Eco Atlantic Oil And Gas: Rare Exploration Bet

Multiple paths to success(paywall removed)

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program which means I have a financial relationship with Seeking Alpha.

Eco Atlantic Oil And Gas

This is one of my longest posts and sometimes the posts don’t fit in the email. Substack almost always warns me that “Post too long for email” and it still usually fits, but not always. If it cuts off abruptly for you the rest can be read from the website or the Substack app.

I like to invest in commodity stocks, but I don’t like to invest in pure exploration and development stocks because these stocks tend to be dilution machines with low success rates and require a higher level of expertise to get an edge over the market. That being said. I like Eco Atlantic Oil and Gas which is a pure exploration play. It’s my most recent pick.

Eco Atlantic has many paths to stock price gains. They have multiple assets in the best oil exploration spots in the world. They have cash coming in from a deal that allows Eco to avoid dilutive raises and they have another deal that reduces their share count by 16,16% on a diluted basis.

These attributes make Eco distinct from its peers in the exploration space. They should not have to raise money in the foreseeable future and instead of increasing the share count Eco will have a lower share count.

The stock is also trading at a very low price compared to what it could trade at if even one of its assets starts gaining traction.

Source: Google

We can see from the stock price that Eco has disappointed investors in the past, but as we know, there is a difference between price and value. I think this long stretch of decline has sucked all the excitement out of this stock and allowed it to get to a price where it has become very asymmetric. Now we are getting close to the multi-year lows at the same time as near-term catalysts are approaching.

Financials, Valuation and Capital Structure

market cap now= 48.26 million USD

market cap using post-Africa Oil transaction share count(USD)= 40,46 million USD

Source: Seeking Alpha Premium

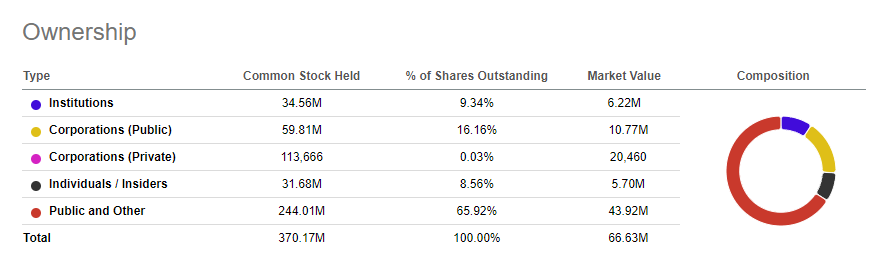

16,16% of shares in the Corporation(public) section are owned by Africa Oil and those shares are going to be deleted based. More on that later.

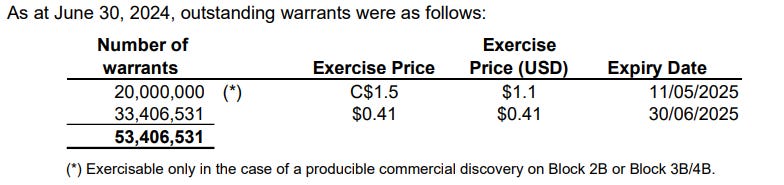

We have some warrants and options out there, but if you look at the exercise prices this stock would have to already be multi-bagger before these become a problem.

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/08/Eco-Atlantic-June-30-2024-FS-FINAL.pdf

It’s an exploration company it has no revenue or cash flow apart from a farm-out deal.

Operating costs are about 1 million USD per quarter.

June 30 balance sheet

Source: https://ceo.ca/content/sedar/EOG-2024-08-29-interim-financial-statementsreport-english-fa84.pdf

Farm-Out provides cash

This balance sheet does not include a farm-out deal they recently completed which provides ECO with 19,8m USD.

Source: https://ceo.ca/@accesswire/eco-atlantic-oil-and-gas-ltd-announces-completion-0160c

They are due to receive 8,3m based on this PR released on August 28th so I assume they have received it by now and will receive 11,5m USD on the spudding of the first exploration well on their block 3B/4B which is expected to take place in the first half of 2025.

With this money based on current operating costs, ECO can avoid raising money for near- and mid-term.

Africa Oil Transaction

Another positive attribute of Eco I mentioned was the decreasing share count. Eco recently announced a great deal with Africa Oil. And by a great deal I mean great for Eco and bad for Africa Oil.

“Agreement to sell a 1% interest in Block 3B/4B South Africa in exchange for cancellation of all of Africa Oil's shares and warrants in Eco (worth C$ 11.5m)”

“Africa Oil currently holds, in aggregate, 54,941,744 Common Shares and 4,864,865 Warrants (collectively, the "Eco Securities"), which, assuming conversion of the Warrants, would equal 16.16% on a diluted basis (c.15% non-diluted) of the total outstanding common shares of Eco worth approximately C$11m.”

This is the deal and when closed it means a 16.16% reduction in the share count of Eco on a diluted basis. The weird thing about this deal and what is great for ECO is that Africa Oil already owns about 1%(0,94% non-diluted and 1,01% diluted basis) of Block 3B/4B through their investment in Eco shares. So they did not gain anything by letting go of their shares for 1% of 3B/4B and only lost exposure to other assets Eco has. So for the existing Eco shareholders, the effect is increased per share ownership of all of Eco’s other assets and the same per share ownership of 3B/4B.

Eco’s management showed some good deal-making skills here.

There is a general lesson here for investors in micro- and small-cap investors. If a larger company like Africa Oil wants to something like for example in this case consolidate its portfolio and get rid of these non-core investments like Eco Atlantic shares there is an opportunity for the smaller company like Eco to get a beneficial deal because Eco cares more about 16,16% of their market cap than Africa Oil cares about a deal that is worth 2% of their market cap. In this case, executing its plan to consolidate its portfolio is more important to Africa Oil than getting a good deal on something only worth 2% of its market cap. So Eco can get a better deal because Africa Oil just wants to see it done and Eco is hard negotiating so It’s more likely that Africa Oil will give in to Eco.

I have seen similar dynamics for example when larger companies are divesting from oil and gas fields in a particular region. Smaller companies that are willing to invest in those assets can get a great deal. Like Valeura got with a Mubadala acquisition and Tenaz Energy with NAM offshore acquisition from Shell and Exxon, Both deals have multiplied the stock price of Valeura and Tenaz.

A bit of a detour there. This deal with Africa Oil is a clear net positive for Eco. It’s not a huge catalyst, but it will be a positive news event when it closes. If you happen to be the CEO of Africa Oil reading this post don’t back out. It’s a good deal for you. I was joking the whole time.

So far I have been building the base for the thesis. We are starting off with cash coming in, the share count going down, the warrants and options not until the stock price goes up a lot. Low risks from the financial side.

Eco is about to drill on one block in the first half of 2025, attempting to find a partner to drill another block in 2025, trying to farm out multiple blocks, and upgrading one block. They call areas where they are looking for oil and gas “blocks”. That’s kind of an industry term.

STOP EVERYTHING! The new shorter and better SA Premium Ad is here!

Get a 7-day free trial and 30$ discount on your first year of Seeking Alpha Premium and support AlmostMongolian with my Affiliate link: https://www.seekingalpha.link/3N9WBS8/2QZRGT/

Where are Eco’s blocks?

Hottest oil exploration spots in the world

Eco has their assets in Guyana, Namibia, and South Africa. Let’s look at these places in general before going to the specific assets.

Guyana

Guyana is the fastest-growing oil producer in the world.

Source: https://www.statista.com/statistics/1260886/crude-oil-production-guyana/

Guyana’s oil boom is located on the Stabroek block with an estimated resource of about 11 billion barrels.

Source: https://energycapitalpower.com/eco-atlantic-farms-into-orange-basin-block-1-offshore-south-africa/

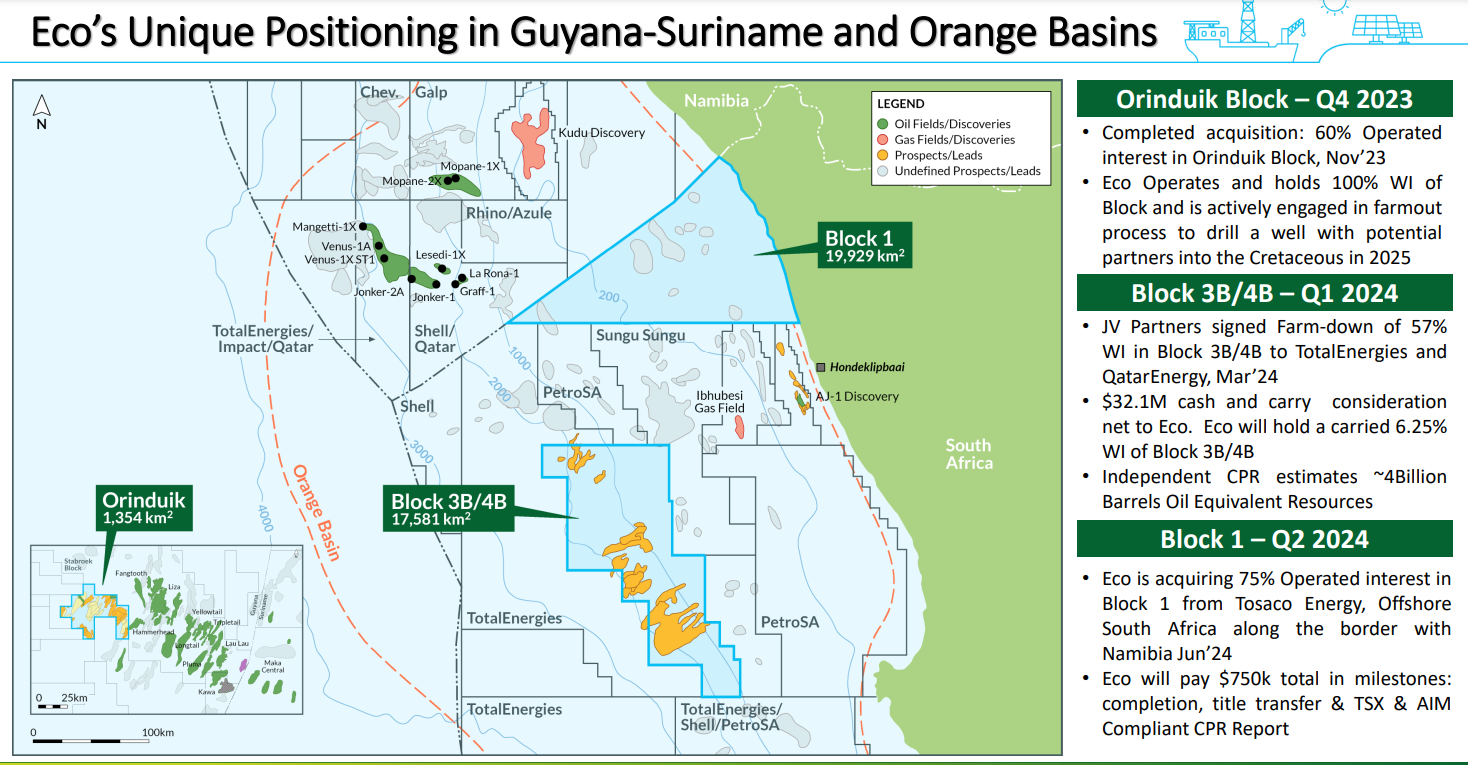

Eco has 100% interest in the Orinduik block next to the Stabroek block with 2 oil discoveries. I will go into more detail about this block in the asset deep dive section.

Also, Look at how rectangular these areas are. Kind of blocky. I guess that’s why they call them blocks. Orinduik Rectangular Area just doesn’t have the same ring to it.

Orange Basin, Namibia, and South Africa

Orange Basin located in Namibia and South Africa is the hottest oil exploration spot in the world. You can see the amount of activity in the below picture. It’s a bit outdated. It’s even busier now.

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/07/ECO_Investor-Presentation-JUL-FOR-WEB.pdf

The Mopane discovery is estimated to hold +10 billion barrels.

According to NAMCOR(National Petroleum Corporation of Namibia) Venus, Graff, and Jonker discoveries are estimated to hold up to 11 billion barrels.

Source: A user named Manudonuts posted this on ceo.ca I don’t know where it is from originally.

About 140 million years ago South America broke up from Africa. This has caused oil and gas to be here. No need to explain that further. But you can see by comparing 2 pictures above how the Post-Rift isochore map shows quite well where the oil companies are exploring.

New wells drilled in Orange Basin have hit oil around 80% of the time which is an amazing success rate.

Source: https://knowledge.energyinst.org/search/record?id=115186

Here are the average success rates for new wells. As you can see the 80% success rate is amazing for offshore and onshore oil wells compared to the averages.

Another exciting thing is how unexplored this basin still is. Because more explored areas tend to have higher success rates and less explored areas tend to have lower success rates. This makes the success rate of Orange Basin even more impressive.

The exploration boom started very recently. It was set off in 2022 by the large Venus and Graff discoveries.

The resource estimates vary from different sources and are changing as more data comes in. Also, the estimates of how much is recoverable economically are changing.

But what is clear is that there is a lot of oil here and the exploration has just started. Orange Basin (Namibia and South Africa combined) could easily be in the top 10 in the world in terms of reserves after a few years of Exploration. And Eco is positioned there with a small market cap.

Source: https://en.wikipedia.org/wiki/List_of_countries_by_proven_oil_reserves

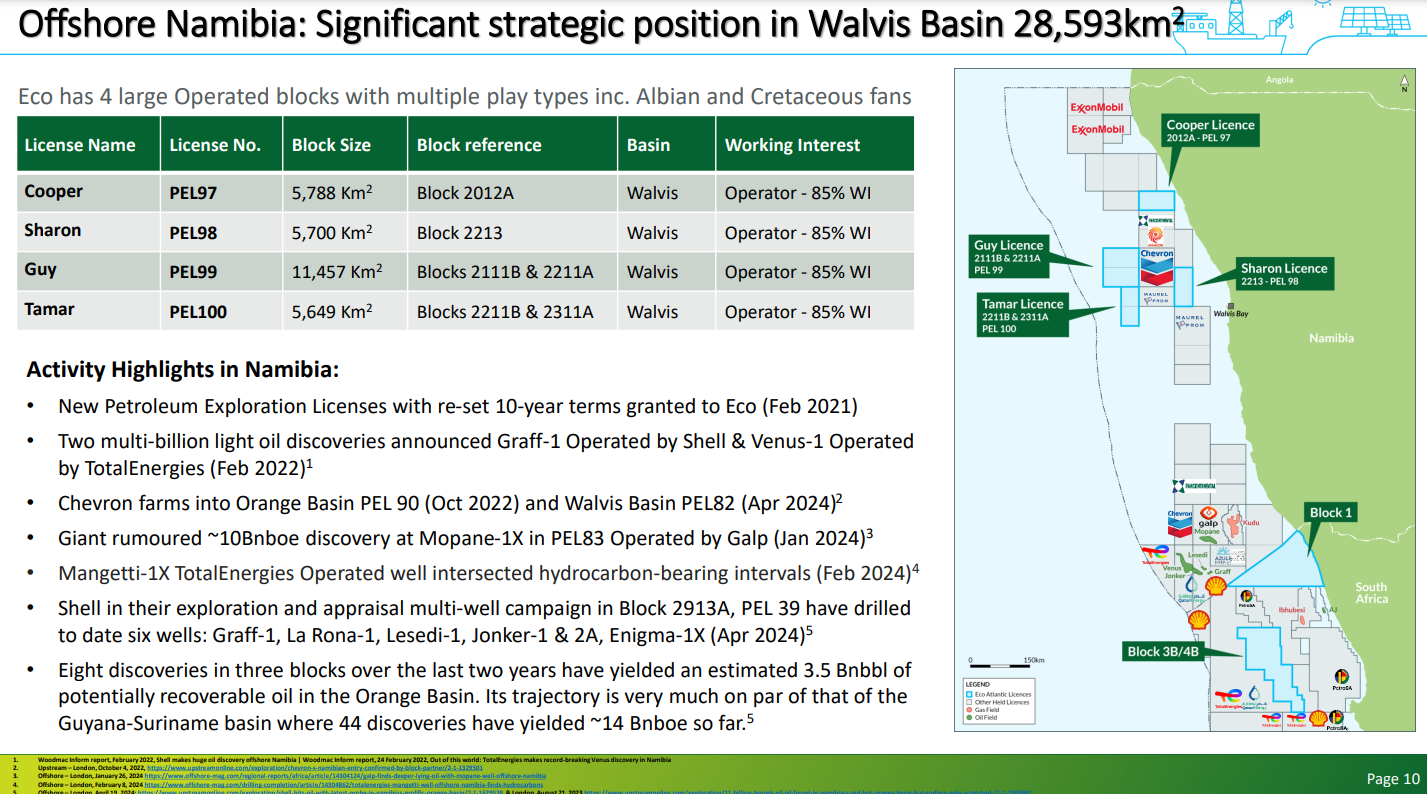

Eco also has 4 blocks on Walvis Basin in Namibia. More about that later.

Asset Deep dive

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/07/ECO_Investor-Presentation-JUL-FOR-WEB.pdf

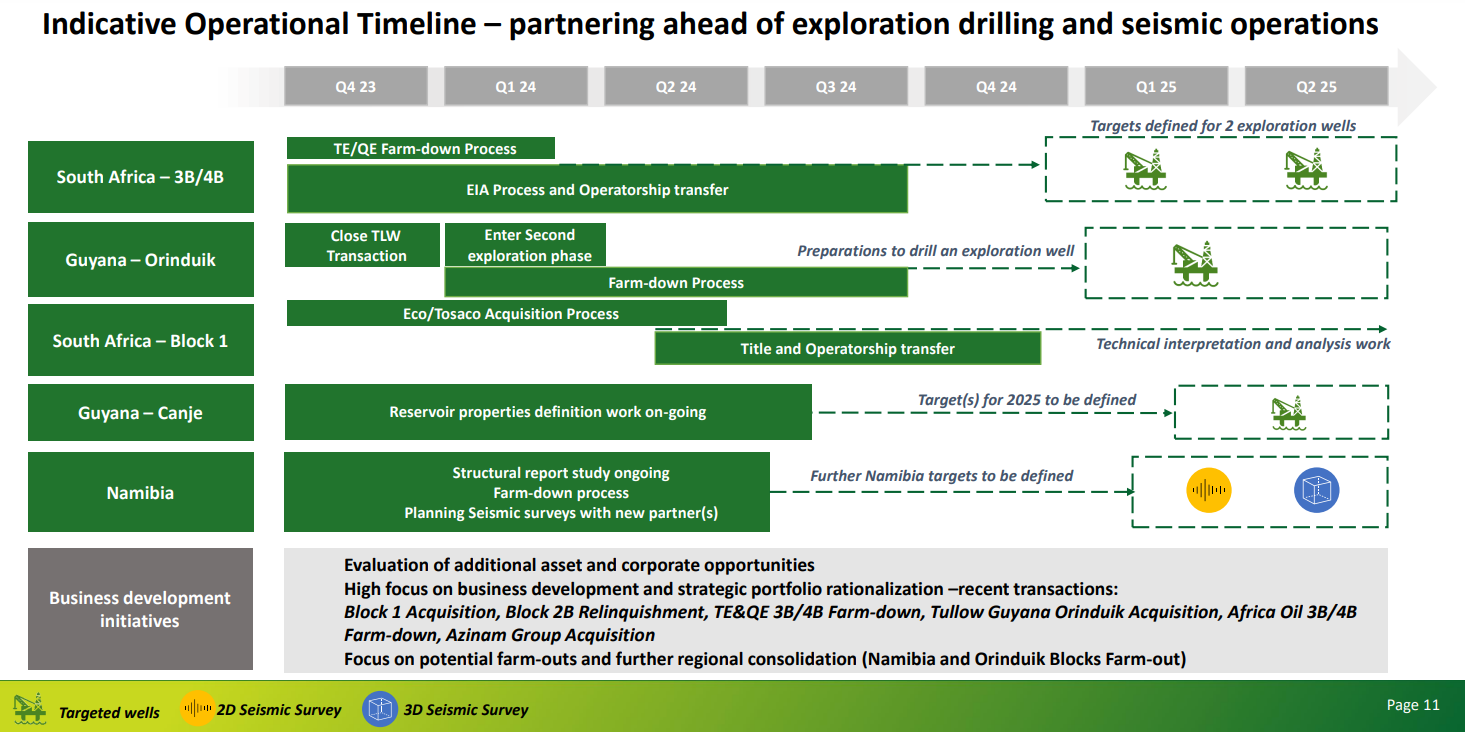

This is the timeline set up by Eco. Of course, they are late already on the Farm down of Orinduik which was supposed to be done by the end of q3 according to this slide, but when it comes to investing in stocks I think it’s better to always assume your companies are going to be late on everything. Never assume a timeline given by the company will hold.

These terms and concepts are important to understand for the next section↓

Working interest = Right to develop and operate a leased piece of land for the production of oil and gas

Operated interest=Basically the same as working interest, but when a company is the operator

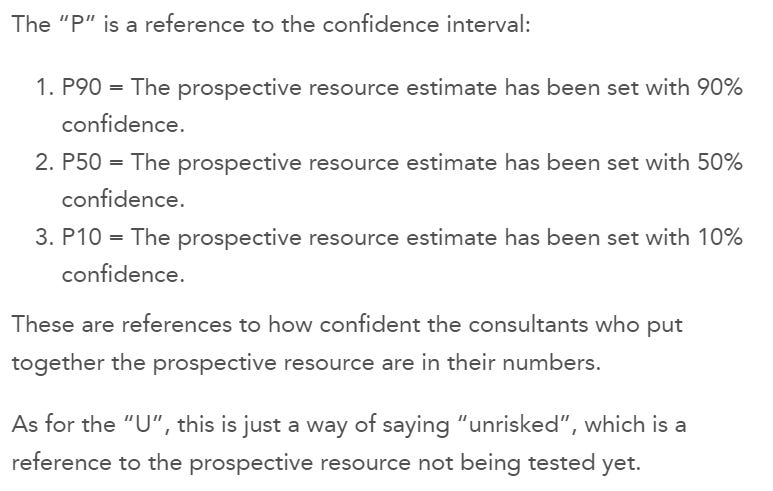

Prospective resource. P90, P50, P10

Source: https://nextinvestors.com/learn-to-invest/oil-gas/what-are-oil-and-gas-resources/

Farm-in = A company (farmee) acquires an interest in an oil or gas project or license from another company (farmor) that already holds the license.

Farm-out=Opposite. Farmor decreases their stake to the farmee. The farmee is usually a larger company that has more capital and the ability to advance the project. The farmor could be left with a carried interest that allows it to avoid development costs while retaining exposure.

And farm-down is basically the same as farm-out.

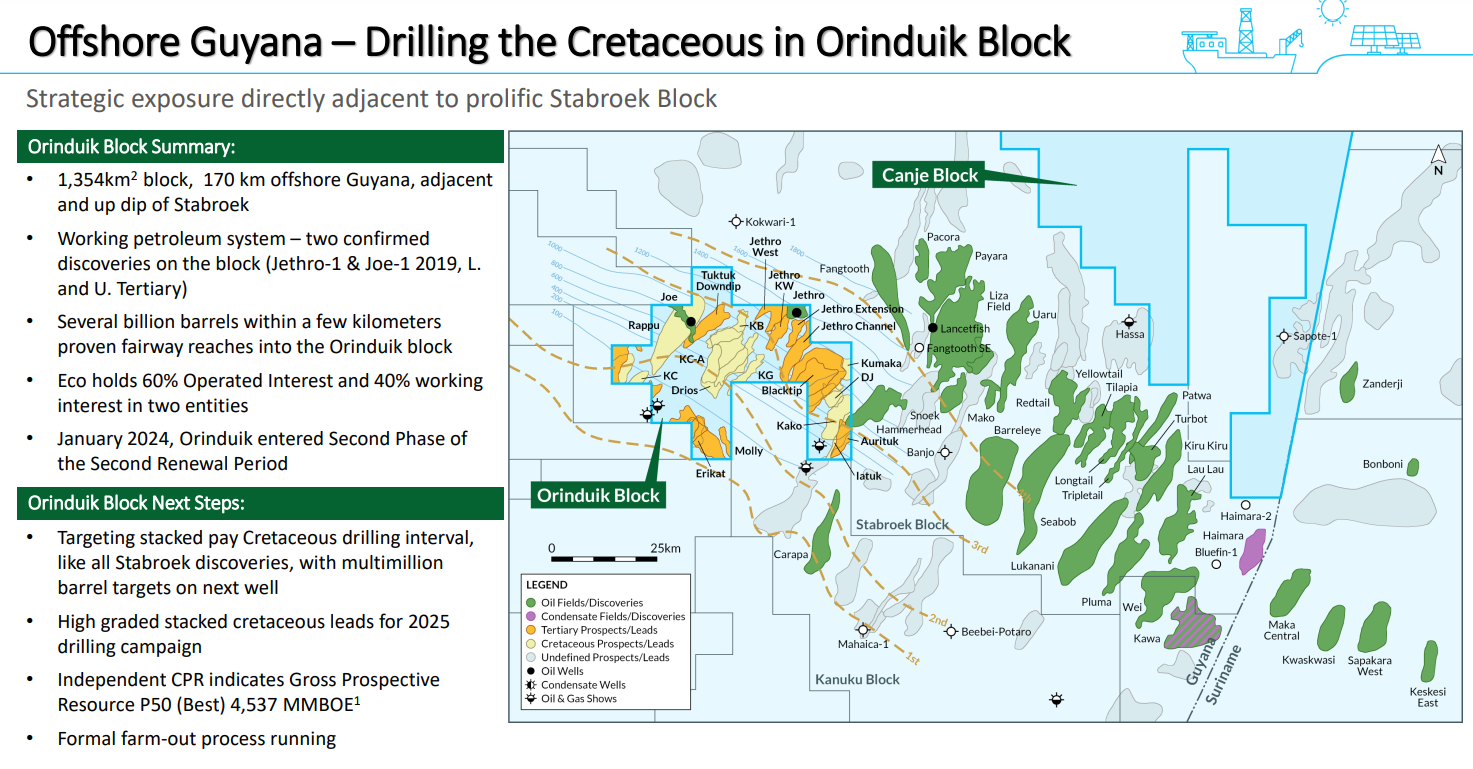

Guyana, Orinduik Block, 100% WI, Operator

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/07/ECO_Investor-Presentation-JUL-FOR-WEB.pdf

Eco also has 1,3% WI on the Canje block shown in the above picture, but because of the low WI and not many results, It’s too unimportant to mention again.

This has been Eco’s main asset for a long time and they have gradually acquired the whole thing.

Based on the first look, Orinduik seems amazing: Right next to Stabroek, 2 oil discoveries, and tons of prospects, and the Hammerhead discovery from Stabroek reaches Orinduik block, and there is a 4,537 MMBOE P50 prospective resource based on independent valuation.

And a small company like Eco has 100% interest. But. Of course, there is a catch.

You saw that chart of the stock price earlier there was a big spike and the market cap at the top in 2019 was more than 400m CAD after it fell. This whole spike and fall was based on expectations and results of drilling on this asset although the crash in oil prices in 2020 made the share price drop even lower.

As you can see from the picture above they found oil from this Block, but it was heavy and high in sulfur and at the time it wasn’t seen as attractive enough to develop.

A quick history of this Block

2019 They did 2 exploration wells and found a lot of oil, but it was heavy oil

2020 Resource report completed

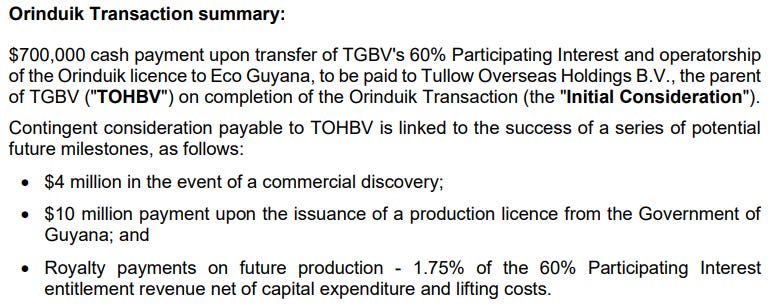

2023 Eco Acquires 60% WI from Tullow Oil and Assumes Operatorship

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/11/EOG-MDA-September-30-2024.pdf

2024 January Total and Qatar Energy give up their 25% WI to Eco

So now Eco has 100%. They are the last man standing on this block that was once hyped and now forgotten. Eco is still a believer. Let’s what we have here.

This is from the 2020 Orinduik Report CPR Report link

Source: https://www.ecooilandgas.com/wp-content/uploads/2020/02/AIM2020CP-ECO-Orinduik-report-Feb2020.pdf

This analysis was done after the 2 heavy oil finds. It’s quite a large resource.

Quote from Eco’s website

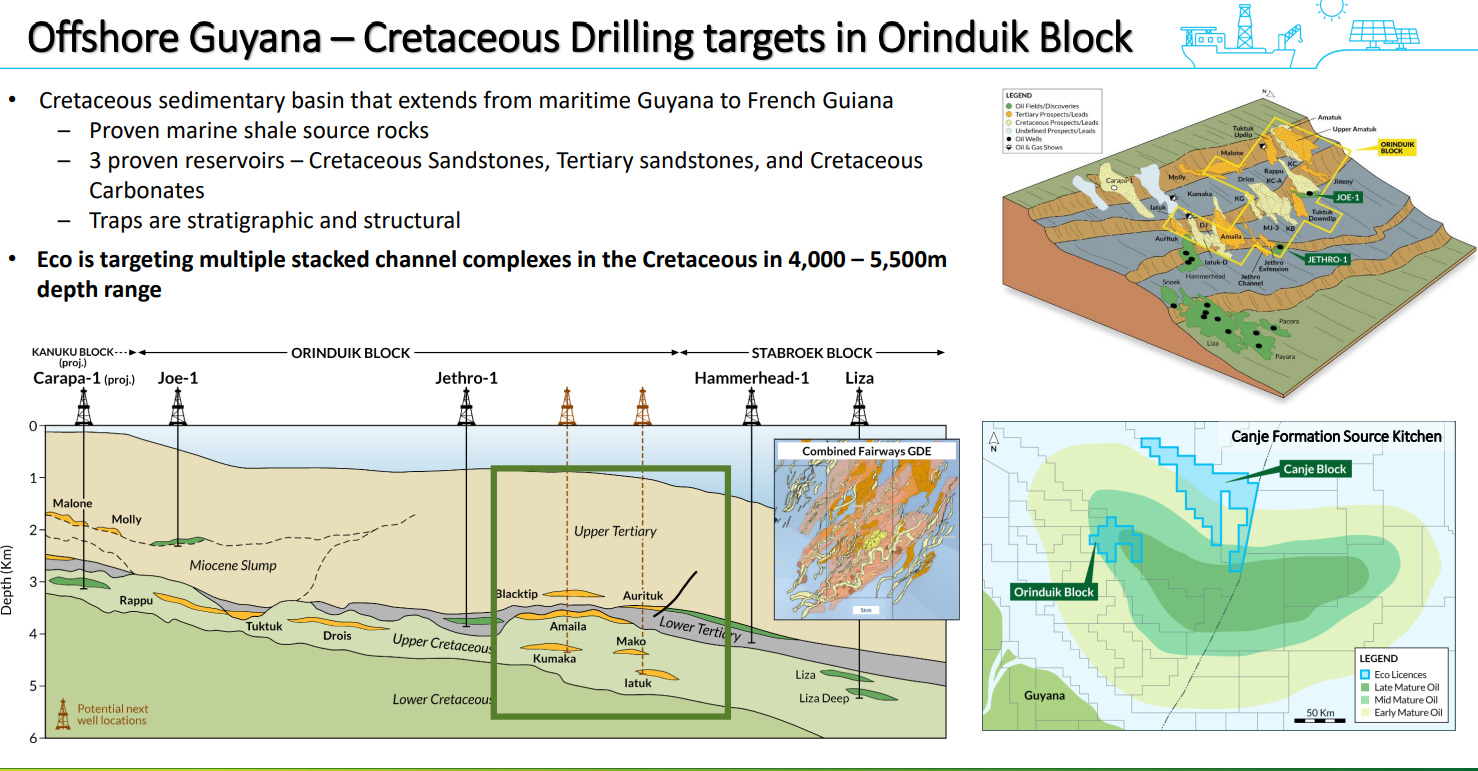

The Orinduik Block is situated in shallow water (70 – 1,400m), 170 km offshore Guyana and is located 11km up-dip from ExxonMobil’s Liza discovery and 6km up-dip from Hammerhead discovery on the Stabroek Block. In 2019 two oil discoveries at Jethro-1 and Joe-1 were made, both wells encountered high quality reservoirs containing mobile heavy crude.

Eco is now working on the overall prospect inventory in particular the cretaceous horizon and developing plans to unlock value from this acreage through additional exploration wells.

The Liza discovery went through a big development and has now achieved peak rates of 400,000 barrels per day. Huge.

Another discovery they mentioned was Hammerhead and this is more important to Eco because Hammerhead discovery reaches Orinduik block and it’s in development.

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/07/ECO_Investor-Presentation-JUL-FOR-WEB.pdf

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/07/ECO_Investor-Presentation-JUL-FOR-WEB.pdf

The above picture shows the potential well locations and you can see how the Hammerhead reaches Orinduik from this as well. The CEO said in July that

“next drill campaign during 2025 probably the Aurituk prospect which is a stack Prospect of Mako and Latuk”

So they are going to try to get 3 prospects that are stacked on top of each other that also connects to the Hammerhead.

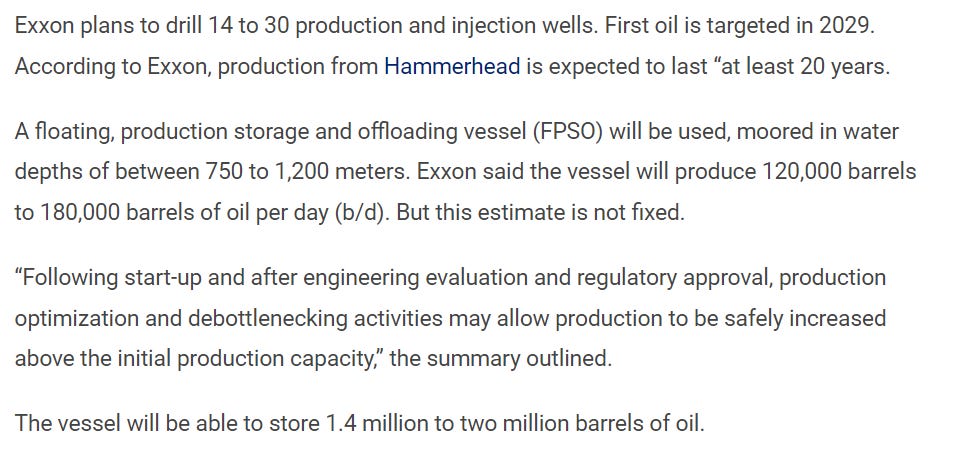

More about Hammerhead. Hammerhead is Exxon’s discovery and currently, it’s in development and it’s a big development.

Source: https://brazilenergyinsight.com/2024/07/18/hammerhead-will-be-stand-alone-development-exxon-project-summary/

This is significant for Eco. Orinduik is all owned by Eco which has no money to develop it. It has already a significant heavy oil resource and has a slice of the Hammerhead field. Exxon is the primary oil producer in Guyana. It seems clear that Exxon would be the natural partner for Eco’s farm out.

The fact that Exxon is going forward with Hammerhead is also significant because Hammerhead is a heavy oil development. And the original reason Eco got hammered was because they found heavy oil.

Also, the CPR report on Orinduik says that the oil from Hammerhead is similar to what was found in Orinduik.

“Oil and associated gas in the Tertiary have been encountered by Tullow Oil, the operator, on the Orinduik Block based on the Jethro and Joe discoveries on Orinduik Block. The oil from these discoveries is reported by the operator to be similar to the ExxonMobil Hammerhead oil, in the 12o to 15o API range although a Final PVT analysis has not been provided by the operator at the time of this report. In addition, the Repsol Carapa 1 well located less than 40 kilometers southeast of the Hammerhead area and 55 kilometers south of the Jethro well has discovered 27o API oil in the Cretaceous.”

So Exxon is developing Hammerhead which is similar to Eco’s finds and reaches into Orinduik and Eco has even larger resource than Hammerhead based on estimates from Joe and Jetthro discoveries. Paints an interesting picture.

Eco also has an obligation to drill a well by January 2026. You might have wondered why for example Total and Qatar just walked away from their 25% for nothing. It’s because the blocks are leased from the government and there are obligations to develop those areas because the government wants the blocks to be developed for economic benefits. So Eco is going to need to find a partner as drilling the well by themselves would cost too much for them.

This also makes Eco more interesting now. Because there is finally an urgency to move this block forward.

This is a Quote from the CEO during a presentation in July.

“we have an obligation to drill well by to spud well by January 2026 so basically during 2025 and we have identified the Target that we want to drill and we are currently actively in a process of bringing in a partner to help us drill the well and most probably will not drill a well 100% we will not drill well 100% on our sole risk um so we will bring in a partner to drill in with us a part of the cretaceous light oil Target that we have that we are targeting around 800 million Barrels in total and we also have as a bonus for farming we have the two heavy oil discoveries that are still there still under our names mainly the Jettro one which has around 1 billion barrels of oil in place again heavy but still oil and there's a lot of demand for heavy oil especially these days when Venezuela is sanctioned and we have another small bonus which is the extension of hammerhead um which is the seventh project development project of Exxon in the Stabroek block that part of it stretches into our block and there's a clear unitization legalization in Guyana and when the time comes it's very clear under the petroleum agreements it's very clear under the legislation but again this is Exxon just announced just few weeks ago that they're going to develop it it's very good news for us in any case because first of all it's a heavy oil development and second as I said a bit of it or a piece of it is stretches into our block um and I believe it will be a subject to further discussions with the government and with the stakeholders going forward”

A lot of that I already went through, but this was a significant part “light oil Target that we have that we are targeting around 800 million Barrels in total” If they can hit even 100 million barrels of light oil I would assume the stock will fly. The difference in commercialism is so big between light and heavy. Allthough there are other attributes as well that make a difference in the economic potential of an oil field.

Eco still thinks what they have now is commercial and I think the Hammerhead development gives some validity to that. If they can get the farm out done and drill and find light oil it would be huge.

I think this is the highest potential asset Eco has. It’s not the most imminent catalyst which is the next asset I will talk about, but in terms of potential if they can find a dedicated major company to develop it the upside is massive. This asset has been on the shelf with no drilling and partners getting out for so long that I don’t think the market is giving Eco a lot of value for it compared to what it can be worth if things line up.

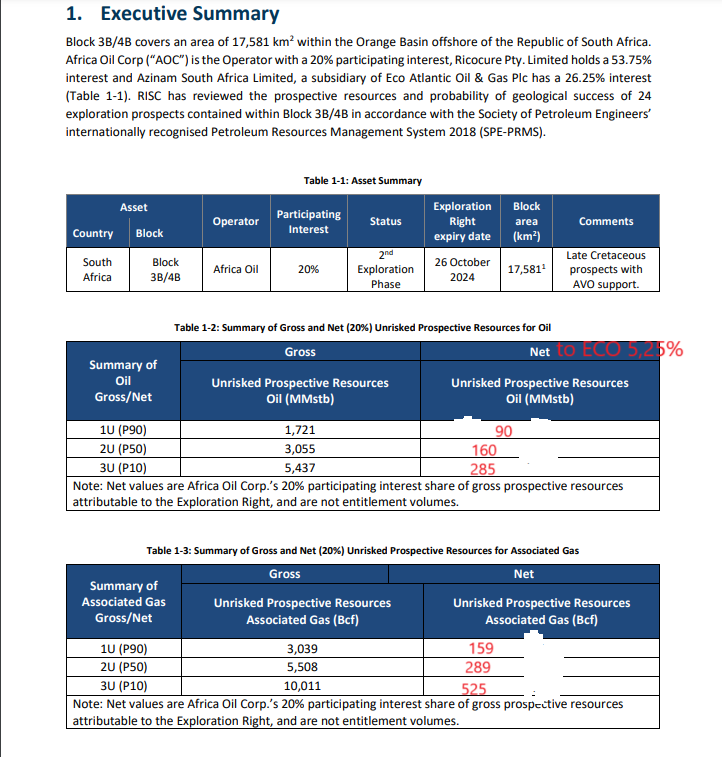

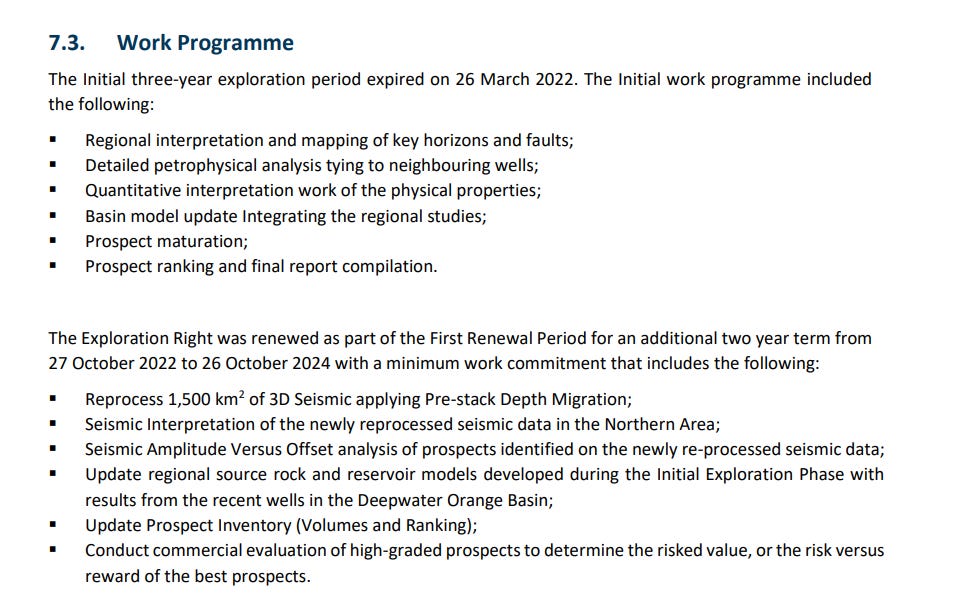

3B/4B, South Africa, Orange Basin, 5,25% WI post-Africa oil transaction

3B/4B has already been mentioned twice in the context of the farm out that provides Eco with cash and the share count reduction deal with Africa Oil.

Eco owns 6,25% of 3B/4B now and 5,25% post-Africa oil deal which is supposed to close in q4, but because of the reduction in share count effectively the 3B/4B per share ratio does not change.

This is the second part of the 3B/4B deal not covered earlier.

Source: https://ceo.ca/@accesswire/eco-atlantic-oil-and-gas-ltd-announces-block-3b4b

On top of the cash Eco does not have to pay for their share of the drilling costs for the first 2 wells. These drilling costs are repayable from production so that would be very far away (probably 2028-2032) if this block ever goes into production.

The cash from this deal is in itself great, but the real impact will be the drilling. So what do we know about the property and when will the drilling happen?

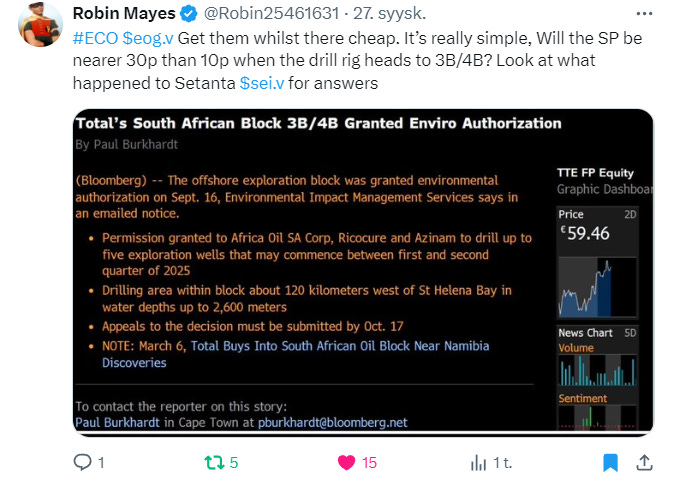

Source: X, Robin Mayes

This was spotted by Robin Mayes from X. We have heard before that the drilling will likely be taking place in the first half of 2025 and here we see a higher confirmation as they have been granted an environmental authorization to drill 5 exploration wells and for the drilling to commence between first and second quarter of 2025.

Note that they have permission to do 5 wells. It’s not sure whether they actually end up doing 5 wells. I think a lot will depend on the success of the first and second wells.

So if those wells are successful Eco stock price will be higher and they will drill more wells. This means Eco will have to make another deal or pay their share of the drilling.

Robin Mayes also mentions Sintana (He wrote Setanta. A mistake, but that’s okay)

Source: Google

Sintana had a similar market cap to Eco and now has a 413,86m market cap. Their biggest positive news was the huge Mopane Light Oil Discovery. The Mopane complex is now estimated to have 10b barrels and Sintana has 4.9% fully carried interest on it.

This is just a good example of what can happen when you are positioned in the right place and have a low market cap. If 3B/4B for example gets similar results when it drills 3B/4B early next year it makes sense Eco would have a similar move.

So what do we know so far about 3B/4B?

Valuations so far

Last time Eco increased their position Eco bought 6,25% WI for 10m USD valuing the Block at 160m USD.

The farm-out announced in March 2024 that closed in August values the Block at 428m USD which would put 5,25%(post-aoi deal) at 22,47M USD valuation compared to post aoi market cap of 40,46m USD.

The AOI deal values the block at 1,15 billion at the time of the deal valuing ECO’s post-aoi deal position at 60,375million USD. But as I went over earlier that deal was questionable on AOI’s part so I take that valuation with the Grain of salt.

The trend emerging is that we are seeing the valuations moving higher over time for 3B/4B.

We can see that the players in the market are already valuing this block highly before any drilling and there is a reason for that.

Source:https://africaoilcorp.com/wp-content/uploads/2024/06/risc_-_africa_oil_corp_prospective_resource_report-_blo.pdf

There is a significant Prospective resource based on a report by RISC Advisory. Here is a link to the whole report: https://africaoilcorp.com/wp-content/uploads/2024/06/risc_-_africa_oil_corp_prospective_resource_report-_blo.pdf

This report is huge and very technical. I’ll go over some of the important and easily understandable parts next.

Source: https://africaoilcorp.com/wp-content/uploads/2024/06/risc_-_africa_oil_corp_prospective_resource_report-_blo.pdf

This report was made on behalf of Africa oil which means the original net was based on 20% of Africa Oil’s position at the time. I edited the picture to include the post-aoi deal 5,25% for ECO Atlantic as the net number. So you can see ECO Atlantic’s prospective resource.

Even if they prove the low case of 90% confidence it’s still a decent amount of oil and gas for the market cap of ECO. The 50% confidence resource should be bullish. and if they prove the 10% confidence resource that would be very bullish.

Based on the valuations of the company not a lot of success is priced in meaning even the P90 resource being proven could end up being bullish, but it’s hard to say with these small-cap stocks how they will react.

Source:Source: https://africaoilcorp.com/wp-content/uploads/2024/06/risc_-_africa_oil_corp_prospective_resource_report-_blo.pdf

This is what they did to come to their conclusions.

Here are some quotes from the report.

“A large opportunity set of exploration prospects has been identified in deepwater Block 3B/4B and the ability to stack targets in early wells on the license combined with an extensive data acquisition campaign will help to significantly understand the prospectivity and presents opportunities for ‘cluster’ developments to optimize value from any possible developments.”

“Shell Exploration & Production’s (“Shell”) recent Graff well discovery and TotalEnergies Venus well discovery in deep water Namibia contain seismic amplitude anomalies and are on trend with AOC’s South African 3B/4B license. The discoveries prove the existence of a working petroleum system for light oil, gas condensate and gas in the geological play fairway. The proven reservoirs in Graff and Venus discoveries are similar to Cretaceous reservoirs and geological plays that would be targeted in the AOC 3B/4B Exploration Right.”

As I went over earlier Venus and Graff were huge oil discoveries in the Orange Basin north of 3B/4B.

Source: https://africaoilcorp.com/wp-content/uploads/2024/06/townhall_presentation_april_2024_website_version.pdf

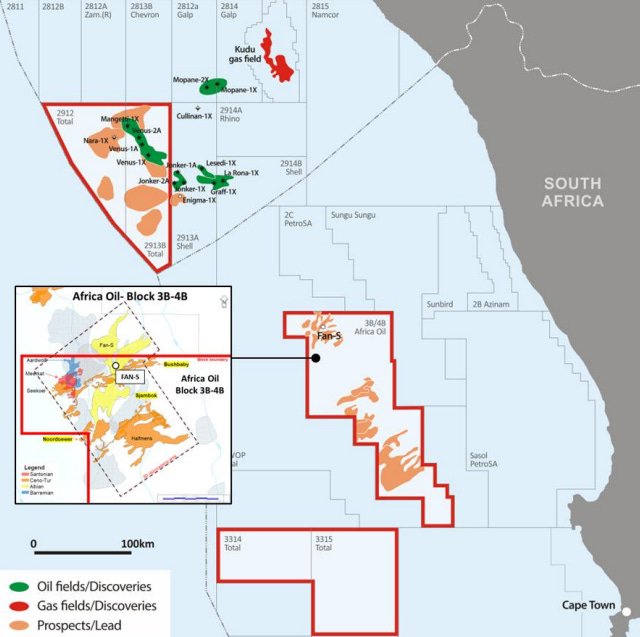

Africa Oil's presentation highlights the FAN-S prospect. I would guess this would be one of the first drills next year. This is what the report says about it.

“Fans SA, SB, and SC are Albian age basin floor turbidite fans that are of similar age, stratigraphic sequence, and depositional environment as the Lower Cretaceous age sandstones of the Venus discovery in Namibia.”

Venus was the world’s largest new oil discovery in 2022.

“Fan SA is at-present the largest prospect in the inventory. Detailed mapping of its internal structure indicated that it is comprised of at least three interfingering or shingle-like lobes. A prospect location has been selected within Fan SA that would test a structurally high AVO-supported position within the fan that would also be an advantageous position to test Bush Baby.”

Bush Baby is another prospect close to FAN-S.

I went over the amazing success rate for new wells in Orange Basin and 3B/4B has very strong prospects based on independent evaluation and high valuation by the market and the highest valuation by Africa Oil which is likely the most experienced party involved with 3B/4B.

Something to note is that if you like 3B/4B, but are hesitant because you don’t like the other assets of ECO or don’t want to invest in pure exploration companies. In that case, there is Africa Oil which is a safer way to play this block. Africa Oil is a producer and is bigger. Africa Oil will own 18% of 3B/4B post transaction with Eco, but Eco still has more torque than 3B/4B because Africa Oil has a much higher market cap.

There is no public company with more torque to 3B/4B than Eco.

So Eco will have 5,25% and after the 2 drills their free carry runs out and they would have to pay for their share of drilling expenses. I see 2 likely scenarios for the future:

The drills are successful and ECO will make another deal ideally a full carry to production or something like this and they will have to relinquish more WI to do this. Or maybe they just sell their stake if they get a high enough price.

The drills are unsuccessful and 3B/4B goes into an uncertain situation. Will the big WI holders like Total and QatarEnergy want to continue trying or leave the investment? Maybe Eco will leave as well or they will keep trying.

I think scenario 1 is the likely one because of how all the things I have gone over the high success rates in Orange Basin, The high valuation of the block by big players, and a huge amount of research that has already been done on the block resulting in many strong prospects.

Block 1, South Africa, Orange Basin, 75% Working Interest, Operator

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/07/ECO_Investor-Presentation-JUL-FOR-WEB.pdf

This is the newest acquisition from Eco Atlantic. It’s part of South Africa’s side of the same Orange Basin that includes the massive Venus, Graph, and Mopane discoveries in Namibia’s side of the basin.

They will pay 750k USD for 75% WI and they are the operator. I’d say that is a pretty low price considering the potential here with the close proximity to these huge oil finds.

These are the terms of the deal in more detail

“Terms of the 75% WI Farm-in Acquisition are as follows: US$150k payable upon signing, US$225k payable upon issuance of Section 11 (Government title transfer) and US$375k payable upon a TSX-V/AIM compliant Resource Report to be commissioned by Eco. The Company will carry the remaining 25% Interest through the Budget and Work Program for the first three years up to an agreed sum of US$2.3 million of a total work program.”

750k price with 2,3m work commitment.

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/07/ECO_Investor-Presentation-JUL-FOR-WEB.pdf

The current Plan with this block is basically to upgrade it and then I assume wait for a bigger company to get interested. Doing the Resource Report which is kind of like the 3B/4B report I showed earlier. Doing other studies and analysis work.

This what the CEO said about it during a presentation in july.

“I think that by the end of the year or even before we will become the operator official operator then we will we will start our technical evaluation and we'll probably attract additional big companies to come in and explore with us as I said 2D and 3D are there existing we just need to analyze to select targets and move forward on the one hand there's no commitment not to shoot seismic and not to drill on the other hand we think we can Fast Track the the entire process”

They are saying talking about fast-tracking it. Because it’s Orange Basin I will not completely disregard that possibility, but I’m not going into this investment expecting a fast track on Block 1.

"The block has significant 2D and 3D seismic data already completed and no additional seismic acquisition or drilling of wells is planned in the three-year carried period. During this period, Eco will complete the interpretation and analysis required for its planned Work Program with its in-house exploration team. The Farm-in is subject, inter alia, to normal Governmental approvals and no field activity is currently planned that requires environmental permitting.”

This is what Eco said about this block. This is from when they bought it. Eco the Block.

“There are inboard gas discoveries on the block, Kudu to the North, and multiple discoveries in the Ibhubesi field to the South. With the reach of the block some 250 km out into the Atlantic, this puts the West end of the Block into highly prospective opportunities for oil being just South and on trend with Shell’s Graff discovery and Galp’s Mopane discoveries, and North of our 3B/4B Block oil targets recently farmed out to TotalEnergies and QatarEnergy.”

Inboard gas discoveries are close to shore gas discoveries.

Also as the nearby areas are getting more and more discoveries and as those discoveries get more defined and as more companies are trying to enter Orange Basin Block 1 should be getting an increasing amount of interest as time goes on. So I think Block 1 will basically passively increase in value at the same time as Eco is working to upgrade it.

Block 1 is not a near-term catalyst like 3B/4B, but for the long term, it’s really good to have it on the portfolio. And maybe they can fast-track it.

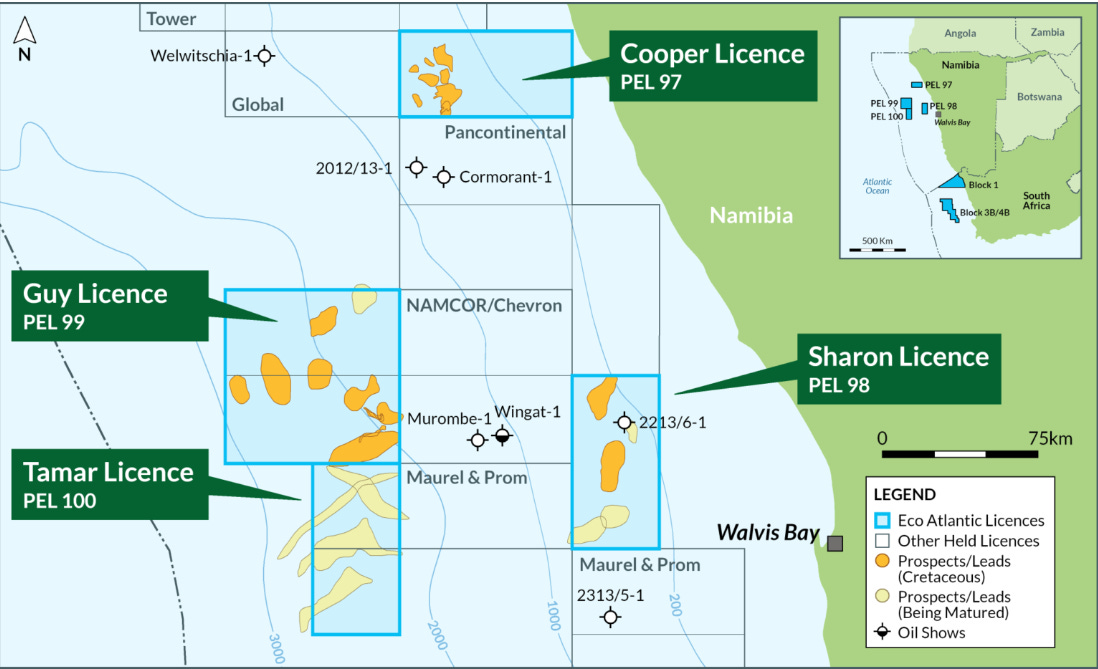

Namibia, Walvis Basin, 4 BLocks, 85% WI+operator each

Source: https://wp-ecooilandgas-2020.s3.eu-west-2.amazonaws.com/media/2024/07/ECO_Investor-Presentation-JUL-FOR-WEB.pdf

Walvis Basin is Namibia’s less explored basin north of Orange Basin. Eco is currently the biggest player in the Walvis basin in terms of WI and is trying to do a farm out.

“· A multi-block farm out process remains underway for all or part of Eco's four offshore Petroleum Exploration Licences ("PEL"): 97, 98, 99, and 100. Eco holds Operatorship and an 85% Working Interest in each PEL representing a combined area of 28,593 km2 in the Walvis Basin.”

But so far Walvis has had only a small amount of exploration with mixed results.

Source: https://www.ecooilandgas.com/projects/namibia/

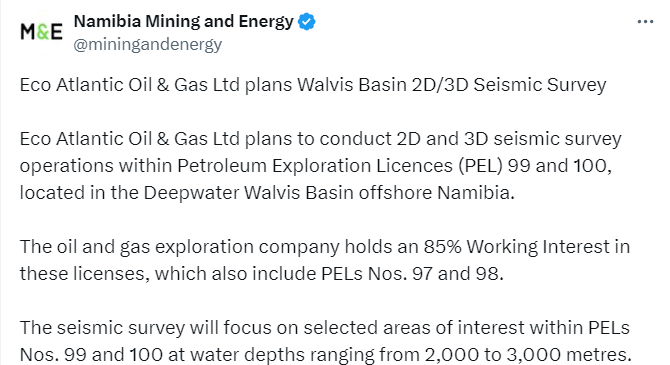

Eco’s blocks have multiple prospects based on 2D and 3D studies. Namibia Mining and Energy just reported that Eco plans to do more 2D and 3D.

Source: https://x.com/miningandenergy/status/1842880519387943280

When it comes to actual oil finds in the basin it’s underwhelming.

There was one well in 2013 Wingat-1 that “indicated the presence of oil”, but not in commercial quantities.

Source:https://www.galp.com/corp/en/investors/publications-and-announcements/investor-announcements/investor-announcement/id/397/wingat-1-exploration-well-results

Although this find did not indicate commercial quantities of oil this is what a company operating in the area Global Petroleum says about it.

“Wingat-1 well as being the most significant of the wells drilled in the Walvis Basin since liquid hydrocarbons were recovered from the Aptian interval, thus establishing for the first time that a source rock has charged oil into a trap in the Walvis Basin.

Furthermore, the company has mapped 3D and 2D seismic across the basin and this license, confirming that the source rock is present and can charge oil into the significant portfolio of prospects and leads.”

Quote from this article: https://www.offshore-energy.biz/talks-underway-with-potential-partner-to-sign-up-for-exploitation-of-oil-prospect-offshore-namibia/

It doesn’t seem very exciting at the moment, but considering how long ago and how limited the exploration was I don’t think we can throw Walvis in the trash quite yet.

Also, I think we are starting to see a spillover from the oil boom in Orange Basin causing a positive effect on Walvis Basin assets. We have already seen some increased activity for example Chevron entered the Walvis basin last April.

Source: https://www.offshore-mag.com/regional-reports/africa/article/55032808/chevron-farms-into-oil-proven-walvis-bay-license-offshore-namibia

This block is surrounded by Eco’s blocks from the west(PEL 99), from the east(PEL98), and from the southwest (PEL 100). There was also another news release about a potential farm-out last august. And this was concerning a block that is next to Eco’s PEL97 block.

Source: https://www.offshore-energy.biz/talks-underway-with-potential-partner-to-sign-up-for-exploitation-of-oil-prospect-offshore-namibia/

These developments next to Eco’s blocks bode well for Eco’s farm-out process. And if they can get it done it will be a positive event that I assume will have a positive impact on the stock price despite this being one of their less-valued assets currently.

I took 2 quotes from a presentation in July where the CEO talked about the Walvis basin.

“without entering into too many details I can tell you that since Chevron farmed into the Basin and there's a rush into Namibia regardless orange Basin is fully taken um we have many many companies interested knocking on our doors looking at our Namibian acreage and considering it farming to finalize”

Rush into Namibia. Orange Basin taken. That’s the spillover effect on Walvis.

“in Namibia other than doing some structural report on the entire basing at the moment for the ministry and for ourselves obviously and we are in an active Farm out mode we speak with a lot of companies or many companies at the moment there's a keen interest for many big oil companies to come into Namibia and explore and I hope and believe that by the end of the year, we will be able to announce a farming deal in our Namibian blocks”

Currently, these assets are just potential, but considering the very large position Eco has here it could be a very asymmetric opportunity if big finds are made and the spillover effect from the Orange basin oil boom is real meaning it’s easy to see these assets gaining value just based on that.

Closing comments

I invest based on Risk/reward calculation and what is attractive about Eco is that I can go over different scenarios in my head of how it could play out and in most of them I win from the current valuation. That is a very important part because if the stock would double that would completely change the risk/reward.

Everything goes great 3B/4B finds more oil than expected, Guyana gets a partner with great drill results, Walvis basin farms out, Orange Basin keeps getting busier block 1 gets interest=That could be a 10x

3B/4B is disappointing, but Orinduik gets a partner with good drilling results, Walvis doesn’t get a farm out, Block 1 just exists = stock price +50-200% possibly

Same thing as 2. but 3B/4B has great results, but they can’t find a partner for Orinduik=+50-200%

3B/4B results disappointing, can’t find a partner for Gyuana, Can’t Farmout Walvis, Block 1 just exists= Stock price probably goes down -25-50% from here

The reason I think the downside will be limited even in the bearish scenario 4 is their cash position will still be solid with the 3B/4B farmout money and their portfolio will still have the Orinduik block that does have a big resource that does reach into HAmmerhead and their overall positioning in Namibia and Soth Africa. I don’t think 3B/4B will still be worthless if the first drills are unsuccessful.

And the stock only needs one of their 2 big assets 3B/4B or Orinduik to be successful for decent gains from here and in case both are successful there is massive upside potential. Their 2 earlier stage assets Walvis and Block 1 will in my opinion gain value over time just from their proximity to the Orange Basin oil boom and offer potential upside in the future.

Do you see the risk/reward now? Do you see?

Then there is the Africa Oil deal which will be good, Oil prices will have an effect, but that is always unpredictable, and jurisdictions are okay. Guyana has been a great jurisdiction for oil companies and Namibia and South Africa are going to play nice at least until the production starts in 2029. Now it’s the exploration phase so they need foreign investment. Not many risks from jurisdictions at the moment.

Eco is an asymmetric investment opportunity.

The En

Great write-up. An interesting lottery ticket.