Ensign Energy Services: Ignored bull market in onshore drilling.

There is oil under the ground.

I have 2 oil drilling plays Ensign and Transocean. Other drills on land and another on water. There has been a lot of buzz around the water Drillers, but not for the land drillers. So naturally, I will wrote about the latter.

This investment is part of my larger oil thesis and I’m playing it through various companies mostly E&Ps, but there are some service companies that have gotten my attention like Ensign, CGG, and Transocean. These service plays are also a hedge to the capital discipline thesis not playing out as expected which would hurt the E&Ps, but it would benefit at least short- and mid-term the service companies. While I kind of partly buy that capital discipline thesis. I still think there will be higher capex in the oil sector over the coming years and if there is a repeat of “drill baby drill” these service companies will moon and all of my service picks have similar characteristics high debt, improving business fundamentals, and no dividends or buybacks yet.

Why would I prefer companies like this over their dividend-paying, low-debt counterparts? Answer: the valuations are still low. The service companies get higher multiples than e&ps and they should. The businesses are more diversified and have way less windfall tax risk, other political risks, less operational risk, and no geological risk. But I don’t want to pay high multiples and I still want exposure to the sector. This forces me to pick companies that are not fully priced yet. They are not yet obvious picks for the investment community to play oil services. Maybe they have not yet started capital returns or have not yet achieved consistent profitability. So I try to find companies that will meet these criteria in the future, but not yet. Like picking a dirty orange that nobody wants off the floor and cleaning it up and then selling this orange to a store at full price when it looks nice and clean. Forget the ethics of the previous example. You get the point.

I have been increasing my Ensign position recently whenever the stock goes sub 3,5 CAD. I’ve been inspired by the recent earnings call from Precision Drilling. Which I will quote in this post quite a lot. Precision and Ensign do the same thing in the same countries so their businesses are affected by the same factors. They are similar-sized companies so it’s a good comparison. The precision drilling stock got killed from missing earnings expectations and that was mostly, because of their massive compensation, the business itself did great and the stuff that was said in the call sounded really bullish about the sector. So I will use stuff from Precisions’ earnings call and corporate presentation to make a bullish case for the sector and then I will explain why I prefer Ensign over Precision.

Precision q4 call quotes

“For 2023, Precision's strategic objectives are: one, elevating our high-performance, high-value strategy, which encompasses safety, rig efficiency, Alpha and EverGreen and most importantly, our value proposition to our customers; two, maximize free cash flow, including driving field margins towards 50% in the North American drilling business”

(I don’t know what “field margins” are exactly. What is included in that? Comment if you know. I could not find it on Google, but I would expect it means something like gross margins. 50% sounds pretty good for a usually low gross margin business. The thing is whatever this means for these companies increases in rates have a massive impact on the bottom line, because the operating expenses are so low compared to the revenue[at least they should be. Looking at you Precision] if you have higher gross margin revenues it translates to the bottom line in a massive way and you can have a full repricing of the stock.)

“Last quarter, we achieved and are sustaining of 100% or sold out utilization with our Super Triple rigs in the Canadian market. We reactivated and are sustaining approximately 90% utilization on our U.S. Super Triple fleet.”

“Waqar Syed

Kevin, I didn't hear you clearly. For this rig upgrade, the super spec in Canada, did you say that the day rate was mid $40,000 a day. What was the day rate at which it was contracted?

Kevin Neveu

Waqar, yes, thanks for the question. And I understand there may have been some muffling on the call. So I'll clarify that. What I was saying was the day rate is in the mid-40,000s. So I think that would be in the range of $44,000 to $46,000 per day.

Waqar Syed

Well, is this a new high or for that class of rig in Canada?

Kevin Neveu

Certainly, it is…”

(New high. Nice.)

“Kurt Hallead

Right. I think what we've been hearing so far is got leading-edge rates are, I don't know, 35,000 to 40,000 a day, sort of kind of average rates in the fourth quarter were around 32. So that leaves a lot of headroom for this repricing without even rate count going higher. Is that fair?

Kevin Neveu

Yes, we would agree.

Carey Ford

Yes, and that's reflected in our Q1 guidance.”

Precision corporate presentation relevant slides

Source: Precision Drilling corporate presentation

This all sounds bullish. These are mostly facts too. Only forecasts are on the first slide. I don’t how much this recent natural gas price crash will affect drilling activity, but I’m not playing this sector for the next quarter and my thesis is based on oil. Natural gas is just gonna do whatever.

I’m gonna link the Ensing corporate presentation here. It’s not as up-to-date, because they have not reported q4 yet, but I would recommend taking a look at it if you’re unfamiliar with the company.

https://www.ensignenergy.com/wp-content/uploads/2023/01/2023-01-ESI-Corporate-Presentation.pdf

Some stuff from Ensigns’ presentation:

“Long-term international contracts, short-term North American contracts • As leading-edge pricing continues to improve, short-term contracts deliver more favorable exposure to pricing dynamics • Across global operations = approximately $1.14 bn in contracted revenue with 33% of our active fleet under long-term contracts (≥6 months)2 • Weighted average contract tenure = 10 months”

This is not like offshore where contracts can be very long and you might not get to take advantage of price spikes. This company will regularly have contracts rolling over and have the ability to renegotiate them at higher rates.

Revenue distribution USA 56% Canada 28% international 16%

Source: Ensign Energy Services corporate presentation

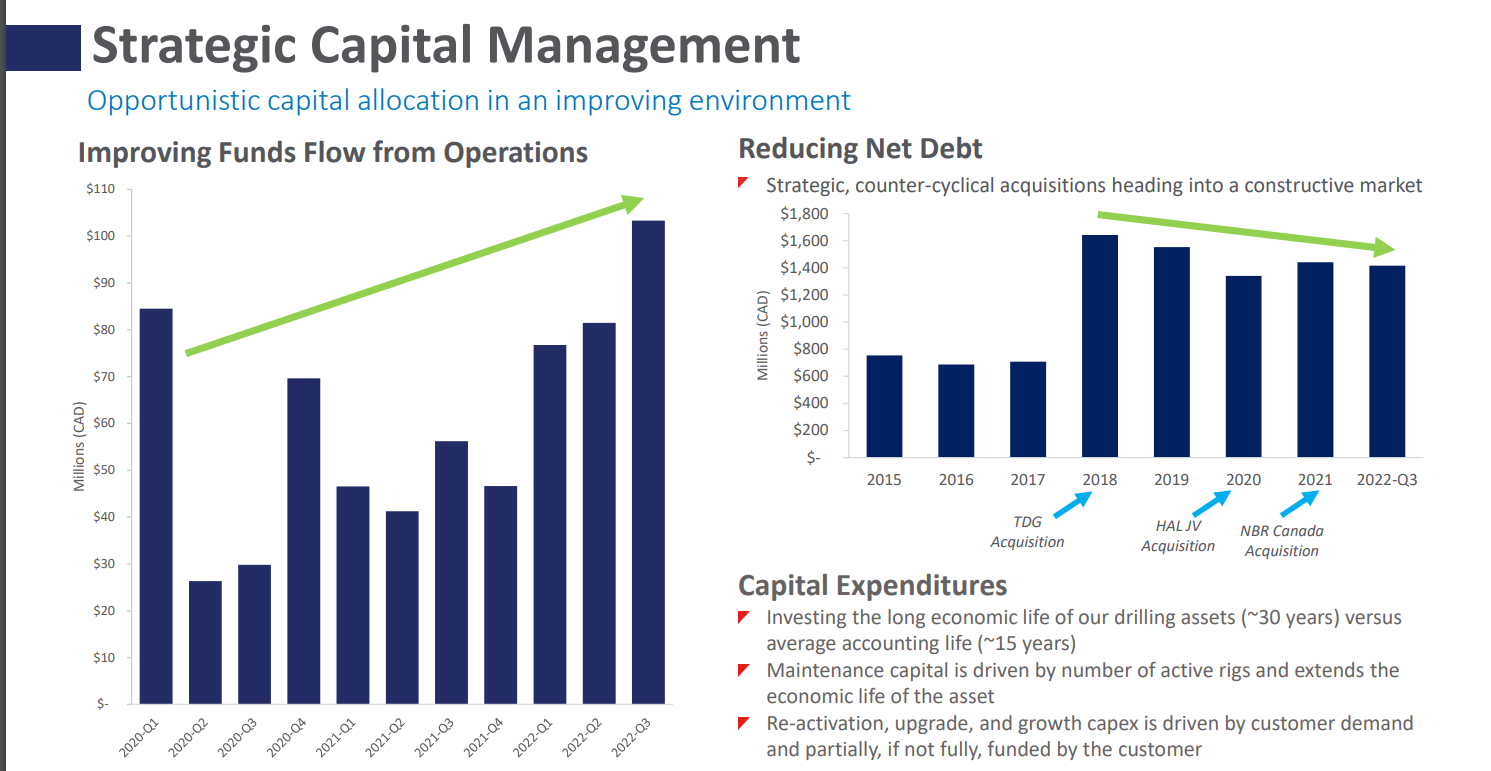

100 million CAD of funds flow in q3 compared to 620 million CAD market cap. I know it’s funds flow, but the increase is quite high and everything points to the direction that it’s going higher.

DUCs

Source: MacroMicro

I also want to bring up the DUC count in the US. Which means the amount drilled but uncompleted wells. As we can see E&Ps have been depleting their inventory of DUCs. The last time it was this low was in 2014, but you can see how much lower US oil production was at the time. DUC count tends to track oil production, but this changed after the pandemic hit. We have not seen a disparity like this before where the DUC count is so low compared to oil production. I would expect as the world returns to normal so would this.

A lot of these DUCs left are so-called “dead DUCs” that for one reason or another are not really viable targets to complete. By using up their DUC inventory E&Ps have been able to increase production quicker and with less cost, but because the best DUC inventory has been used up to increase and maintain production E&Ps will have to do more drilling of new wells using services of Ensign which gets around half of its revenue from the US.

So now we are all excited and want to have exposure to the sector. There are many options, but for these kinds of plays, I like the obvious choices if they have enough torque. I would look at Ensign and Precision because they are pretty much pure drilling plays. They have financial leverage and they have exposure to both US and Canada, both have a small international segment. But for me, the obvious choice out of these two is Ensign.

Why Ensign and not Precision?

I have 2 reasons for this. First is that Ensign is discounted to Precision and I don’t really know why exactly it is discounted so much. Almost everything in these companies is comparable, but Ensign trades at a 620 million CAD Market cap and Precision at a 1,1 billion CAD market cap. Ensign has 1,46 billion CAD of debt which is 300 million more than Precision. So there is that. Their EV is pretty comparable to Precisions EV is 200 million higher. But you have to remember when looking at EV that you are not buying the debt or the preferreds when you buy a common stock. I know it’s obvious, but it seems to get lost with people sometimes. If you have increasing earnings while debt is staying the same it amplifies the up move in the stock price, because the stock is getting derisked as the debt looks less and less scary. I think Ensign will benefit from this effect more. Their revenue is basically the same Ensign has not reported their Q4 yet, but I expect that to be higher than q3. In q3 both companies had the same revenue and Q3 was a turning point for both companies as they both reported profits after a long streak of money-losing quarters.

Source: Sedar

The Second reason why I prefer Ensign is management alignment with shareholders. While Precision had a great quarter in many ways it did not translate so much to the bottom line, because of the massive compensation the management got. “The higher expense in 2022 was primarily due to our increasing share price and the impact of a higher performance multiplier” So the stock price goes up mostly for external reasons and the management rewards themselves handsomely. I prefer management owning the stock rather than this as an incentive. This compensation based on share price moves incentivizes short-term thinking.

Consider that operating expenses for Precision were 180,9 million in 2022. Most of that was “cash settled share-based incentive plans” while Ensign a company with comparable revenue had operating expenses of 54 million. Ensign has some share-based comp too, but nothing out of control like Precision has. The incentives become even more clear when we look at insider ownership of the two companies Ensign has 36,92% insider ownership while Precision has 0,68% insider ownership according to Yahoo finance. I’ll rather ride through this what I think will be an upcycle with Ensigns’ management.

Conclusion

This is a sector play reliant on market conditions. I think the demand for rigs will be going up in the coming years and the supply response will be muted, because of PTSD from the brutal Covid bear market and both material costs for building new rigs and interest rates have increased a lot. Ensign is my choice for taking advantage of this supply and demand unbalance. This is not one of my top picks, but I have recently added a lot because the market has given good prices to add. I’m planning to reduce this position after we get to around 1-1,5 billion CAD market cap, but I do think we have the potential to go much higher in the right conditions. In a drill baby drill scenario who knows how high this could go, but that is not my base case. The plan is to buy now, wait until fundamentals improve, and sell when the company looks nice and pretty to everyone.

These are my personal opinions and should not be taken as investment advice.