Zoomd Technologies: Momentum

Continues?(paywall removed)

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program, which means I have a financial relationship with Seeking Alpha. This article is for entertainment purposes.

Mongolian short AD: THE LINK

Get a 7-day free trial and the SUMMER SALE 60$ discount on your first year of Seeking Alpha Premium with my Affiliate link: AFFILIATE LINK

If you sign up for 1 year of SA premium using my link and send me proof, you will get a free one-year premium to AlmostMongolian substack.

Zoomd is a Canadian-listed international adtech business that operates a user acquisition platform. They are also a performance-based marketing company. Simply put, Zoomd delivers paying customers to its clients through whatever means necessary within the bounds of legality and the digital world that confines them. Most adtech businesses are compensated based on clicks or impressions; Zoomd is compensated based on delivering paying customers. Multibillion-dollar brands, such as Kentucky Fried Chicken, are using Zoomd for this purpose.

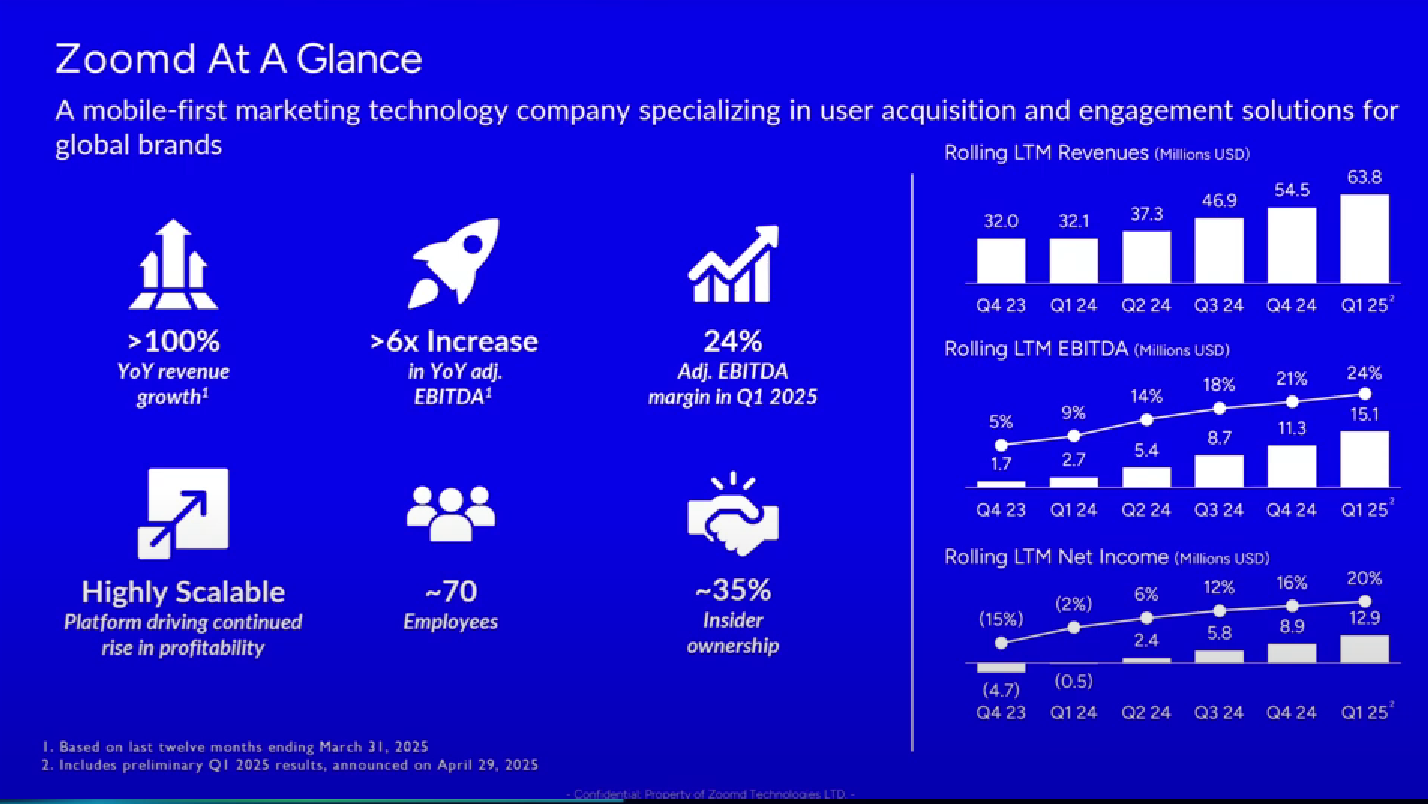

Source: Zoomd Q1 investor deck

“I say once more our only duty is to get paying clients for those logos that you see here. We don't do for them branding, we don't do for them awareness. Some of those brands are just huge, but in the end of the day each one of the names here needs for their earnings, quarterly earnings to say how many new clients they got in how many new clients left.” ‘

Quote by Chairman and Founder of Zoomd, Amit Bohensky.

Source: Zoomd Technologies Company Webcast Lytham Partners Spring 2025 Investor Conference

From their growth, we can deduce that they excel at their only duty. High insider ownership of 35%. Their revenue growth translates to higher and higher net income due to their high operating leverage. Operating costs do not increase in proportion to increased revenue.

This is when I got involved with Zoomd.

Source: AlmostMongolian

This was on May 9th. It did put Illumin to shame at the time. The stock I was just pounding the table on. 55m USD market cap 44.5m EV Q1 revenue up 100% y-o-y, net income 4,5m annualized 18m, record revenue during the weakest seasonal quarter in Adtech. These preliminary results got me to take a position.

I didn’t expect it to move so fast for almost no reason. Meaning no additional good news. Of course the stock was cheap which can be a reason in itself.

Source: Google

Now the situation is basically the same, but the market cap is 105m USD and the EV is 94.5m USD.

The only catalyst for the 84,62% move that I can see is that the Q1 official results were slightly better than the Q1 preliminary results. In the official results, net income was 300k higher, Revenue was 200k higher, adjusted EBITDA was 200k higher, and cash from operations was 300k lower. Not a huge difference. It showed that the preliminary results were never fully priced in, despite causing a 53% move before the official results were released, which highlights the difficulty of determining what is priced in and what is not.

The earnings call also didn’t have anything substantial that they hadn’t said in earlier interviews.

Now that the stock has gone up. I’m hearing people saying they missed it. And I get worried because if they missed it and they are right, it means I should sell. But if they are wrong and haven’t missed it, but are actively missing it, I should either hold or buy more. I need to figure out what all of this means. I have to put the pieces together.

Now we looked at the data. We looked at the data, and what we found surprised us.

If this company continues to grow at its current rate, the stock price is unlikely to remain at this level. Even after rising significantly, it still has a low valuation based on recent financials. So, the market clearly has doubts about the sustainability of their growth rate or even their ability to remain at Q1 level of earnings. This is because it’s still a turnaround story. Starting its turnaround in 2024.

Source: Seeking Alpha Premium

This company has high operating leverage. Q3 2023 was the low point of revenue of 7.1m. And the Operating costs were 2.9m. Q1 2025 had 18.2m of revenue and operating costs of 3.1m. 13,8% increase in operating costs while revenue went up 155% and gross profit went up 186%. Due to this operating leverage, nearly all revenue growth goes straight to the bottom line.

From Q3 2023 to Q1 2024, the gross margin improved from 39,4% to 43.9%. GM is not expected to change much from now on.

Source: Seeking Alpha Premium

Now the cash is piling up q-o-q. They went from unprofitable, declining revenue, and low on cash business to highly profitable, growing revenue, and high on cash business. When they had their weak period in 2023, the stock fell to a very low level, and after they turned the business around, the stock has gone up by 23x from the lows.

Source: Google

With stocks that have moved up a lot recently, investors may think they have missed the boat, but you should not be focusing on the price. It’s a common psychological trap investors fall into. In this situation, it would be called “anchoring effect”. Fixating on some historical price of the stock as a reference point. It’s irrelevant.

The stock will rise more than you think, and it will fall more than you think. Investors should focus on the current valuation and try to predict the company's situation in the future. If Zoomd continues growing the stock will go higher.

Turnaround

The turnaround happened. How did it happen? And how does the way the turnaround happened set up Zoomd for continuous growth going forward?

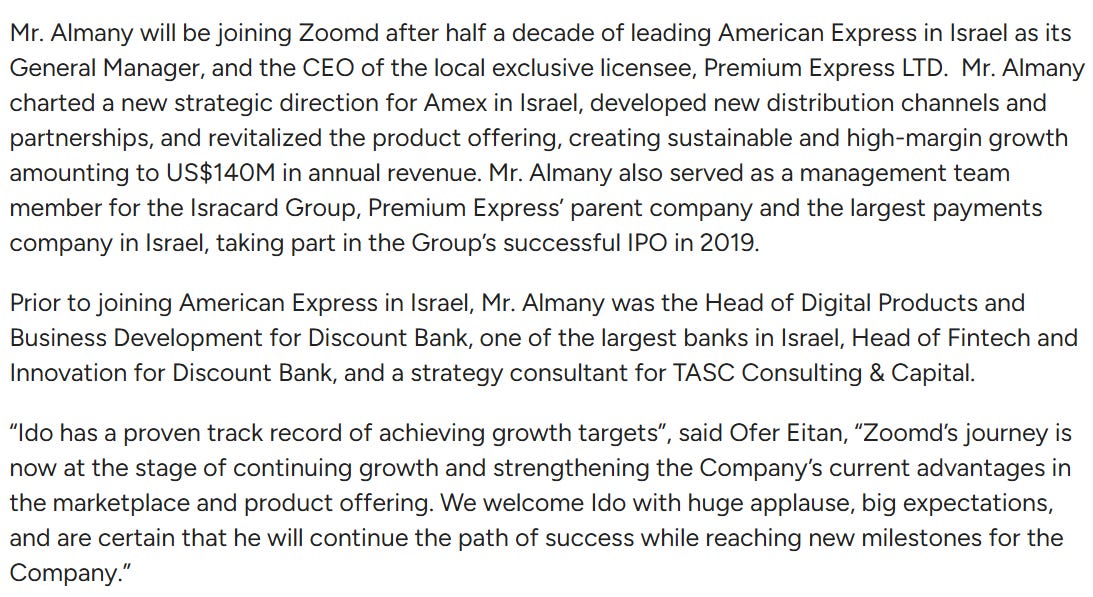

New CEO

Source: https://zoomd.com/zoomd-technologies-announces-appointment-of-ido-almany-as-ceo/

In 8.12.2022 Zoomd hired Ido Almany as the new CEO. He must have had something to do with the turnaround. But he doesn’t do much of the talking; most of the talking is done by the founder and the chairman, Amit Bohensky. The quotes in this article from earnings calls and interviews are from him. He is not a native English speaker.

Bohensky is an accomplished businessman. He even has a Wikipedia page.

He co-founded Unicoders in 2003 and sold it for $2 million in 2007. He founded Focal Info in 2008, and it was acquired by Verint Systems in 2012 for an undisclosed amount. Founded Zoomd in 2012. He served as the CEO of Consist Systems… He has a lengthy list of various involvements.

What did Zoomd do differently in 2024 to turn the business around? Here is Bohensky answering that question.

“It's a combination of several reasons. One of them is that we dropped several engines that we were trying to incubate, and we saw that they are not generating profit, and we decided to go focus on our main strategy performance marketing with our technology. The second is that we optimized a lot of the sales processes and active relation with the client. We've developed some automation tools that help us to interact with them on a daily basis on an hourly base and also this helped to cost reduction the decrease in reduction and that's the first slide that I've showed it which is amazing that while we are going up in revenues and EBITDA we go down in operation cost because of this type of automation.” Founder

Here is the CEO talking about the same subject.

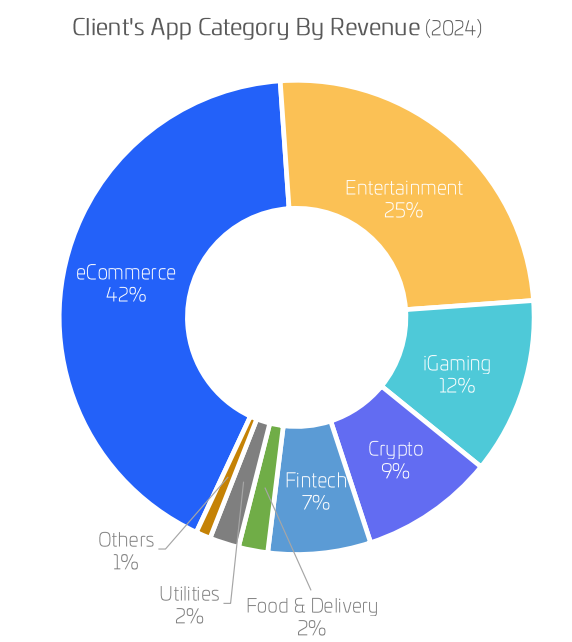

“Past 12 month, we made some key decisions that now provide Tailwinds to our performance. We've launched multiple companywide initiatives centering around operational efficiency and strategic Focus first we took a hard and cold look into each and every one of our business lines ultimately we decided to shut down those that no longer align with our vision and future trajectory as well as bottomline potential that also means that we had to streamline all aspect of our cost structure touching all processes ways of doing business and unfortunately we also had to downsize our Workforce and say goodbye to some dear friends in parallel we set on the offensive deciding to focus the lion’s share of our resources and attention on mobile user acquisition by realigning behind our core competency we reignited Revenue growth we also took some deliberate measures to diversify our client base into e-commerce gaming and fintech prioritizing high margin areas over outright Revenue growth.” CEO

In Summary, they shut down everything that wasn’t working, laid off people, streamlined the cost structure, improved sales and client relations, and refocused on the core business.

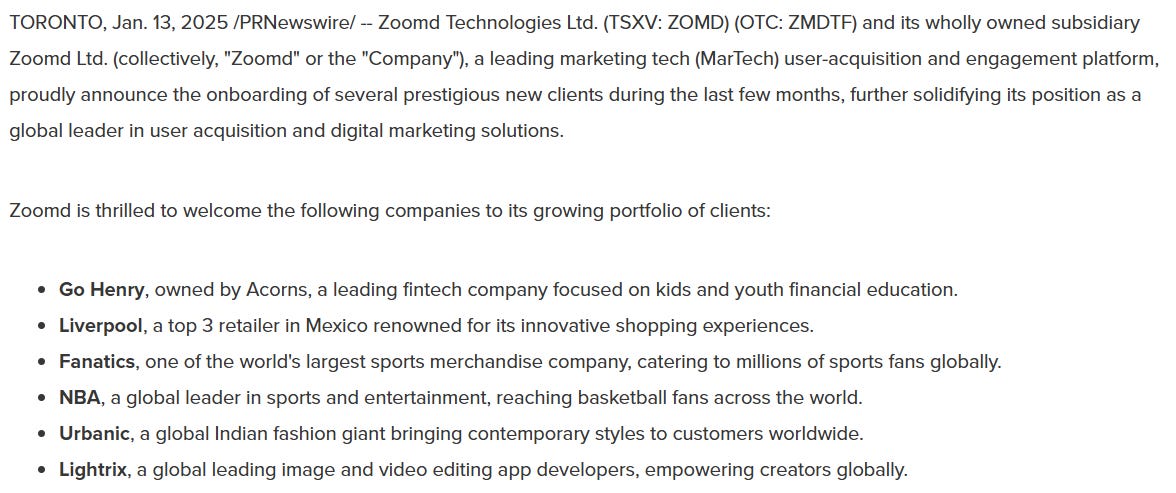

The 2024 growth certainly didn’t come from macro or industry tailwinds. They gained new clients and expanded their business with existing clients. On January 13th, 2025, they announced a group of new clients gained during “the last few months”. I think the revenue from these clients started showing up in Q1, contributing to the record quarter.

Source: https://www.prnewswire.com/news-releases/zoomd-expands-global-reach-with-new-client-partnerships-across-multiple-industries-302349099.html

I asked Grok for the market valuation and revenue of these companies to get a sense of the potential.

Go Henry (owned by Acorns): Acorns, a fintech platform, was valued at around $860 million in 2021 after a funding round, with revenue estimates in the tens of millions annually, though specific figures for Go Henry alone are not isolated.

Liverpool: As a major Mexican retailer, Liverpool's parent company, El Puerto de Liverpool, reported revenues of approximately $6-7 billion USD in recent years, with a market valuation fluctuating around $10-12 billion USD based on stock performance.

Fanatics: Fanatics, a sports merchandising giant, was valued at over $31 billion USD in 2022 after a funding round, with estimated annual revenues exceeding $4-5 billion USD.

NBA: The National Basketball Association generates around $10 billion USD in annual revenue, though it’s a league rather than a publicly traded company, so it doesn’t have a traditional market valuation.

Urbanic: As a relatively newer global fashion brand, Urbanic’s exact revenue and valuation are not widely publicized, but it has raised significant funding (over $100 million), suggesting a valuation potentially in the hundreds of millions.

Lightricks: Lightricks, known for apps like Facetune, was valued at approximately $1.2 billion USD in 2021 after a funding round, with estimated revenues in the range of $100-200 million USD annually

Getting these companies onboard is just the first step. They are not going to give Zoomd their whole marketing budget right away. Likely, they will pay Zoomd 1-3 million USD at the start and see what Zoomd can do with it. And if Zoomd can deliver results, they will expand the relationship. This is how Bohensky explained it in the Q1 call.

“Can you walk us through a typical process of when a client decides to increase their budget with Zoomd?

certainly most clients starts with one or more target geographies as campaigns begin as the campaign begin deliverings and the client is satisfied they often choose to increase their budget in those existing markets or expand to additional countries since we operate in performance marketing space our goals as directly tied to our client results if we deliver the client naturally wants to allocate more of their budget to zoomed if we don't we won't go it's a very result driven module that aligns to both sides”

This means that when Zoomd announced it's signing NBA, it’s not that they are now going to make a certain amount of money from it; because the NBA is a big organization and it will necessarily be a big deal. Because NBA is big, it has more potential, but it could end up being one campaign $1 million in revenue, and they leave Zoomd or $100 million in revenue annually from NBA, based on Zoomd's performance and the gradually improving and expanding customer relationship.

With Zoomds' largest client, they have expanded over the years and gained more of their marketing budget. This client is Shein. They sell fashion online with about 40-50 billion USD of annual revenue.

Source: Zoomd Q1 investor deck

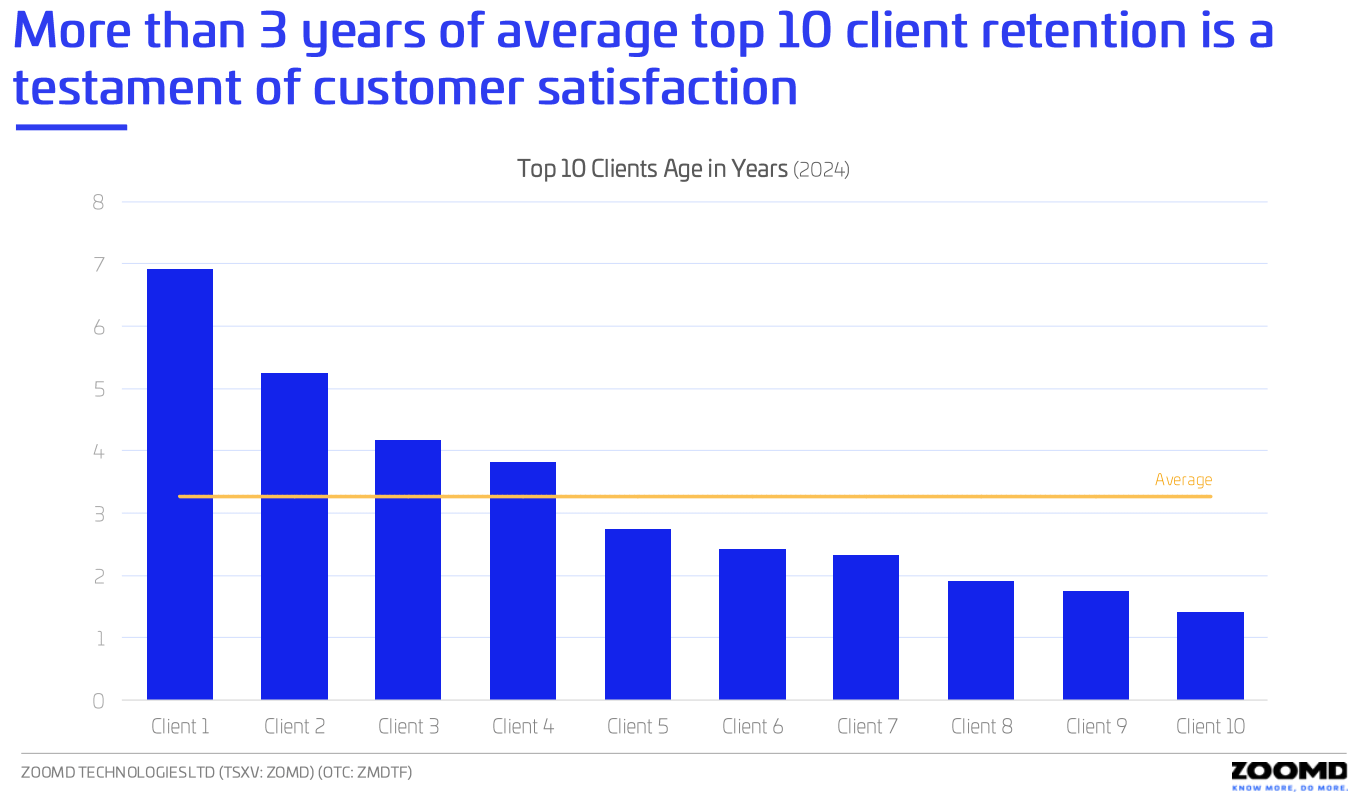

According to the chairman Shein is about 35% of their revenue. This has also been presented as a risk for Zoomd because losing this client would be devastating or Shein just reducing marketing would hurt Zoomd. But Shein has been with Zoomd for almost 7 years now and they have a good client retention overall.

Source: Zoomd Q1 investor deck

“our biggest client been with us for more than six years and continue to grow with us” Bohensky referring to Shein.

When stock was crashing during the height of the tariff fears. People feared Shein would be reducing spending. As it is a Chinese company. This is Bohensky answering the question of someone asking about Shein in relation to the tariffs.

“tell Paulo Yeah that we are managing more than more than 14 countries to Shein and UK and Germany and France and other domains are so big we can't share how the spread goes But we are far from disappointing these clients and and that client in particular and as of now he hasn't changed anything including in risky areas”

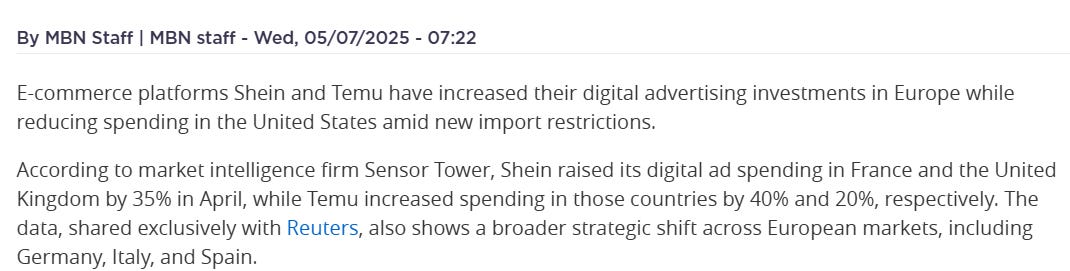

Source: https://mexicobusiness.news/ecommerce/news/shein-temu-shift-ad-budgets-europe-cut-spending-u

Shein is boosting spending in Europe while reducing it in the US.

If Shein provides Zoomds 35-50m USD of revenue annually it’s would be a fraction of their marketing budget. Sheins’ marketing budget is not public, but based on comparable companies of similar size it’s likely way over a billion annually. Which leaves a lot of room for growth for Zoomd if they keep delivering results for Shein.

In Q1 85% of Zoomd the revenue came from 5 clients.

“for example for one of our top client we operate in more than 30 countries and 10 countries for another top client that same client increased the number of countries we operate in by 50% during the last quarter” Q1 earnings call

This should provide some growth in Q2, as Q1 would not reflect this expansion fully.

As I covered earlier, the Gross margin has been improving, but we should expect it to be around the Q1 level going forward. This was Bohemsky answering, covering the Gross margin question.

“Our gross margin moves between 40 to 43% it used to be between 38 to 40% now it's between 40 to 42 So 43 this means we optimized a little bit more the gross margin So we are doing more of the same but we are now able to scale it more So we are getting more clients on the same rate but we can get more of them and expand within them”

“We are reaching to the stage that in terms of optimization the system is very optimized and this is why we went out and got a bunch of new clients and also we are going within the new clients and we finally can grow within the existing client even more Those are giant clients billions of dollars of clients there have they have massive budgets we are not even a fraction one divided to 1,000 is not even our budget within their marketing budget as a whole So there's much to grow within those clients but the combination of getting new clients and growing within the existing clients is what now drive us to grow”

Now it’s all about acquiring new clients and expanding with existing ones.

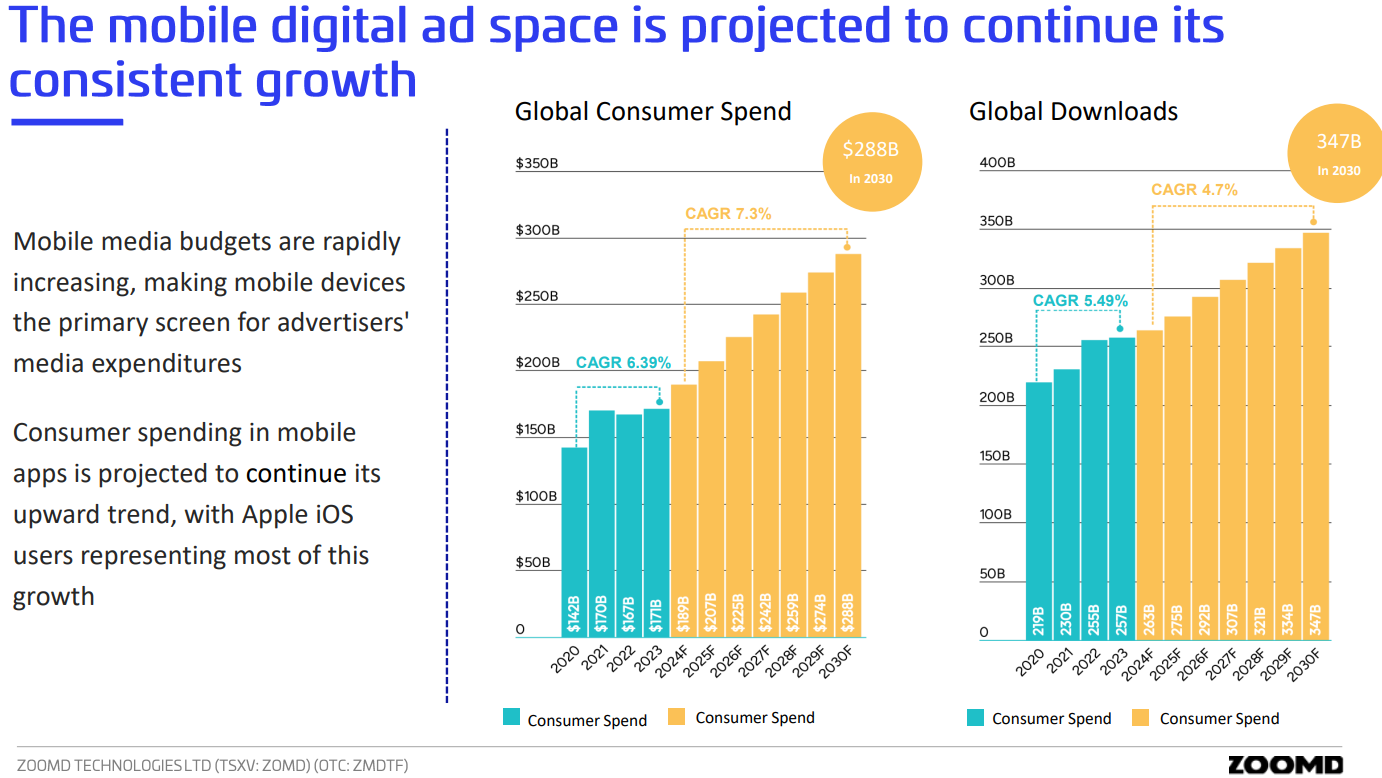

There is also a sector tailwind.

Source: Zoomd Q1 investor deck

This sector is extremely competitive, so this rising tide is not going to lift all boats. It will lift Zoomd, because Zoomd is competitive.

Capital Allocation

If the cash pile continues to grow as it has been, the next question for shareholders is what they will do with it. The chairman has been pointing to a potential acquisition where Zoomd would focus on acquiring clients. Without dilution, if Zoomd is trading at a low valuation.

“The purpose of the money now is to accumulate it, and when the time comes, we're going to give few quarters to continue to be rewarded by our investors to show consistency, and when the time come we will do one or two potential M&A, mainly to acquire more clients”

About buybacks

“Are you considering an NCIB share buyback?

We are considering that option a lot as we are keeping our options open If we go and raise money even a little bit then we can't be do of course an NCIB We can't raise money and do the buyback at the same time That's why we keep that option still open and we are not doing that yet but we are aware that if we do that it will show of course a token of face and investor will love that uh we we continue to hold our card at the moment about that”

About the possibility of raising money

“only if the target that we find is that big that will need a raise can also consider the valuation because we not going to dilute in a valuation like that but it seems at the moment that the cash that we are generating and that we generated till now will be sufficient So it it depends it depends on the next couple of quarters and how we perform for that particular decision

In summary, M&A should be expected sometime in the future. Buybacks potentially. If the M&A target is big a raise is possible, but they think that likely the cash they are generating will be sufficient and they don’t want to dilute at what the see as low valuation allthough we don’t know what they mean exatcly as the point where valuation is high enough for dilution to be in the table.

Zoomd is looking for acquisitions, and according to Bohemsky, they have also received a lot of interest from potential buyers for Zoomd.

“Have you had any interest from others to potentially buy Zoomd outright?

Yes Zoomd is constantly being court shipped It's not a plan that we have We believe that the engine that we've built is not just a slogan engine It works on particular industries and it proves itself and and you know in the field of marketing loyalty is not a term that you use When I say I have a client for five years and another client for four years and another client for six years like unbelievable that they stayed with us and they continue to grow with us uh this immediately attracts potential buyers from different type of the industry We have talks but there's nothing that we put in stone because our purpose is our target is to grow the company”

Summary

When it comes to Zoomd upside it’s all about does the growth continue. I covered the factors that have led to the turnaround. New clients Zoomd has recently onboarded with a lot of potential for expansion and a lot of potential for expansion with the old clients. It’s looking pretty good even with the macro situation looming in the backround. And Zoomd can even grow with macro headwinds with strong performance as they are still a small player and only have a fraction of their clients marketing budgets so if Zoomd delivers results they can increase their share and grow despite macro.

In the most recent interview with Bohemsky, he says “momentum continues” twice and “momentum will continue” once, referring to their revenue and net income. This was May 29th, so already 2/3 of Q2 done as he says this, so unless he is being deceptive, Q2 should be another strong quarter.

Looking at the risk/reward, I think it’s still very favorable even with the stock having gone up a lot recently. If Zoomd can keep growing at 50-100% annually, I see +300 million USD market cap as inevitable, and from there, who knows how high they can get to if the multiple starts getting expanded when the stock starts getting valued like a growth stock.

If they can maintain the revenue level achieved in Q1. Meaning annual net income of around 19.2 million USD. The current EV of 100m is still quite cheap. And I think whether the stock goes up or down in this situation will be mostly based on sentiment and macro. One could make an argument that the P/E is too low and it would re-rate to 200-300m just based on this scenario, but I never base my investment thesis on the assumption of re-rating without a catalyst. That’s just a horrible investment thesis. Assuming Bohensky’s “momentum continues” is true, this scenario should be at least what Zoomd will achieve in the short term. And this scenario could be our margin of safety of some kind.

Then the ultra-bearish scenario would be some kind of black swan event. Macro getting much worse(global recession) or Shein leaving Zoomd. These are always possible, but not likely or predictable.

My own positioning will stay the same for now. Holding. I said I wished I had made it a bigger position originally, but now, after the stock has gone up, the stock price has made it a bigger position for me, and I’m happy with the position sizing for now. Based on my current investment thesis, I prefer not to sell any shares when the market cap is below 200m USD. Unless there is a fundamental change to the thesis, or I see some insane opportunity elsewhere and sell some Zoomd stock to buy that.

Zoomd is one of those stocks that has the potential to become a long-term investment for me.