Voxtur Analytics: Focus on Blue Water

Why I am adding to my worst investment ever

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program which means I have a financial relationship with Seeking Alpha.

Voxtur, Voxtur… Where do I start?

Voxtur is a collection of different real estate technology- and technology service businesses bought by the current CEO and executive chairman Gary Yeoman. It’s kind of a synergistic, cross-sell strategy. He took control of this company Ilookabout a few years ago and started shopping. In 2021-mid 2023 another guy took the CEO position until he got pushed out(This is my interpretation of the situation) and Gary came back as a CEO. I can say Gary because I have interviewed him on the AlmostMongolian Youtube channel. I expect the rest of you to refer to him as MR. Yeoman.

Here is what Gary bought.

Acquisitions: purchase price at the time USD(Most of this was done through share issuance at higher prices than the stock is now)

2019 Ilookabout market cap before the below acquisitions was 15,5m(Clarocity included)

2020 APEX 4.8M USD

2020 Voxtur technologies 23,5m

2021 Anow 22m

2021 XOME 15m (sold for 30m 1.11.2023)

2021 RealWealth 4.2m

2021 Benutech 17m

2022 MTE 3,2m

2022 Bluewater 101m

Current market cap 55.4m USD at 0,115 CAD per share

fully diluted market cap 72m USD at 0,115 CAD per share (took fully diluted share count from the corporate presentation and added an approximate of remaining BW shares to be issued as I don’t think the corporate presentation included those)

EV=After the recent business unit sale the debt should be around 25m USD and the cash and cash equivalents we don’t know for sure rn, but maybe around 6-12m USD.

I’m not vouching for any of these numbers.

Source: Voxtur Analytics corporate presentation

Here is some reasoning for the acquisitions.

As you can see there is a lot of stuff in Voxtur so I will not go through everything in this article. It would make this way too long. I will write about some of the other businesses within Voxtur in other articles here in AlmostMongolian Substack.

Now I will go over Bluewater.

The reason why I’m going over Bluewater specifically in this article is because it’s the main reason why I’m adding to this stock. The main reason why I keep throwing money into this seemingly bottomless pit.

Maybe we found a bottom at 0,095 and it’s now at 0,115, but I will never underestimate Voxturs’ ability to go even lower. But I will always buy a great risk/reward despite the chance it could go lower.

Bluewater

Source: Voxtur Analytics corporate presentation

They do all that stuff mentioned above and get fees for it. And because it’s completely digital they can do all this stuff very fast and efficiently and they have a very scalable business. But I’m not gonna get too deeply into the minutiae. If you’re unsophisticated you have to Google that word.

What I want to focus on is the clients, growth, and earnings potential. Everyone can make a product sound great. But is it performing? Are paying a cheap price for it? This is the most important part. And I think Bluewater is very cheap within the Voxtur package.

The way BW was bought also aligns incentives very nicely. The purchase price was 101m and only 30m was cash the rest was shares and the shares are going to be issued gradually within a 4-year time frame. So the Bluewater people are incentivized to stick with the business, because if they do not it will hurt their own wallets. So far it has hurt their wallets regardless because the stock was around 50 cents at the time of the purchase, but that is beside the point. It also tells how committed Bluewater people are to this merger. They supposedly had a 150m all-cash offer from a bank(not confirmed), but they went with Voxtur because of the benefits they saw with merging with Voxtur.

Bluewaters’ main investor was Ricepark Capital which is also their client(That should tell you something). Their founder and CEO Nicholas Smith became the Chairman of Voxtur. And also will own a lot of shares.

The founder of Bluewater Al Qureshi is going to be a very large shareholder too, but in addition he bought a large amount of stock from the open market when the stock was at 28 cents.

Source: ceo.ca, SEDI insider filings

These people really believe in the combination of Voxtur and Bluewater.

When they bought BW in 2022 for 101m USD. This read on the PR. When I start with these numbers remember the current market cap mentioned earlier.

“Blue Water is a high-growth business that had approximately US$11.4 million of revenue and US$6.7 million of net income for the fiscal year ending December 31, 2021. For the trailing twelve months (“TTM”) ending July 31, 2022, Blue Water generated approximately US$18 million of revenue and US$11 million of net income, with increasing run rates for revenue and net income during that period1.”

https://www.globenewswire.com/en/news-release/2022/09/22/2520882/0/en/Voxtur-Closes-Acquisition-of-Blue-Water-Financial-Technologies-and-Announces-Expansion-of-Credit-Facilities-and-Private-Placement.html

If it was generating 11m USD net income right now it would certainly be worth more than the Voxtur market cap. It’s high growth, tech, and high margin. It also supposedly runs with only around 30 employees. And supposedly has fixed costs of around 600k per month which kinda makes sense from that profit margin 18-(12*0,6)=10,8. I say supposedly because these are things said by the management and they do not provide detailed financials for every specific business unit and this was a private company before they acquired them. During the 11m of net income period that is 366 666$ of net income per employee.

Source: Visual Capitalist

It would put it eight between Apple and Alphabet(Google) in the Fortune Global 500 list for profit per employee. This is a great business.

But the thing is Bluewater’s revenue dropped to below their fixed costs of 600k per month and because of this in q1 and q2 they lost money with Bluewater. In q3 according to Gary in the interview we did recently BW did around 500k-600k of revenue in July and August but raised it to 1-1.1m in September and supposedly higher than that in October. This raised the question. Why did this large drop happen from 2022 and is it an indication of weakness in Bluewaters’ business?

I would argue no. It is a temporary effect. In the future Bluewater should exceed the 11m of net income annually easily because their client base is much larger now than it was then. Their offering is also much more expansive than then.

So the revenue roughly doubled in one month from August to September and before that, it dropped by around 50% from q4 to q1. Remember Al Qureshi bought stock right when this happened and there is a reason for it. So this fluctuation in revenue is not just an effect of transaction levels in the market. Mostly It has been an effect of clients leaving involuntarily or clients pausing transactions momentarily, clients being added and clients ramping up transactions.

Incompetent Investo and Sukkana from Inderes Voxtur public and private forum have done a lot of heavy lifting with BLuewater DD. It’s quite impressive. They also do not mind me using their messages in this article even from the private forum. They have basically used websites like securitytrails.com to find the new clients of Bluewater and we have a lot of evidence that these are accurate findings. With some guidance from Incompetent investo, I was able to find some of these unannounced or unnamed clients as well. And this is completely legal to do it’s public info, but Voxtur does not most of the time release the names of the clients because they are saying the client doesn’t want them to do it they say for example “Voxtur Announces Exclusive Strategic Partnership with Top 3 Mortgage Originator and Aggregator”.

Basically using the the info from these 2 guys coupled with parsing of different pieces of information and words from the management we can get a picture of what is going on in this business.

So I will go client by client and what we know so far.

Roundpoint revenue is either 287.8m, 464,5m or 148m from different websites.

Most of these are private companies so we don’t have accurate financials easily available these revenue numbers are from me going into Google and typing x company revenue and there are different sites with different answers. So it is what it is, but I do it just to give something we can use to try to determine how big the particular client is.

This is the only client from what Incompetent Investor and Sukkana found that was an old client(pre-acquisition) that went back to 2021 and this was their largest client according to Gary. This client was lost because Freedom Mortgage owned Roundpoint and sold it and according to Gary the condition in the sale was that Roundpoint was forbidden from using Bluewater because they intend to start using Bluewater themselves. The reasoning for this was that Roundpoint had a lot of entities they were selling to and Freedom wanted to onboard those entities to the new platform they were going to build with Bluewater. And Freedom is much larger than Roundpoint so this was basically a revenue deferred situation and they should generate more revenue later. Bluewater was generating 500 000$ from RoundPoint according to Gary and I would guess they lost that revenue at the beginning of 2023 based on financials.

Source: Voxtur Corporate Presentation

Revenue: 1.6b according to Zippia or 5.2b according to ZoomInfo. Who to trust? Anyway, it’s a big company.

This was found in March. Gary said this in my first interview with him in May 2023 about Freedom

Source: Youtube Transcript

If he was saying this stuff in 2021 the stock would be flying, but it’s 2023. Different times.

I don’t know if that was a slip of the tongue that he said Freedom by name because after that he has avoided mentioning Freedom by name by talking about a client that sold RoundPoint.

In our second interview in August 2023 he said they had only reloaded 48 of 580 of their clients in that platform. So they seem to be coming back slowly, but I expect more than 500k per month after Freedom has fully come back.

I also asked in our October interview whether they had fully ramped up with their mystery top 3 client they press released in the summer(Which is probably Freedom) and he said they have not. But considering they already had gotten to 1-1.1m a month in revenue in September without this client ramping up. I would guess this means they are ramping up with other clients that I will look into next.

AD

Get a 7-day free trial and 30$ discount on your first year of Seeking Alpha Premium with my Affiliate link: https://www.seekingalpha.link/3N9WBS8/2QZRGT/

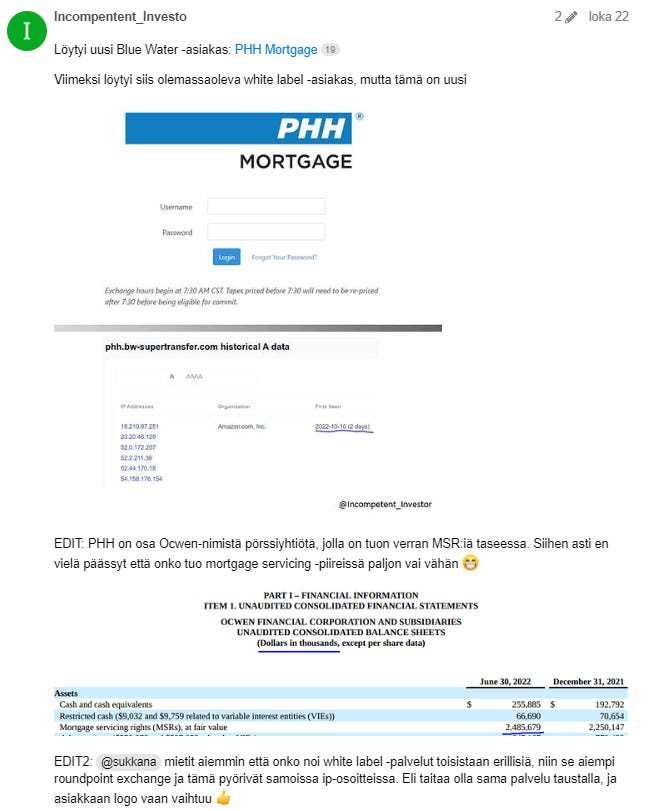

And PHH mortgage is either 732.4m or 1.4B

I suspect this client was this PR. This was found in October 2022

https://www.voxtur.com/voxtur-announces-strategic-partnership-with-top-servicing-aggregator/

TTM revenue 1,1B USD. This is a public company so the revenue number is accurate.

The live version was found on April 4th, 2023.

Gary also in mentioned in our last 2 interviews “a very large client who was taking a large piece of our business or you know providing us with a large piece of our business” “with MSRs you know they were our best client” (I suspect this might be PHH or Texas Capital bank) That hit some kind of limit which caused them to have to pause trading MSRs. And this client was still not fully back in. So we have this client that hit their revenues and Roundpoint. Both from external reasons.

This is important because we want to know why has the revenue been weak this year and we need to know that it’s not because of losing market share. And as we can see they are gaining market share from all these new clients added.

Revenue 62.6m

Source: Youtube, Mariusz Skonieczny

https://www.nationalmortgagenews.com/news/planet-home-lendings-10b-msr-buy-increases-portfolio-by-over-10

There is another confirmation of this method. We can see Village Capital using Bluewater.

ServiceMac revenue: 102m

Midwest loan services revenue 22m

This one also confirms this method as the PR from Voxtur announcing this client was released a couple of hours after this guy found this client and posted it on the forum.

https://www.voxtur.com/voxtur-signs-exclusive-platform-agreement-with-the-mortgage-collaborative/

This client will be more of a gradual ramp-up because it is a mortgage collaborative that has 262 members who are small- and mid-sized lenders. They will adopt it gradually, but this client gave us some extra info on Bluewater and a lot of good signs. For example, before BW TMC had Optimal Blue and Phoenix as their preferred partner and now they are calling BW solution the TMC CapTrader and that sits on the top of the page.

Source: The Mortgage Collaborative

And they have this page for TMC Cap Trader when you click learn more. They don’t even have a page for OptimalBlue(What’s with the color Blue?) and with Phoenix they have a very basic page. Because these other solutions still exist within the preferred partners section page the nature of the exclusivity is still kind of questioned. It says right there in the below picture it’s exclusive, but why do they still have these other ones? I have asked Gary and the answer was not quite complete. I sent a message to Jay Patel but no answer. atm I’m done asking about it.

Source: The Mortgage Collaborative

The point is that Bluewater is clearly displacing these other solutions. TMC looked at Bluewater compared to Phoenix and Optimal Blue and decided Bluewater is better for our 262 members.

And consider that Optimal Blue a business Bluewater displaced here a couple of months ago got sold for 700m USD

https://nationalmortgageprofessional.com/news/ice-black-knight-announce-deal-sell-optimal-blue

“Under terms of the agreement, Constellation will acquire Black Knight’s Optimal Blue business for $700 million, the companies said in a news release.”

TMC also allows us to get to see how this platform works because they put 3 lengthy presentations on YouTube. They are clearly pushing this.

Source: youtube

https://www.voxtur.com/voxtur-analytics-announces-insurance-for-its-due-diligence-solution/

After TMC, they announced their fully insured loan due diligence product. This basically allows them to review loan portfolios very cheaply, very quickly and they can review 100% of the loans while usually only 10-20% of the loans are reviewed. They can do this because they developed a digital process to do it. And the review is insured by Lloyds of London. This is a big differentiator from the competition. Detailed showcase in the first YouTube video in the above picture.

.Revenue: 14.3m

The most recent client found. Not much to say about it.

According to these guys who did this DD Roundpoint was the only client they found that was there before the Voxtur Acquisition. Others are new additions since the acquisitions. And I‘m sure there are clients that haven’t been found with these methods.

As we can see Bluewater has had big client growth during the Voxtur era, but that has not yet shown up in the financials, because of the clients being slow to onboard fully and the market being pretty slow in general, coupled with other issues I addressed earlier. But if Bluewater was able to do 11m of net income without these new clients when their biggest client was Roundpoint and now they have at least 3 clients bigger than Roundpoint. When these clients are fully onboarded and the market improves a bit. What is the earnings potential? All I will say is that it’s much more than 11m. And what is that company worth? Definitely more than Voxturs’ current market cap. I would even say it’s worth more than their fully diluted market cap and debt combined.

And this is just one of their businesses. Their best business for sure, but they have other valuable assets as we just saw they sold one for 30m.

Summary

At current prices, Voxtur is a great risk/reward IMO and I like adding at current prices. This article is pretty long and I didn’t even cover everything about Bluewater let alone Voxtur. So I’m going to write about Voxtur in pieces. It’s quite interesting to dissect my worst investment and try to figure out whether it could be my best investment someday or not.

Why not wait to see the company become profitable before adding? You probably buy at a higher price, but at least you know the company has turned around.

Thank you, if my brokerage allows buying sub-$1 stocks I will consider this (US pink sheets).