely. It has to be treated as a new investment. Seems like the CEO of Smith Smith understands this with his recent 3 million dollar investment at 1,165$.

It’s noteworthy that the last time Bill Smith made a large investment in the company was before the big ramp-up with Sprint which led to a big stock price rise. Now he makes a big investment and they have just launched with Orange.

Source: Q3 2027 Smith earnings call

Smith stock multibagged after this.

Getting back to the dilution after a death spiral. In late 2022 Smith's stock price was 18$ and the market cap was 131 million.

Smith’s current stock price would have to rise 21x to get to that same price and because of the dilution, the market cap at the current diluted sharecount would be 460m USD. So this is very unlikely. Maybe if everything lines up perfectly. But returning to the 131m market cap is very possible and even likely if they can get to profitability and consistent growth again. Considering last time they were at that market cap, they were not even growing or profitable, but market believed they would be in the future.

Buying when you think the death spiral is over is similar to having your stock go bankrupt and you buy the post-bankruptcy business. If you want to make money you need to buy the dip and lower your cost-basis dramatically and understand the stock will likely not get to your original pre-spiral purchase price.

This death spiral reminds me of another stock. Send me a carrier pigeon if you know what stock I’m thinking about.

Now that I’m making up terms let’s talk about a life spiral which is the opposite of a death spiral Aduro is a good example of a life spiral which is another stock that needs to raise money and I have been also holding it since 2022. When a stock like this meets market expectations or exceeds them the company can keep raising money and raising the same amount of money becomes less dilutive over time because the valuation is going up.

Source: Google+My edits

Red spots mark when Aduro raises money,

These spirals are very important. Always predict the spirals. Also, predict everything else. Correctly. Very important for investing success.

The Smith investment case at this price is that they are exiting the death spiral.

They have no debt. They have 6,9m USD from their last raise if they can stop burning cash before the money from the last raise runs out they are out of the death spiral. I would say that alone would provide 2-3x return from here.

The last raise also included a warrant for every share. These warrants will be exercisable from the 3rd of April 2025 and at the price of 1,04$. So if the stock is above that price by that time this will also provide the company with more cash giving them more time to become profitable. This would also be quite dilutive, but considering the price is 0,88$ there is already a considerable 17% return before that dilution.

Then if they can return to consistent growth and start having strong earnings, this would return the stock to a more typical Nasdaq software growth valuation. Potentially 70-140m USD. 3-6 times revenue With the current market cap being 15,42m USD.

Reaching profitability

Smith needs a mid-7m$ revenue range per quarter to breakeven according to the management

Scott Searle

Maybe to dig in a little bit further, I think at the midpoint of guidance for December, you're looking at about a $500,000 sequential uplift. I wonder if you give us an idea of where that comes from. It sounds like the European carrier is part of that, but who else is providing a positive trajectory on that front and contributing to that increase?

Bill Smith

Yes, I don't really want to get into the name by name on the thing, but it's coming from a collection of activities with current customers, as well as new customers. And so we feel very comfortable with it. And I think the other part to keep in mind is you add that growth to the fact that we're going to continue to reduce the overall expenses will allow us to narrow the losses that we will see in Q4 and lead us to a trend that will take us to profitability in ‘25.

Scott Searle

And just to clarify that in terms of the new break even, Jim, it sounds like we're in the ballpark around $7 million or so is kind of the break-even level?

Jim Kempton

Hey Scott, how are you? As far as the break-even, it's probably you know in the mid-7 range when you take into effect cost of sales.

Quotes from the Q3 earnings call

In the fourth quarter of 2024, we expect consolidated revenues to be in the range of approximately $5 million to $5.2 million. This anticipated growth in revenues as compared to the third quarter is driven in part by a projected increase in Family Safety revenues.

From 5m to 5,2m in Q4 to mid-sevens might seem like a big jump, but this company has a very jumpy revenue. This would not require much to happen.

Since Q3 2023 every quarter has been a Q-O-Q decline in revenue. Q4 2024 would break this trend if they have 5m to 5.2m of revenue as they say. I do trust Smith management’s short-term revenue and cost predictions from my experience they have been accurate in the past.

And if they keep up Q-O-Q growth we will also get Y-O-Y growth next year. This would improve how the stock screens and change the sentiment around the company. This coupled with their prediction of being profitable next year would make it a profitable growth story which would completely change the valuation, but I can’t just take their word for it. Let’s see how they could get to that point and how likely is it.

“In other words, we anticipate that our total quarterly non-GAAP operating expenses and cost of sales will decrease by $2.4 million to $2.8 million, when comparing first quarter 2024 costs to the fourth quarter of 2024, based on the cost reduction activities executed this year.”

excluded the following items from GAAP earnings calculations: stock compensation, intangibles amortization, depreciation, fair value adjustments, amortization of debt issuance costs and discount, goodwill impairment, personnel severance and reorganization activities, and adjustment for non-recurring items.

The non-GAAP costs are all cash costs. In Q1 their cost of sales+GAAP operating expenses were 13,3m if we take out the midpoint of that prediction 2.6m

Then we have 10,7m then we take out non-cash costs like amortization and stock-based comp(these are about 50/50) which is roughly 3m then we get 7.7m that is basically a cash flow positive point. Stock-based comp is of course a real cost, but at this point, it’s most important to get the cash flow breakeven to stop the death spiral.

Smith has also delivered on cost reduction so I’m inclined to believe they will deliver on that front going forward. The revenue has been the problem.

At roughly 7,7m cast costs(including cost of sales) and 5,1m revenue(midpoint of the prediction) they would burn 2,6m of cash. They received the 6,9m on October 3rd. Assuming they would not improve their revenue or reduce their costs any further than Q4 and that the stock doesn’t go above 1,04$ for the warrants to provide them more cash this raise would sustain them to around the start of summer 2025 with the warrants possibly to the end of 2025.

This would be the bear case. Even a conservative prediction would include some revenue growth for the next quarters, because of certain activities I will talk about soon, but I think a conservative estimate would be that Smith would have reduced burn and this cash would last them to the latter part of 2025.

The moderate bull case is that they will stop burning cash before the cash from the last raise runs out. To do that they will have to grow revenue.

Revenue drivers

I’m pretty confident Smith will deliver on costs, but to get to profitability Smith also needs higher revenues so let’s see what negative revenue drivers have been causing lower revenues and are those factors going to keep causing further declines and what positive revenue drives there are and what are the projected and potential positive revenue drivers.

After Verizon revenue ended their revenue dropped to 5,8m in Q1 2024. This was the biggest cause of falling revenue, but revenue still kept going down in 2024 being lowest in Q3 at 4,6m. What were the drivers of this?

ViewSpot

Viewspot their retail product. Experienced declines.

“ViewSpot revenue was approximately $100,000 for the third quarter of 2024, which declined by approximately $1 million, compared to the third quarter of the prior year. The decline in ViewSpot revenues compared to the third quarter of 2023 was primarily due to the previously announced terminations of two of our ViewSpot contracts. ViewSpot revenues decreased by approximately $300,000, compared to the second quarter of 2024.” Q3 conf call

Viewspot was never that important for the bull thesis, but a decline of 1m per quarter is very material for the company. Like I said I did not do proper DD on this stock originally and this was one of the problems I was ignoring.

Now Viewspot is almost nothing 2% of the revenue in Q3 so this won’t be a material negative on revenue growth from now on. The base is so low that more likely it will grow from here, but I’m not projecting that.

Someone asks if Viewspot is going to zero in the Q2 conf call and the CEO says this.

“Yeah let me add that we also have new opportunities for ViewSpot that we are exploring and they're with meaningful names, so let's just you know we'll monitor the process we'll report it safely every quarter but I think it's a nice product. It's had sort of a checkered role in the market in the last year or so, but that doesn't mean that we can't turn it around. So we'll see.”

I’m not expecting much from Viewspot, but it won’t be causing additional material revenue declines and could possibly make a comeback if they get some contracts.

Currently Viewspot has only one client left.

Legacy Sprint Subscribers

What else has been causing revenue decline this year? Another issue I was not aware of because of my original lack of DD. This is the:

“The 52% year-to-date decline, compared to the prior year is primarily due to the conclusion of the Verizon Family Safety Contract in the fourth quarter of 2023, coupled with a decline in Sprint Safe and Found Family Safety revenue related to the continued attrition of legacy Sprint subscribers driven by T-Mobile's acquisition of Sprint.”

I talked about the T-Mobile and Sprint merger that hasn’t worked for Smith. There has been a steady subscriber decline from old Sprint subscribers, because after the merger these subscribers are being migrated to T-Mobile which ends their Safe & Found Subscription. Safe and Found is the Sprint Safepath App which is getting phased out.

And like I said earlier T-Mobile has not been pushing their version of Safepath “FamilyMode” so the growth from T-Mobile has not been offsetting the decline of Legacy Sprint Subscribers. This has been a gradual decline, but according to Smith this is getting less impactful. There is only so many users left on the old app.

“the decline of sprint users is getting down to a fairly small number overall.”

I don’t know what is the number at the moment. So I’m not quite sure how big of an impact this will still be, but this attrition has been happening for a while I doubt there are still many Safe & Found users left and the management is saying the decline is getting to a “fairly small number”

These 2 are Smith’s remaining sources for revenue decline. Potential further declines from Viewspot from this point are immaterial. And the decline from legacy Sprint subscribers are getting to a “fairly small number”.

Based on current information there is not much left in terms of sources of revenue declines from here.

Now I can move on to the fun part. Sources for revenue growth.

CommSuite

Commsuite their visual voicemail platform was experiencing revenue declines but turned the corner on Q3.

“During the third quarter of 2024, CommSuite revenue was approximately $600,000, which decreased by approximately $100,000 compared to the third quarter of 2023. Revenue from CommSuite increased by approximately $100,000, compared to the second quarter of 2024, as we have been experiencing subscriber growth on the boost CommSuite premium visual voicemail platform and expect that trend to continue in the fourth quarter.”

This was 13% of the revenue in Q3. It’s not huge that it has returned to growth, but it’s a net positive. Everything matters as they need to get the revenue to mid-7s to stop burning money.

“Boost has continued to grow as value-added service premium visual voicemail, which is powered by our CommSuite platform during Q3. The expansion of subscribers Boost experienced on the premium visual voicemail platform during the third quarter translated into the meaningful increase in our CommSuite revenues, representing over 20% growth versus the second quarter.”

If they could continue 20% Q-O-Q growth CommSuite revenue would be about 1.5m in Q4 2025. Not projecting that, but it would be impactfull.

This product did more than 18m USD in 2020 so if it’s still competitive enough to grow with Boost maybe it’s a sleeper.

Boost is also one of the new Clients of Safepath

Boost Family Guard, Safepath

Source: https://seekingalpha.com/pr/19673212-smith-micro-announces-new-agreement-mobile-operator-in-us-for-deployment-of-safepath-platform

Boost Family Guard Introduction

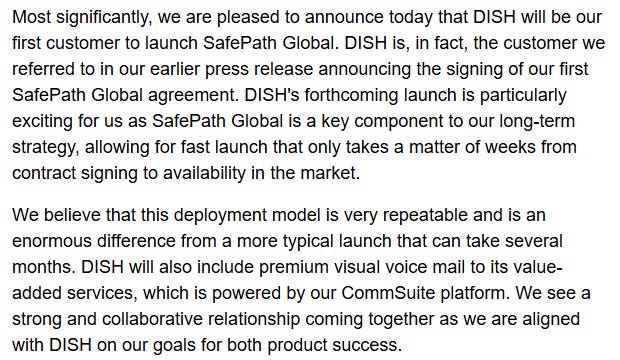

This was client was confirmed to be Boost Mobile which is owned by Dish and this is done with a relatively new module Safepath Global which allows for a faster launch. Smith was able to launch this in 6 weeks which is a major improvement from other launches.

Source: https://seekingalpha.com/article/4691148-smith-micro-software-inc-smsi-q1-2024-earnings-call-transcript

This combined with Boost signing up with Commsuite aswell is setting up for a a strong long-term relationship which is just starting to show up in the financials.

The CEO said in Q2 basically that he expect similar results with Dish than with Sprint.

“Well, you know, I think you've brought up Sprint and you've brought up the success we had at Sprint. And we've always thought it would be very repeatable. Based on the commentary I've already made, I think you can see that DISH is doing everything that Sprint did plus more. So I think where you really want to watch is to watch the growth for DISH and the Boost Family Guard. I believe that's going to be a rather exciting event. I haven't said much.”

Dish is not as big as Sprint had over 50m subs before the Merger with T-Mobile and Boost Mobile owned by Dish has 7m now. Making it the 4th largest wireless carrier in the US.

The difference between 3rd and fourth is huge. 3rd biggest is AT&T at 116m subs. Still if Boost ramps up marketing it will definitely be a material customer.

“Bill Smith

Thanks, Jim. As I started the call by talking about some of our new customer opportunities, let me pivot to providing you with some updates on our ongoing carrier partners. Boost is ramping up the marketing of its SafePath-based Boost Family Guard in its retail footprint. They provided marketing collateral to their retail stores in September and are providing splits for their retail employees, which we believe is an effective tool to drive awareness of the new product offering.

Outside of the retail stores, Boost continues to leverage other avenues to promote Boost Family Guard throughout its subscriber base, using SMS, email, and website promotions to promote Boost Family Guard and attract more family plan subscribers to the Boost Mobile Network.” Q3 conference call

Boost seems motivated to push Safepath.

T-Mobile, FamilyMode

“At T-Mobile, we continue to explore our expanded SafePath platform for opportunities to broaden our relationship. Our sales and marketing teams are working together to further our progress by widening our reach within the organization. In the meantime, T-Mobile continues to be a key customer for us.” Q3 earnings call

This is all they had to say about T-Mobile in the Q3 earnings call. The management doesn’t seem too excited about it and so far T-Mobile does not seem to interested in pushing Family Safety.

In the Q2 call someone asked about T-Mobile and Smith pivots to talking about how exited he is about the European carrier and Dish.

So we’ll see if someday they can get through to T-Mobile, because it would be a huge opportunity, but at the moment T-Mobile is not a something to be too exited about before we see some actual change. For example similar marketing campaign than Boost is doing.

AT&T, Secure Family

Secure Family introduction page

Source: https://www.smithmicro.com/press-releases/2023/08/30/us-tier-1-carrier-launches-upgraded-family-security-application-powered-by-smith-micro-safepath-platform/

This is when AT&T launched Safepath and it was paired with a lot of optimism. The stock had a run-up up and people were sending pictures of AT&T stores with Secure Family showing on the phone screens to this WhatsApp group of investors which was very active at the time. The bull case was that this was going to compensate for the loss of Verizon. I did doubt how fast it could happen hence I reduced my position on this run-up, but I was still optimistic so I kept a small position.

But this did not happen. It did grow, but by far not as much to compensate for the loss of Verizon. Still, I’m more optimistic about AT&T than T-Mobile as they have started some marketing activities recently.

“Let's talk about AT&T and the new promotional activity for AT&T Secure Family that is currently happening. In November, we began a new social media influencer campaign for AT&T Secure Family with a group of selected influencers, who are purposely driving awareness of the product's features. More than just focusing on family and relevant issues faced by parents in today's world, these influencers are also parents, who have the same concerns as all parents, which makes each of them an outstanding spokesperson on social media platforms to promote the benefits of AT&T Secure Family. This campaign is just getting started and we expect it to continue over the coming months and into 2025.

In addition, AT&T Secure Family has been recently featured within connected television advertising. This advertising content has shown on platforms such as Paramount, Pluto, Warner Brothers Discovery, and Disney, just to name a few. This is another fresh approach to raising awareness of the benefits of this app. These activities are in addition to the ongoing digital advertising. With all these marketing efforts, we remain very optimistic about the opportunity with AT&T and are looking forward to seeing growth in the coming months resulting from these efforts.” Q3 earnings call

It seems like AT&T is still motivated to push Safepath. I’m cautiously optimistic about this.

Orange, Safepath, European Tier one carrier

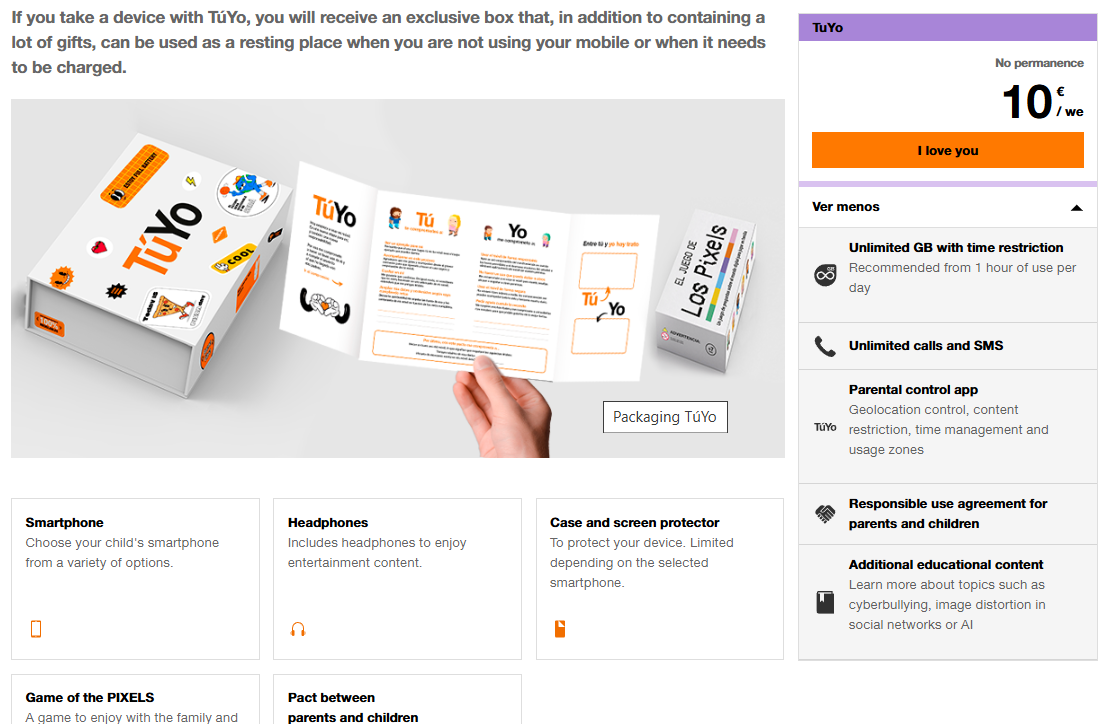

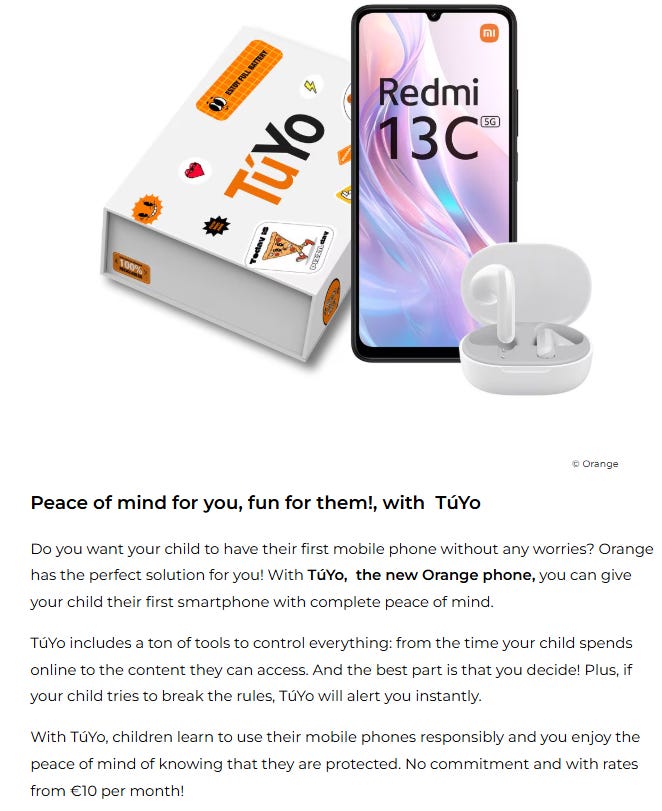

This is the most recent big client for Safepath and the delay in launching this has also been playing a part in the weak revenue for 2024. It was originally supposed to launch in summer of this year, but it was launched in November.

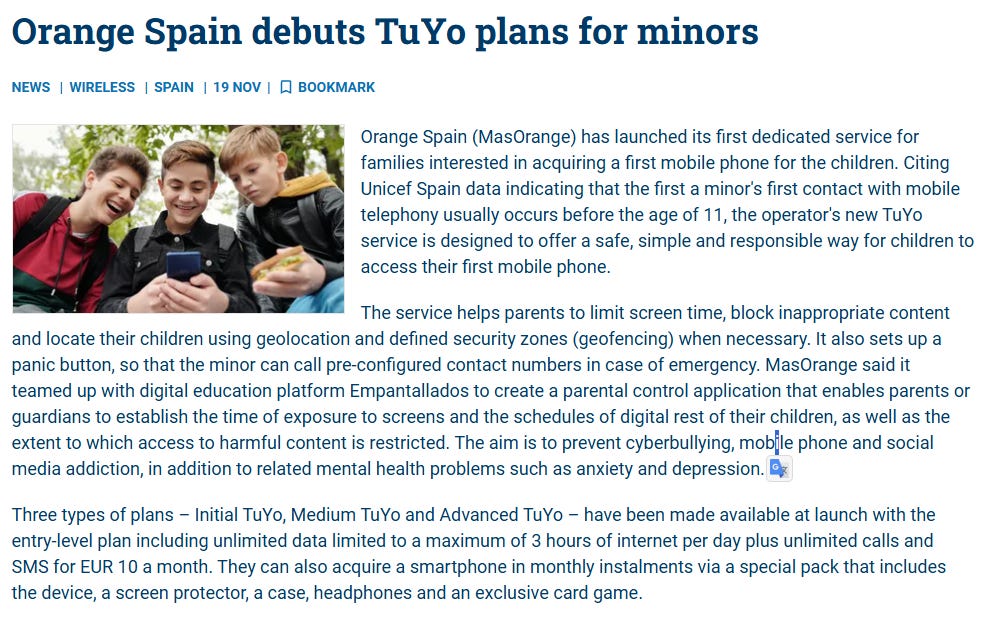

Source: https://www.smithmicro.com/press-releases/2024/11/19/safepath-powers-orange-spain-tuyo-childrens-mobile-plan/

I think Orange is the most promising client Safepath has at the moment. One reason is that it’s a major carrier. It has almost 300 million customers worldwide, but for now, they have launched Safepath in Spain.

Orange has around 37 million customers in Spain.

They operate in 18 countries.

And they will also launch Safepath in other countries. So far it is unknown whether they will launch it in all 18 countries. But I would expect them to launch it in the European countries at least.

“Yes, look, I, you know, What I can say is this, this launch will be launched in a first country. It is a country where they have meaningful size and we are already in conversations about who the next countries will be. So this is just the beginning. So when we launch in a couple of months, yes that's just the first country and there's more to follow and they can be -- and that can be done in rapid fashion. Really the only difference is just changing the language and so that the users can read the props.” Q2 earnings call

This should provide some nice positive news flow in 2025 as Orange launches in other countries if it really can be done in a rapid fashion.

I’m also more optimistic about Orange because it’s a completely organic client. Many of the other big clients became Safepath clients because Smith acquired the family safety app they were using and converted it to Safepath, there was a merger, and cross-sell and Smith has been doing business with these carriers in the US for years. Decades even. The point is the way they ended up with Safepath was less organic than how Orange ended up with Safepath.

Orange is a huge global carrier from Europe that picked Safepath over all the other competitors seemingly just because they think Safepath is the best product for them. They didn’t have a history with Smith and it’s a small foreign company. So their picking Smith tells me that they picked Safepath despite of Smith.

This also improves my view about Safepath as after Verizon ended their contract and T-Mobile seemed very unmotivated with promoting Safepath you could have gotten an impression that the product might not be as competitive as I thought, but this year with Orange, CCA, and Boost it’s telling me that the product is competitive it just had a weak period. This is kind of how I have to judge Safepath because I haven’t used all of these different family safety apps and compared them to see what’s the best. The reviews for Safepath are good, but we know that reviews are a lot of times flawed and not even real. I think that if significant players choose Safepath, it is a better barometer.

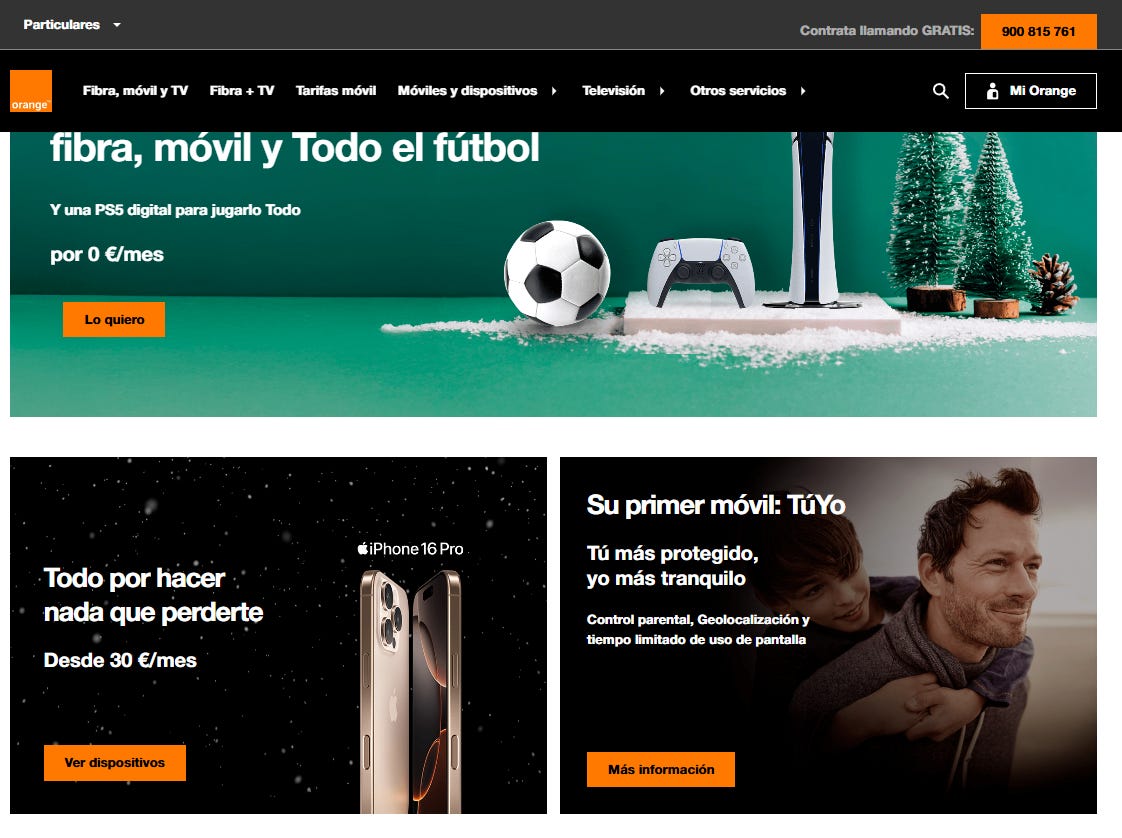

Also Orange is the only big Safepath client that has the product on the homepage.

Source: https://www.orange.es/

And it’s also their pinned Tweet

Source: https://x.com/orange_es

Here is some more info about the product.

Source: https://www.telecompaper.com/news/orange-spain-debuts-tuyo-plans-for-minors--1519523

I’m optimistic about this launch with Orange and what the next launch country will be. Also, They are saying they are in talks with other big European carriers.

“In Europe, we have ongoing discussions with several carriers in various countries and truly believe that our European Tier 1 carrier launch will ignite further conversations. We are also in discussions here in the U.S. with carriers to launch SafePath as a strategy to attract new family subscribers. Overall, we believe that these new opportunities bring significant upside and that the potential for AT&T Secure Family with several new marketing initiatives positions us for growth over the coming quarters.” Q3 earnings call

The offering with the Orange is also different because it’s integrated with the phone and the phone plan the customer is in. This means a much lower churn because for Smith to stop receiving revenue the client would have to change their whole phone plan.

Source: https://www.orange.es/tarifas/movil/tuyo

This should be recurring revenue with low churn and committed customers. If they can just switch the language and roll it out in other countries this could be big.

I also like this direction because it moves Safepath away from being a competitor to different free family safety apps like Life360 and moves it to being more of a premium product that can be sold as an integral part of the device.

Source: https://www.hola.com/padres/20241213734320/10-juguetes-tecnologicos-ninos-y-adolescentes/?viewas=amp

The stock has been in such a bad place there is very little excitement for this, but it’s hard not to be optimistic about a development like this.

CCA Marketing Agreement

Source: https://www.smithmicro.com/press-releases/2024/08/06/smith-micro-announces-entry-into-a-marketing-engagement-agreement-with-competitive-carriers-association-for-safepath-global/

Source: https://www.ccamobile.org/about-cca

It’s hard to tell the signifigance of this marketing agreement yet. Most of that “subscribers served” is T-Mobile being a member of CCA. Most of the members are smaller carriers, but all of them together still provide a large potential opportunity.

“we're pretty excited about the CCA opportunity. It provides us access to a large number, about 40, 50 different carriers around the US. And I'm not including T-Mobile, who is also a member of CCA. So that's their excluded from this opportunity, because we already do business with them. So, collectively, we are talking about tens of millions of subs and individually, there are a number of carriers that are smaller that would be very difficult to market to without this marketing arrangement.

And we're very, very excited, as is CCA, to be able to leverage their footprint to find some more meaningful growth. Again, we will focus on SafePath Global with all of these accounts. We are looking for very rapid deployment” Q2 earnings call.”

The management seems quite optimistic about it and saying they have already got some contracts and are expecting to sign more more CCA carriers in the coming weeks and months. Below is some quotes from the Q3 earnings call about CCA.

“On our last call, we discussed our marketing and engagement agreement with the Competitive Carrier Association, CCA. This is the completion of that agreement. Smith Micro and CCA have partnered to market our SafePath Global Family Safety Solution to CCA's carrier members under a single brand name of SafeTools. This partnership enables CCA carrier members of any size to offer this valuable solution to their subscribers under the rapid go-to-market model that SafePath Global supports. We currently have contracts in process with multiple CCA members under this arrangement, and I expect it will sign additional CCA member carriers in the coming weeks and months. This quick to market approach truly expands our brand and market opportunity, delivering our SafePath platform to more families across the U.S.”

“We're seeing good traction through the CCA with a number of different member carriers now in the process and expect more to follow.”

“As I noted in my opening remarks, the competitive carrier association marketing agreement that we announced during the last earnings call is already yielding positive outcomes. In addition to opportunities with CCA and the SafePath OS contract under way that I touched on earlier, there are several other exciting opportunities in the sales pipeline.”

“Leo Carpio

Okay, and then lastly, in terms of the CCA, what's the average deal size you're seeing there in terms of your contemplating?

Bill Smith

That was on the CCA.

Leo Carpio

CCA, yes.

Bill Smith

Yes, and they vary in size from relatively small carriers up to carriers with a few million subs. So we expect in total as we see a number of these carriers going through the process of executing contracts and launching the Safe Tools product that will see a very nice collective increase for us going forward.”

This has the potential to be material if they can get multiple carriers that are motivated to market Safepath and potentially Smith could use this to also cross sell their other products.

New Safepath offerings

Safepath has various offerings. They are basically the same Safepath product with varying features and methods of bringing to market. They had Safepath Family, Safepath Home, Safepath Drive and Safepath Iot. In the last 12 months they have released Safepath Premium, Safepath OS, Safepath Kids, Safepath Live and Safepath Global.

Source: https://www.smithmicro.com/safepath/premium/

Premium has extra features and is more expensive.

The parents will be notified about dangerous behavior on social media or if their child is being cyberbullied. It has all kinds of AI features. If the kid is in a dangerous area the parents will be notified for example.

This is overall just a good opportunity to get a higher revenue per customer.

Source: https://www.smithmicro.com/safepath/os/

This is maybe the most interesting out of the new offerings. Safepath comes pre-installed and more integrated with the phone. The carriers are also best at selling hardware so Safepath being pre-installed with the hardware seems like a good strategy.

CEO answering a question about the Safepath OS business model.

“First off, it is a subscription model. So it's a fee that we'll collect month-after-month, as long as the device is still active and in use. So it's a gift that keeps on giving. It is a fee that, frankly, can be a little bit higher than what we get for value-added services, because it's actually part of the device of the phone. It is a specialized version of the Android operating system. And we think that probably the most salient point is that if there's one thing that carriers know how to do and do really, really well, it's sell new devices. And to be able to align our business case with that activity, I think, you know, increases our chances for really positive growth” Q3 earnings call

With Smith having some trouble with some of the carriers not actively marketing the app this approach of having Safepath already in the phone and having the carriers do what they do anyway. Sell phones and tablets.

In Q3 earnings call, they also mentioned many times that they have a new Safepath OS contract being signed this quarter.

“First, we expect to sign our first contract for the deployment of our SafePath OS solution with a U.S.-based MVNO in the coming weeks. SafePath OS is yet another innovation within our SafePath platform that enables mobile operators to offer and otherwise standard mobile device as a kid's phone or tablet with built-in limits aimed at a safer and mobile experience that kids cannot bypass. We accelerated our deployment schedule for SafePath OS given the strong interest we are seeing in the market. We expect to see the first deployments of SafePath OS in the first quarter of 2025.

Additionally, we are focusing on building our pipeline for SafePath OS, and we expect it will be a strong contributor to our business going forward. We believe that the recurring fees from this deployment model will meaningfully contribute to our 2025 revenues.”

“So what I will say is that the SafePath OS opportunity we believe will close this quarter. We have stated in the prepared remarks that we're looking for revenue to begin in 2025. It is possible we might be able to book some revenue in the current quarter, but we're really focusing on a first quarter launch.”

“As far as other opportunities, I'm very excited about the SafePath OS opportunity that I mentioned.”

Global

Source: https://www.smithmicro.com/safepath/global/

Safepath Global is also promising as it allows Smith to tap into the small carrier market more easily and launch faster. An example of this was the Boost Family Guard that Smith was able to launch in 6 weeks.

“In addition to the faster launch cycle, The SafePath Global model also allows us to move quickly to deploy updates to the app with new features and functionality and offers a significant upgrade path with other tools that can be added to the platform.” Q2 earnings call

Safepath Global synergizes well with the CCA marketing agreement to market Safepath to multiple small and mid-sized carriers. I already had this quote in the CCA part, but here it is again.

“Smith Micro and CCA have partnered to market our SafePath Global Family Safety Solution to CCA's carrier members under a single brand name of SafeTools. This partnership enables CCA carrier members of any size to offer this valuable solution to their subscribers under the rapid go-to-market model that SafePath Global supports. We currently have contracts in process with multiple CCA members under this arrangement, and I expect it will sign additional CCA member carriers in the coming weeks and months.” Q3 earnings call

I like the ideas behind Safepath Global and OS. One targets a different market with a faster launch and another connects Safepath sales to device sales.

Kids

This is the newest offering. They don’t even have an introduction page for it yet. This is what they said about it in the Q3 earnings call.

“Second, we are introducing the SafePath Kids Plan, which allows us to align with the sale of rate plans. With SafePath Kids Plan, the carrier provides a rate plan that includes software to enforce the rules of the rate plan and sets predetermined time limits and age-appropriate content filters for kids. These plans are shaped by industry-leading online child safety experts and thought leaders that have done scientific research in this field.

Special plans incorporate best practices in digital parenting, offering tailored guidance on appropriate screen time by age with maximum limits for [giving] (ph) social media and video watching. Crucially, parents have the flexibility to adjust these settings, providing them with a sense of control and peace of mind, while giving children safe, age-suitable online access. SafePath Kids Plan is designed to ease parental concern by addressing the harmful effects of excess screen time, which can impact children's physical and mental health.”

“We also talked about the SafePath Kids plan, which aligns with carriers selling rate plans to their base. In either case, we're tying the software sale to the actual either device sale or rate plan sale.”

Live

This also doesn’t have an introduction page. Safepath Live and Safepath Kids are the newest offerings. This is what was said about Live in the Q2 earnings call.

“I would like to briefly introduce you to our plans for a new expansion of the SafePath platform that we are calling SafePath Live. While I don't want to go into detail about the product, I do want to mention that this product will utilize our technological strength for family location controls.

The offering will provide a premium model for our carrier partners that we believe will greatly expand their reach and further enhance their competitive position. The addition of this product to our portfolio builds on a key focus to expand our reach and market opportunities while leveraging strong relationships with our existing carrier partners. We also see SafePath Live as a strong marketing opportunity to drive users to our full featured SafePath family safety offerings.

We are truly excited about this next wave of innovation. We are already in the market discussing SafePath live with our growing list of carrier customers and they like it.”

Seems like Live is a location-focused app likely much cheaper than the full family safety offering.

Summary

“I am very confident that the business case for SafePath is strong. Coupled with a significantly reduced cost structure, I believe that we are on the path back to profitability and positive cash flow. In fact, I'm so confident in our prospects, our business case, and our mission that in addition to the stock in the company I already own, I invested an additional $3 million into the company last month as part of our $6.9 million capital raise.” CEO during Q3 earnings call

This is a company with huge potential compared to it’s current valuation. There has been a massive investment made to the products Smith owns in the past. Likely 10x more than the market cap. They have huge clients that could ramp up Smith’s revenues very fast.

Smith has been stuck in the death spiral and had some unfortunate events. Like how the T-Mobile/Sprint merger turned out. Verizon terminating their contract. Viewspot losing contracts. AT&T not marketing as much as expected. European carrier launch delay. Hard to say which of these were unlucky or caused by management incompetence or both. Clearly Smith is not managed by a superstar team based on how long they have been around without being able to sustainably create shareholder value, but the company is still around and they have an opportunity in their hands. They have a strong product with demand. The CEO is loaded up on the stock while the market is not giving any credit to the future potential.

If Smith can get profitable they won’t have to raise money again and they will leave the death spiral. This alone I think will provide 2-4x return from here.

If they can start growing consistently taking advantage of some of the many opportunities in their hands I see 10x potential or more from the current price.

They have no debt which means the downside risk is that Smith won’t be able to stop burning cash before the 6.9m from the last raise runs out. Which means they would have to raise more money which would be highly dilutive at the current valuation.

With AT&T's new marketing campaigns, Orange Spain launch, multiple new offerings, targeting new markets, Commsuite and Safepath both growing with Boost, Viewspot already immaterial, Cost cuts, reduced amount of legacy Sprint subscriber attrition, and management predicting profitability and growth for 2025.

Because of these dynamics I see Smith as an attractive investment for a small or mid sized position. It’s very asymmetric I see the risk/reward profile similar to Eco Atlantic and these positions are also similar sized. Both companies have 10x potential and valuation so low that the company has more than one opportunities that could multiply the stock price by themselves.

Excellent write up about the history and turnaround potential at Smith Micro. They have a lot more irons in the fire. I really like the model that Orange Spain has adopted. There is huge upside just based upon the rest of the Orange countries following suit.