AlmostMongolian 2023 Recap+Portfolio update

and a lot of mindless rambling

DISCLAIMER: None of this is investment advice. Do your own due diligence before investing in any company. The AlmostMongolian portfolio could be a mere figment of my imagination. The returns I provide for the closed positions could also be completely inaccurate and possibly also imagination. Don’t trust anything you read below.

The disclaimer is to protect myself. Not for now, but for the future. Because in the future people will want to copy the AlmostMongolian portfolio. In the future, everything will be different. And while this is a 2023 recap it will mostly concern the future.

Stocks.

AlmostMongolian Portfolio:

I have 12 positions now. All long. No margin. No BS. I have been mostly closing positions during this year and purposely reducing the amount of positions. Because I think I had too many earlier. I might still have too many.

What is the optimal amount? 10? Many people say 10, but I think that is because of the psychological effect of the number 10. The idea of having exactly 10 positions feels right in my head. But that does not mean 10 is necessarily the optimal amount of positions. It could be 9, 11 or 6, but those numbers sound much less satisfying than 10. The perfect 10, 10/10. So I might just aim for 10 positions because of that. Just because I like the idea of having 10 positions. But in reality I have no number I don’t know the number. I don’t think there is an optimal number. Let’s just say more than 3 and less than 20, but optimally 10.

I hope that was useful. Now stocks.

Positions ordered by size(CB=Cost-Basis):

$MIND Mind Technology CB 5,6 USD

I did not expect to find Mind here as the biggest position, but here it is and I don’t mind it. I was adding at 4-5,2$ area and the company ended the year strong at 6,59$ now at 6,3$. Up 41,81% in 2023. The orderbook of this company has been exploding recently. During december Mind announced a record backlog and after that, a record order. I was already bullish before this happened so I’m excited about 2024 for Mind. I’m trying to contain my excitement with this one. It could be the one.

$ASTL Algoma Steel CB 6,62$ USD

Algoma was the biggest position until I reduced the position after it reached 10$ just before the new year. My view on Algoma has not changed at all. It ended 2023 strong and then had some profit-taking at the beginning of 2024 and steel price weakness, but it’s still up around 45%. from my cost basis and I’m looking to keep it as a large position, but to trim it during steel price rallies and add during steel price dips. The strength in the stock price at the end of 2023 was the result of strong steel prices and US Steel being bought out. In my last Algoma article, I made an argument as to why I think Algoma is also an attractive acquisition target as the global steel market is turning to EAF.

$ESI.TO Ensign Energy Services CB 2.76$

I added to Ensign at 1.9-2.1$ area recently to reduce my cost basis. I feel like that price Ensign is a really good risk/reward. But I do not see Ensign staying in my portfolio if we get to a 700-800m CAD market cap and I think this is highly likely to happen during 2024. The market cap is now 400m CAD. The thesis is solid, but I just don’t see the margin of safety or the upside at 700-800m market cap that I see with my other investments. I also want to focus more on obscure microcaps. and this is not an obscure microcap it’s a very unobscure midcap.

Source: Google

If you look at how this thing trades it’s quite erratic and moves mostly on sentiment. From 2022 to 2024 there has not been a lot of change in the financial performance. It improved in 2022 and then weakened a bit in 2023, but the stock price has been having 50-100% moves up and down. That is due to their leverage and also the fact that they do not pay dividends or do buybacks at the moment. Because of this, there is not much to support the stock when the sentiment on oil drilling activity changes to bearish.

I expect there will be another run to the 4$ area next year when oil has a next spike up or the us rig count starts increasing again and I’m most likely getting out at that point. But the core thesis is solid they will look to pay 200m CAD of debt per year from cash flow. It would make sense that as they pay their debt the market cap starts getting closer to the EV at the rate the debt is paid off and their EV is 1.67b. Also, this increases their earnings as current interest costs eat into their earnings in a big way. They are not building new rigs. Their management compensation is reasonable. Their biggest shareholder and chairman is the billionaire Edward Murray who is also a chairman of CNRL a huge 98b CAD market cap company. The CEO also recently loaded up on the stock at higher prices

Source: Google

If the financials are in line with recent years this company trades at around 40-70% FCF/Market cap which is cheaper than peers. They refinanced the debt so that is not an immediate issue anymore.

From the macro side, I’m bullish on oil for 2024. Well less bullish than I used to be only because I have realized the difficulty of predicting commodity prices. The good thing is the supply of rigs has been reduced in recent years. This is why the rates can stay high despite US Rig count having decreased and when it starts coming back…

Source: Nov, the tweet was made by “The Energy Realist” a good account to follow

And then in Canada there is the Trans Mountain Pipeline expansion next year and LNG Canada… Canada should be active this year.

There are some reasons why I think it’s likely we will see Ensign have another upswing to 4$ area maybe higher. I don’t know if it will be short-lived again. The current valuation is attractive and there are so many factors going for the company I made it a big position recently so if I can get out after a 60-100% move from here and redeploy it to my obscure investment I will be happy. It does make sense as a long-term deleveraging bet as well, but I wouldn’t expect a grazy upside.

$VXTR Voxtur Analytics CB 0,33 cad

Source: Google

Voxtur was down again. What a surprise.

Voxtur disappointed this year. The new AOL product which had big expectations didn’t do anything. The Ontario RPTA contract didn’t happen. Even thou it was around the corner like it always has been. We had more dilution than expected. Profitability was pushed further into the future. And macro for real estate tech was horrible. Almost no refinance, very low originations, and also very low foreclosures. So it was not really a surprise that the stock is down as much.

The good developments during the year were with Bluewater which I focused my Voxtur write-up on. I believe Bluewater is worth more than the EV of the company currently. The sale of their AMC business which allowed Voxtur to reduce debt and reduce the risk of another raise was a positive development. There are a lot of new products coming out and the market is skeptical about them, because of the recent memories of AOL and RPTA.

Now we are just waiting for profitability and Bluewater to take off. Well, when Bluewater takes off so does profitability, but nothing is certain. The stock has become a very attractive risk/reward due to the decrease in valuation which has caused me to add despite this being my worst investment ever. I still see a lot of potential with this company.

Source: CNBC

While macro is still bad for Voxtur it is showing some improvement. But as we are starting at such a low base for the stock even a small recovery can be a significant turning point for Voxturs’ beaten-down stock.

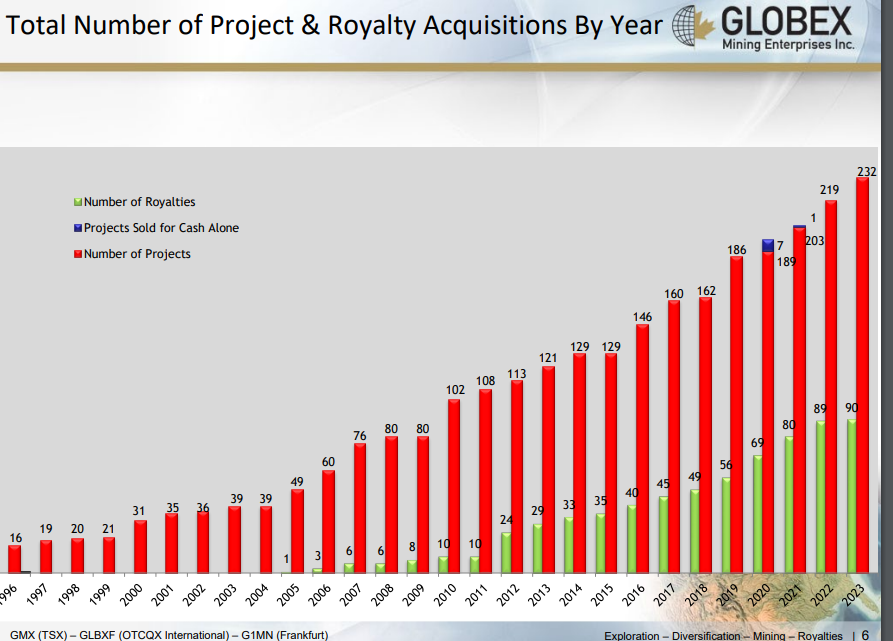

$GMX.TO Globex Mining Enterprises CB 0,76$ cad

Globex has been an alright bet so far. The news has been good some smaller deals and positive developments on their royalty properties, but nothing huge.

The biggest news since my entry has been positive developments with the Mont Sorcier property Globex has a royalty on. If the property is developed it would make Globex around 6-12m CAD annually depending on iron prices. This would be huge for a company with an EV of 25m CAD.

https://finance.yahoo.com/news/globex-mining-enterprises-mont-sorcier-172300236.html

https://ceo.ca/@globenewswire/more-progress-at-globex-mont-sorcieriron-royalty-project

https://seekingalpha.com/pr/19545039-td-bank-appointed-lead-arranger-mont-sorcier-project

Source: Globex corporate presentation

The number of projects has also kept increasing. When I wrote this company up on last May they had 220 projects.

Gold the commodity Globex is most affected by has been strong recently which helps, but I don’t need gold or metals in general to be strong for Globex to work out. That helps but is not necessary. I expect this to be a slow grind to realize the value in their portfolio already or they land something huge and the stock rockets I don’t know, but when the stock is cheap and has a great margin of safety, and does buybacks the odds are in my favor.

$AOI Africa Oil CB 2,34$ CAD

Africa Oil is cheap. Positive news in 2023 was the license extension in Nigeria and a decrease in their tax rate. In the negative news, the Nara well in their Venus discovery didn’t work out. Other than that Venus news has been good. Total is serious about developing it, but they are keeping cards close to their chest.

There was a big news 10.1.2024. Venus stake has been farmed out. Shortly their interest was cut in half, but they do not have to spend money on development anymore and “Impact will also be cash reimbursed on closing for its share of the past costs incurred on the Blocks net to the farmout interests, which is estimated to be approximately USD 99 million.” So that is going to be around 33m for Africa Oil. Not significant but nice.

https://africaoilcorp.com/news/africa-oil-announces-strategic-farmout-of-impacts-122899/

This is good news in my opinion. It removes the risk and uncertainty with Venus. It frees up money for what I hope will go towards buybacks. If Africa oil stayed in fully almost all of their FCF would have gone to this development. If they completely sold it they would have received more money now, but they would not be able to participate in the upside Venus has anymore, and Total who has the data is eagerly wanting to increase their stake and develop this and it should tell you something. This is why I think this was the right way to go. And the market likes it but does not love it. The stock was up 7.1% in reaction.

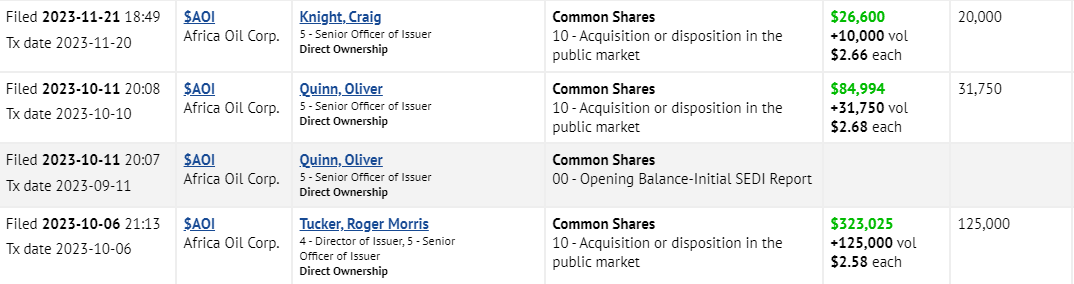

The stock itself has been a disappointment this past year as it was up slightly but considering the weakness in the oil price it’s not the worst thing ever. The new CEO was also brought in and he brought some other people in and they have been buying on the open market.

Source: ceo.ca

It’s cheap and I like oil so I don’t mind waiting for now. What I most like about Africa Oil is the shareholder base. I find their constant whining humorous but I respect their deep due diligence and passion.

UPDATE:

$ILLM.TO Illumin Holdings Inc. CB 2,03$ cad

2023 was an ok year for Illumin. Maybe a bit meh. Regardless I think the stock is dirt cheap and a great risk/reward. I will talk about this more in a full write-up coming during this month or next.

Source: ceo.ca

$ACTHF Aduro Clean Technologies CB 0,64$ USD

Source: Google

There have only been positive developments with Aduro during 2023 and everything looks good for 2024. The stock has performed very well considering its no-revenue microcap. It just pulled back from a new all-time high while other stocks similar to Aduro have been destroyed in 2022-2023. I think this is this is the highest potential position I have.

My thinking with Aduro was always that I do not need to make it a large position because if their technology works on scale and they can execute it will be a large position fast. But the risk in a company like this is high if things go wrong.

I will write about it more at some point. but if you want to know more about it now I suggest going to this YouTube playlist from Mariusz Skonieczny.

https://youtube.com/playlist?list=PLmubI4jYIeYXlKiZcVnrm5W9OJ1l_fM1o&si=J9sSs4unJEuhnrXs

$PEI.V Prospera Energy CB 0,08 cad

I was considering selling Prospera earlier this year because it was becoming clear for me that junior oil stocks are not a good place to be. Most of them are not successful and I’m not knowledgeable enough about the space to differentiate them and many investors in that space also pay for services like Petroninja and they are getting information about the companies’ production earlier than me. I’m at an information disadvantage, but I have not sold Prospera. Why?

I did sell around a third of my Prospera at around 13 cents in September and was thinking of selling the rest, but then it dropped to 8,5 cents where it now stands just a bit above my cost basis after their successful drilling program.

Source: ceo.ca

So I don’t know what is the problem. Well, I do know that the oil price is part of it, but this drilling program is more important than the oil price for Prospera. Maybe that drilling success was largely priced in. I do find that odd as well because why would the market expect a junior oil company to deliver? It’s crazy.

With Prospera, I’m thinking about an exit plan. I’m not looking to hang out in an oil junior in Canada for the reasons I laid out before. So I will look for a spike in the oil price coupled with Prosperas’ increasing production showing in their financials as significant profit. Then some Youtube videos from Kerry Lutch, Mining Stock Education and maybe another long one from Shubham. Prospera has some relatively popular internet people covering it. To get a nice shot of new retail investors to Prosperas’ arm during their success could give me a nice rally to unload. But maybe I won’t and I get further indoctrinated by Propera and become a long-term investor.

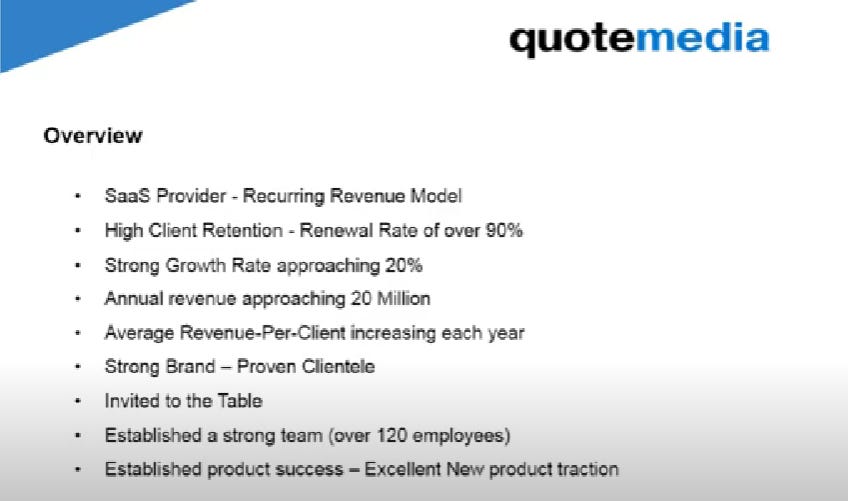

$QMCI Quotemedia CB 0,22$ USD

I like this company I think it’s a gem within the OTC market. Here is a video you can see what they do.

It’s great. But I did try to sell it at 28 cents in October but my order didn’t get filled then it went down. I did not want to sell Quotemedia, but I wanted to buy something else at the time. This stock is very illiquid so the market price is not the real price you can get there is a large bid-ask spread. It’s hard to buy and sell.

Source: Google

It went down, but I’m confident we will be back at 30 cents in the not too distant future. The stock seems to make higher lows and I think fundamentals justify it. They do not grow at a rapid pace but at 8-20% pace yearly. They are profitable but not much at the moment. That is one thing they underperformed this year they projected higher net income for this year which doesn’t look like will be reached. But the company trades a 1.35 p/s and has net cash and It’s Saas, recurring revenue, a great track record and they landed some big clients in recent years. So I think this will trade at a higher valuation in the future especially as the Fed starts to cut rates.

Source: Quotemedia

I’m still mulling over what to do when this goes back to 28-35 cents. Because I think this could be one of those “long-term investments” I mean real long-term investments not like some of my other “long-term investments”. But I feel like at a higher valuation it lacks some punch. Like Mind has punch. But it seems that Quotemedia is just happy being a good company. It’s infuriating.

$SMSI Smith Micro Software CB 1,35 USD

I will likely do a full write-up on this company at some point. Shortly I’m somewhat conflicted, but bullish. Has not been a good pick so far.

$MLX.AX CB 0,285$ AUD

Metals X is a boring stock. They have one tin mine in Australia. I got in it after last summer when the market had no reaction to Myanmar Wa-state stopping tin production. It’s cheap. Tin has good supply/demand dynamics. They have no debt and tons of cash. The company is profitable at current tin prices. The risk/reward is in my favor. I’m happy to wait with it, but I don’t see a reason to make it a large position. I don’t see the upside that I see with the stocks above. The management is also not very shareholder-friendly. If they would slam buybacks I would be willing to invest more.

Closed Positions+Total Return of each closed position

Tracking starting from 1.4.2023. It starts from there because before that there was too much trading, too many transactions. I use total return because it includes dividends.

Ordered by how much money was gained or lost(not %):

Biggest gains or losses first and smallest last

8.12.2023 $PBR.A +71% (margin)

https://twitter.com/AlmostMongolian/status/1733237895148835244

My reasoning for this sale is in the link above, but if clicking a link is too laborious for YOU I will write a quick summary of it.

The main reason for selling pbr.a was to reduce margin. I still like the stock, but the risk/reward is worse than it was at 9$. I think it will go higher over time. It’s still the cheapest major oil company.

My investment was basically the Lula fear from beginning to end. I started when the fear about Lula was high and then it reduced because the market saw it wasn’t that bad and the stock didn’t deserve to be that low and now we are back to the prices during the previous administration. Now the bull thesis is no longer “Lula will not destroy the company” The market doesn’t think that anymore bull thesis now is a strong dividend, some rerating, oil bull case, and their offshore production growth which it’s still a good thesis.

This was the best bet of 2023 because it was the biggest position by far. Position sizing matters a lot this +71% gain was bigger than many +200-800% gains in the past because those were small positions.

$RZE Razor Energy -65%

Razor has been a very poorly performing company. It was by far my smallest position when I sold it, but it wasn’t always my smallest position. That is what -65% does.

Above is a representation of what it’s like to be invested in rze.

I sold the stock at 3.1.2024 and I’m annoyed because I sold it at 0,3 CAD and about an hour from the point of my sale the stock went to 0,475 CAD without any news it even touched 60 cents. WTF?! Now it’s back to 0,34. During the past month, the timing of my exists has not been good. This and Zim both I sold and then they rallied. The Zim rally makes sense. But this $rze rally was more weird. Because there is no catalyst for this run that is publicly known.

Maybe someone knows something or it’s just microcap BS. Someone wants a lot of shares there is not enough available the stock rallies people start thinking somebody knows something the stock rallies more in a speculation fever and after a while it gives up all the gains. I think it’s more likely that this is the case.

Why did I decide to sell Razor? Many people in the oil investing space would laugh at the question itself. I wrote a bit about how I thought investing in Razor was a mistake in my last article. The main point was that my reason behind that investment was the torque Razor offers to the oil price and that is not a good reason alone to invest in a company I have learned that predicting commodity prices is very difficult especially mid- and short term. But among the oil price being somewhat weak Razor has also screwed things up operationally.

During the summer they had a nice setup. They eliminated most of their debt in exchange for effectively 80% of their power plant. Just the interest cost saved from this was more than the profits the powerplant was making. Then they raised 8m to increase production by 800boe. So if they had managed to do this and oil prices were decent this could have been a slam dunk.

But they failed to do this. And q3 financials revealed they had spent almost all of the money from that raise.

So that was bad. Then oil prices went down and then they released more bad news.

Source: ceo.ca

It seems they can’t pay their bills to the gas plant and almost a third of their production is shut down. And their balance sheet is horrible.

The way I see it something needs to be done they need money. And a raise would be massively dilutive because of how low the market cap is. I don’t think the lender wants to take them bankrupt because of all the ARO liabilities they would incur, but something needs to happen and I think most likely whatever happens will be bad for the common shareholder unless someone wants to buy them out.

Source: Google

I was happy to get rid of it at 30 cents because when the gas plant news was released I thought this might be a zero or near zero. So the rally to 30 cents surprised me and the stock spiking quickly to 60 cents made me shake my head. Regardless I’m happy to be rid of Razor.

14.12.2023 ZIM 0.00%↑ -22% (margin)

https://twitter.com/AlmostMongolian/status/1735411187968278689

I made this tweet announcing my exit, but considering the Red Sea thing started really escalating right after I sold I will write a bit about what I think about it and why I’m not getting back in because of it.

So naturally I’m very annoyed by the timing of my exit. Because the stock was 8,3$ when I sold and it’s now at 12,89$. So IF I had waited for a bit… if if if. Never say “if” in investing. It drives you crazy. There is always an if. But there was a lesson here for me.

I already lost my conviction in Zim during the autumn, because I realized I had looked at the investment the wrong way and I also realized I had been looking at their financials the wrong way I was starting to agree with the Zim bears, but I thought it’s oversold and it’s very heavily shorted. At the time the stock was 12$ and I thought It’s reasonable to think there would be a bounce. A little short squeeze to 14$ to unload my position. Well, the stock kept going down without a bounce all the way to 6,5$ and then it had the bounce. Out at 8,3$.

Now I guess I should have kept it because of the Red Sea. Right? That is a bullish event. But that is the problem with holding a stock where you have no conviction to the core thesis every bullish event that makes the stock go up will look like a selling opportunity. When I have conviction in the core thesis bullish events are just extra gravy like with Globex and gold price going up.

Let’s say I keep the stock because of the Red Sea. Zim is very torqued to whatever happens in the Red Sea. If it’s a prolonged situation Zim will go up if it’s resolved then back to all-time lows we go. So I would be just speculating about what is going to happen in the Red Sea. And I have no clue what is going to happen with the Red Sea there are like a million variables.

Having said that I will say this about the Red Sea. Because a lot of people are on the prolonged situation side of the argument at the moment and I already said I have no clue, but the money wants the Red Sea to be safe. There are way more people with deep pockets who are getting hurt from this than benefit from this. And almost every country is getting economically hurt because of this. So I would find it odd if this is not going to be dealt with one way or another.

In summary, because I have no conviction to the core thesis apart from the Red Sea anymore and I have no clear view of the Red Sea this is why I’m not getting back into zim atm.

This Zim section was way too long. Just massive cope because of my bad timing.

3.1.2024 Nasdaq-100 ETF short -14%

This was only as a hedge to the margin portfolio, but because I sold my longs that were on margin this has become obsolete. I also did his weird thing where I always shorted more when the CNN fear and greed index was extreme creed and closed when it was extreme fear as an experiment. It worked for a bit and then it didn’t work, but I’m not interested in continuing this experiment. I don’t want to stare at the CNN fear and greed index all the time. I want to focus on finding and researching great investment opportunities.

Overall I’m not interested in hedging my portfolio from the market. It’s net cash anyway. I do not want to use time and money to do something that in the long term will likely mostly benefit my broker.

8.6.2023 $EC 0.86%↑ +17% (margin)

Ec is the Pbr.a light. I like it but not enough to buy it.

12.4.2023 $CGG.PA -7% (margin)

I do not have much to say about CGG. I know what they do. That’s it. That would be my answer if someone asked me to pitch them CGG while I was holding CGG. I used to have many of these positions in the past that would just linger in my portfolio without much reasoning behind the purchase.

2.11.2023 $CRMZ CreditRiskMonitor +2%

This is a good company. I bought it as a kind of hedge in case there are big economic problems. This company benefits from economic problems. But if there is not it’s low growth, decent profit, decent valuation, great balance sheet. It’s good, but I look for more than good.

I have also noticed trying to be fancy leads to problems. Hedging the market using the Nasdaq down -14%, trying to be leveraged to oil using $rze down -55% and with crmz I was trying to hedge macroeconomic issues. I don’t think I would have lost money holding CRMZ long-term, but underwhelming returns are also not good. Let’s say I hold it for 3 years and I’m up 20%. That is not the kind of return I will accept.

So I will try to avoid being fancy in 2024.

Returns

I don’t know the yearly return % exactly. There are many accounts etc and some of the positions are bought directly from a bank and they don’t give past returns numbers or charts after I sell the position. But I did start tracking returns of the closed positions and put up the cost basis so something can be figured out from those. Remember the portfolio and the returns might be fictional. But it was a pretty mediocre year based on returns. Maybe +5-15% or something like that. Petrobras did a lot of work because I went irresponsibly heavy on margin to buy that at 9$. I don’t think doing that is smart in general but it worked this time. That offset some of the other poor performers. And the worst investment was again Voxtur by far. I ranted about Zim and Razor but those were smaller positions so they didn’t affect the pig picture much, but Voxtur. Not good.

I have high hopes for 2024 and 2025. I have never felt so calm and yet optimistic about my portfolio. And there are some very interesting stocks I’m following in my watchlist which I’m not revealing yet.

Well, I will reveal one because it is making me angry. Southgobi resources $sgq.v which is a coal miner in Mongolia the second greatest country in the world that this person called “Emil Baggie.tinkaren” brought to my attention on Twitter.

I know this stock from the past.

Source: Google

See that spike from 2021. I was there and in the 2nd half of 2023, there was another change.

I should have already 'pulled the trigger when they had a profit warning a couple of months ago. The setup was so good. Then they had a great q3 and the stock started going up I had an order at 0,3 cents but it never got filled. Now it’s at… You can see it. And I will not chase. Maybe I should. They will make so much money as they ramp up exports.

Lessons

It was not a year of great returns but it was a year of lessons. A year of learning. This is what one says when the year was not lucrative, but it was a year of learning. Really. The AlmostMongolian that started 2023 is an amateur compared to the AlmostMongolian that is writing this in 2024. The 2023 AlmostMongolian was like this: He used margin. He would actively trade. He would try to hedge. LOL. He would buy an oil stock based on the torque it has to an oil price. Or a shipping stock he has no clue about how their business and financials work. Not anymore.

My big lesson other than “do your DD” is to stop doing all the things that my broker wants me to do like trading, using margin, hedging, shorting, derivatives… this is all stuff that the casino is creating for you to get you to play more and pay them more fees. The odds are stacked in my favor when going long cheap companies because they have value or are creating value, but with this other stuff, it has been created for speculation. So you have people who are trading with each other and then a broker takes a cut so it’s in total net negative for the people trying to make money trading these things.

I also learned patience. I used to invest all the cash immediately. Now I wait and use limit orders. I wait for the ridiculous dips. Because I have seen so many of them. For example, just a couple of months ago mind hit 4$ after the reverse split and Algoma went to 6.5$ because of some steel price weakness. I know there is always one ridiculous dip coming.

Commodity investing: Order of importance

I started investing in 2019 and I started investing in commodities in 2020 and I have continued investing in commodities to this day. I like the volatile boom-and-bust nature of it. I feel like it’s a great place to try to “buy when others are fearful and sell when others are greedy”. My biggest winners have been from commodity stocks. A lot of that is …

A lot of the lessons of 2023 concerning commodity investing are in the article above.

I also focus much more on the margin of safety as I have noticed my worst investments tend to lack it. I invest based on risk/reward, but I need to focus more on the risk part of that equation. Sometimes I have gotten too excited about the upside forgetting the risks.

“The first rule of an investment is don’t lose [money]. And the second rule of an investment is don’t forget the first rule.” Warren Buffett

I just rediscovered this quote from the goat. I need to start applying it. Do not lose money. So simple yet so brilliant. Armed with this quote AlmostMongolian will be unstoppable in 2024.

For me best strategy is to buy at 52 week low,with an up trend in fundamentals and share price

Have been looking too at ILLM, charts looks good with insiders buying.